The empirical relationship between short- and long-term VIX is imperfect, something that we show can be explained theoretically with the presence of both short- and long-term uncertainty shocks. We suggest a theory-informed, nonrecursive identification strategy to separately identify the macroeconomic effects of short- and long-term uncertainty shocks in a structural vector autoregressive (VAR) model. We find that long-term uncertainty shocks have stronger and more persistent real effects than short-term shocks. Moreover, they are an important driver of fluctuations in unemployment and the policy rate at horizons greater than two years. In a supplementary analysis of anticipated uncertainty (news) shocks, we show that news about higher uncertainty in the future is recessionary.

Macroeconomic research has widely documented that uncertainty shocks are recessionary. But are the effects of uncertainty shocks all alike, or can they differ fundamentally according to the resolution horizon of uncertainty? In principle, uncertainty can relate to both short-term aspects of the economy but also to longer-term dynamics. The conventional approach in the empirical literature on the macroeconomic effects of uncertainty shocks is to use a single measure of uncertainty – typically short-term – from which a generic uncertainty shock is identified (e.g., Bloom 2009, Leduc and Liu 2016, Basu and Bundick 2017, among others).

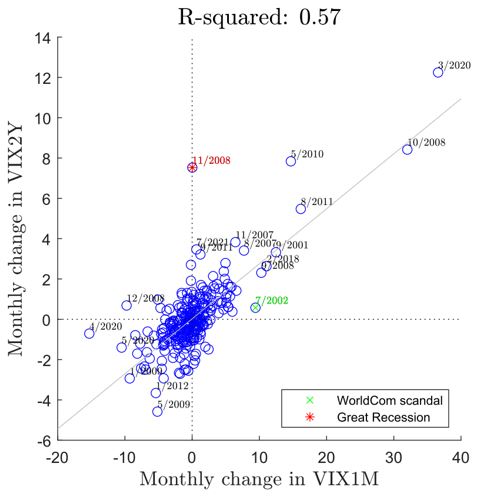

In Krogh and Pellegrino (2024), we estimate the term structure of the VIX using a large dataset of S&P500 options (OptionMetrics) and show that jointly considering short-term and long-term financial uncertainty, as proxied by the 1-month and two-year VIX, allows the separate identification of the macroeconomic effects of short-term vs. long-term uncertainty shocks in a structural vector autoregression (VAR). We exploit the imperfect empirical relationship between short- and long-term VIX changes, as can be observed in Figure 1. As the figure shows, sometimes one of the two VIX moves significantly while the other does not, something that, for example, occurred in November 2008 (in correspondence with the Great Recession) and July 2002 (WorldCom scandal). In particular, the one-month VIX explains only 57% of the monthly changes in the two-year VIX, suggesting that the conventional one-month VIX captures only part of the market’s expectations about future financial uncertainty. Hence, considering a longer-term VIX, such as the two-year VIX (the most forward-looking available), allows to capture uncertainty at longer resolution horizons.

Figure 1: The imperfect empirical relationship between VIX-1M and VIX-2Y

Note: Scatter plot of monthly differences in the one-month and two-year VIX in the sample 2000M1—2020M12. The grey line represents the best-fitting (OLS) line.

As documented in our working paper (Krogh and Pellegrino 2024), we extend the state-of-the-art theoretical macroeconomic model by Basu and Bundick (2017) to include both short- and long-term uncertainty shocks and show that jointly considering the two shocks is essential to generate an imperfect relationship between short- and long-term financial uncertainty as observed in Figure 1. Within this theoretical model, we find that: i) both short-term and long-term uncertainty shocks impact the entire VIX term structure, implying that the common Cholesky recursive identification is invalid; and ii) the key distinguishing feature between the two uncertainty shocks is the persistence of their effects on the VIXs, an insight that we exploit in our identification strategy.

We apply a theory-informed, nonrecursive identification scheme within a structural VAR to separately identify the macroeconomic effects of long-term and short-term uncertainty shocks in the US for the period January 2000 – February 2020. Our analysis is closely related to that of Leduc and Liu (2016), who use a small-scale recursive VAR with the following variables: the standard one-month VIX, the unemployment rate, inflation, and the policy rate to identify uncertainty shocks. With respect to them, i) we augment their model with the two-year VIX to capture market expectations about financial uncertainty at longer horizons and ii) identify uncertainty shocks with a nonrecursive approach. Specifically, we rely on standard sign restrictions derived from theory and narrative sign restrictions building on Ludvigson et al. (2021) (details can be found in Krogh and Pellegrino 2024).

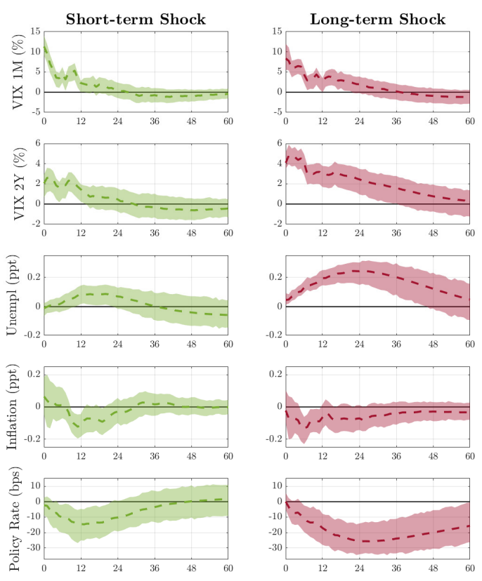

Figure 2 plots the dynamic impulse responses produced by our econometric analysis. Four main results arise. First, long-term uncertainty shocks have a much stronger and more persistent effect on the 2-year VIX than the one-month VIX relative to short-term shocks. Second, short-term shocks mildly impact unemployment, peaking at less than 0.09 percentage points after 12 months, whereas long-term shocks have a stronger and more persistent effect, peaking at around 0.24 percentage points after 25 months. Third, the policy rate decreases in response to both uncertainty shocks but, again, with bigger and longer-lasting effects to long-term shocks (reaching a decrease of 25 basis points after two years). Fourth, both shocks are deflationary.

Figure 2: Impulse responses to short-term and long-term uncertainty shocks

Note: Sample 2001M1—2020M2. One standard deviation shock. Dashed lines are posterior means, and shaded areas are 68% highest posterior density intervals.

The Great Recession is one of the most prominent examples of spectacularly high levels of financial uncertainty in modern economic history. Several policymakers and researchers have argued that heightened uncertainty significantly contributed to the length and severity of the Great Recession (e.g., respectively, Blanchard 2009 and Alessandri and Mumtaz 2019). Did long-term uncertainty shocks contribute to the Great Recession?

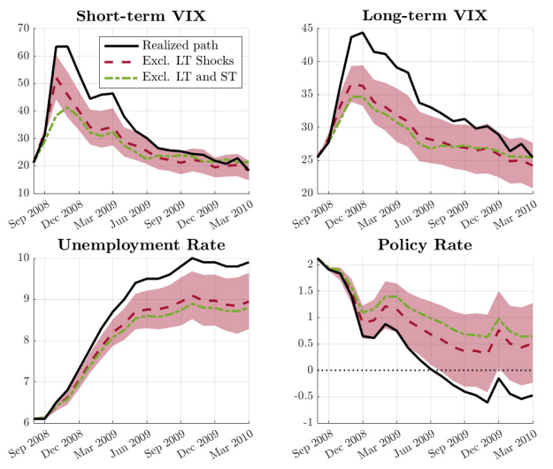

To illustrate the contribution of long-term uncertainty shocks to the Great Recession, Figure 3 compares the realized historical path of the unemployment rate, the policy rate, and the two VIXs with two counterfactual scenarios: a scenario where no uncertainty shocks (neither short-term nor long-term) materialized between September 2008 and March 2010, and a scenario where only short-term shocks occurred. The black line, representing the historical path, shows that in September and October 2008, i.e., amid the financial panic of the crisis, the two VIXs increased massively. From December 2008, they started to decay and returned to their initial value around March 2010. In the same period, the unemployment rate rose from 6% to 10%, and the policy rate fell from around two percent in August 2008 to the zero lower bound (ZLB) in December 2008. Later, after having reached the ZLB, unconventional monetary policy was adopted as conveniently captured by the shadow rate of Wu and Xia (2016). Figure 3 suggests that long-term uncertainty shocks contributed significantly to the severity and duration of the Great Recession: The unemployment rate would have increased by one percentage point less at its peak in October 2009 (i.e., roughly one-fourth less, a statistically significant difference), and the policy rate would have exhibited a less dramatic decline.

Figure 3: Counterfactual on the Great Recession for the role of long-term uncertainty shocks

Note: Black lines indicate the realized paths of the one-month VIX, the two-year VIX, the unemployment rate, and the policy rate between 2008M8 and 2010M3. Dashed red lines (dashed-dotted green lines) illustrate the counterfactual paths that would have occurred if no long-term shocks (no uncertainty shocks) had materialized from 2008M9 and onwards. Shaded areas indicate 68% highest posterior density intervals.

In our working paper, we also present a supplementary analysis of anticipated uncertainty (news) shocks and find that they are recessionary and inflationary. A literature review is also available.

Regarding policy implications, our study highlights the potential pitfalls of monitoring only a single-horizon uncertainty index. Doing so could lead to shortsighted decision-making, and it is thus recommendable to monitor uncertainty at multiple horizons. Similarly, for applied work, our results imply that using only a single-horizon uncertainty index in a macroeconomic VAR confounds the effects of short- and long-term uncertainty shocks and may understate the importance of uncertainty.

Alessandri, P. and H. Mumtaz (2019). Financial regimes and uncertainty shocks. Journal of Monetary Economics 101, 31–46.

Basu, S. and B. Bundick (2017). Uncertainty shocks in a model of effective demand. Econometrica 85 (3), 937–958.

Bloom, N. (2009). The impact of uncertainty shocks. Econometrica 77(3), 623–685.

Blanchard, O. (2009). (Nearly) nothing to fear but fear itself. The Economist. Jan 29th 2009.

Krogh, M., and G. Pellegrino (2024). Real Activity and Uncertainty Shocks: The Long and the Short of It. Marco Fanno Working Paper No. 310, University of Padova.

Leduc, S. and Z. Liu (2016). Uncertainty shocks are aggregate demand shocks. Journal of Monetary Economics 82, 20–35.

Ludvigson, S. C., S. Ma, and S. Ng (2021). Uncertainty and business cycles: Exogenous impulse or endogenous response? American Economic Journal: Macroeconomics 13(4), 369–410.

Wu, J. C. and F. D. Xia (2016). Measuring the macroeconomic impact of monetary policy at the zero lower bound. Journal of Money, Credit, and Banking 48(2-3), 253–291.