Russia has witnessed a high number of bank failures over the last two decades. Using monthly data for 2002-2020, spanning four presidential elections, we test the hypothesis that bank failures are less likely before presidential elections in our new paper.1 We find that bank failures are less likely to occur in the twelve months leading up to a presidential election. However, we do not observe election cycles in bank failures are more pronounced for banks associated with greater political costs. Overall, our results provide mixed evidence that political cycles matter for the occurrence of bank failures in Russia.

A growing literature suggests that politicians have incentives to interfere with the banking system to pursue their own interests, including their chances of reelection. For example, there is evidence that lending by state-owned banks accelerates before elections compared to private banks (Dinc, 2005; Carvalho, 2014). Regulatory interventions may also be used to affect the electoral outcome: macroprudential policies restricting access of voters to credit may be relaxed (Müller, 2019).

The experience of Russia over the past two decades provides a relevant natural setting to investigate how politics can shape bank failures. Two salient features of the banking sector in Russia stand out. First, the Russian banking system has witnessed a massive number of bank failures over the last two decades. These failures have taken place throughout this period, and thus are not clustered around the Global Financial Crisis. Second, there is evidence of the authorities intervening in the electoral process in Russia over the last two decades through media control, electoral fraud, and bank lending before elections (Schoors and Weill, 2020). Both of these features provide strong incentives for studying the potential influence of Russian authorities on bank failures.

There are at least two reasons for the authorities to limit the number of bank failures in election times. First, incumbent politicians are incentivized to avoid the political costs of bank failures. These costs arise from costs to the stakeholders of the bank (shareholders, employees, depositors), as well as costs to the taxpayer. Voters can perceive the cost of failure as a negative signal about the competency of the ruling government. Second, bank failures reduce the credit supply. This can have short-term negative effects on the economy and restrict the access of voters to credit. Career concerns may cause bank supervisory authorities to avoid taking actions that potentially harm an incumbent’s election performance.

The objective of this paper is to examine the existence of political cycles in bank failures in Russia. We ask whether the probability of bank failure around presidential elections differs from the probability of bank failure otherwise. Controlling for economic conditions, systematic fluctuation in default probability around presidential elections is taken as evidence for political cycles in bank failures.

To perform our investigation, we use monthly data on individual banks from the Central Bank of Russia (CBR) for the period 2002–2020. This enables us to identify the interplay between bank failures and elections over four presidential elections (2004, 2008, 2012, 2018). We perform estimations to explain the occurrence of failure at the bank level. In addition to bank fundamentals and macroeconomic controls, our model accounts for the timing of elections and the reasons bank licenses were withdrawn. We use an unbalanced panel of almost 200,000 bank-month observations for over 1,400 banks that includes over 700 bank failures.

This setting provides us with two key advantages. First, the use of monthly bank data and daily data on failures allows for a clean identification of the relation between elections and bank failures. We can precisely track the evolution of bank failures around the dates of elections. Second, our dataset on bank failures provides the information on the reasons for the bank failures. The reasons can be broadly classified as related to financial problems of the bank or illegal activities. This allows us to investigate the plausible channels linking bank failures to the timing of elections.

We show that the probability of a bank failure is lower in the twelve months leading up to an election. The effect is economically significant with a probability of a bank failure two to three times lower in the pre-election months than at other times.

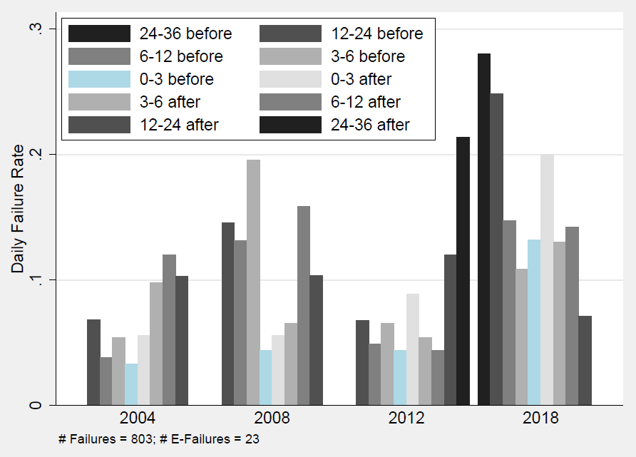

Figure 1 provides an illustration of this finding. It shows the monthly development of bank failures around four presidential elections that took place during the period we consider. The number of bank failures tends to decrease as the presidential elections are approaching. The sharpest decrease is visible up to three months before elections. After the elections, the number of bank failures tends to increase.

Figure 1: Failures over monthly intervals around elections

This key finding is confirmed by a large set of robustness checks. We notably check the existence of electoral cycles in non-failure bank closures. These closures are initiated by the bank itself rather than the regulator, and include mergers and voluntary liquidations. We find no electoral cycles for bank closures initiated by the bank, which accords with our interpretation that political interference takes place before elections to delay bank failures.

We can question whether our main findings hold for all types of bank failures. As discussed above, the authorities might have incentives to reduce the number of failures before elections to avoid the political costs of bank failures and the reduction of credit supply. However, the delayed failures of banks brought about by illegal activities can also generate political costs. To close dishonest banks cannot be interpreted as a signal as negative as closing a bank with financial issues since it can contribute to the image of authorities fighting corruption and dishonest practices. Hence, we assume authorities have greater incentive to reduce bank failures caused by financial problems. These failures also typically incur greater costs than those caused by illegal activities. In other words, our hypothesis about political interference in bank failure decisions is supported if we observe fewer bank failures caused by financial problems before presidential elections, while bank failures caused by illegal activities are less affected by election times. We therefore test the hypothesis that different types of bank failures are not affected in the same way before elections. We however do not find support for this hypothesis.

We can also question whether banks associated with greater political costs through greater share of household deposits in their balance sheet or through greater share of regional assets should be associated with a higher reduction in the probability of bank failure. We test this hypothesis but find no support for it.

To sum up, these estimations provide no evidence that certain types of banks would be particularly concerned by the electoral cycles of bank failures. Consequently, they do not bring additional support to our key hypothesis of political interference in the process of bank failures before elections.

We show that the probability of a bank failure is lower in the twelve months leading up to an election. However, additional estimations do not corroborate the hypothesis of a political intervention in the decision to revoke a bank’s license. Thus, we find mixed evidence supporting the hypothesis of political interference in the process of bank failures before elections. The main take-away is that bank failures might be delayed for non-economic reasons. Our work helps understand bank failures in Russia. As failures cannot be fully explained by weak fundamentals at the bank level or by macroeconomic cycles and changes in the bank supervision at the country level, political factors matter through electoral cycles. The key policy implication is that the process of revoking a bank license should be more independent and less susceptible to political incentives. This lesson from Russia may also be relevant for other countries since politicians can have incentives to interfere in the process of bank license withdrawal.

Carvalho, D. (2014). The Real Effects of Government-Owned Banks: Evidence from an Emerging Market. Journal of Finance, 69 (2), 577-609.

Dinc, S. (2005). Politicians and Banks: Political Influences on Government-Owned Banks in Emerging Countries. Journal of Financial Economics, 77, 453-479.

Müller, K. (2019). Electoral Cycles in Macroprudential Regulation. ESRB Working Paper No. 106.

Schoors, K., Weill, L. (2020). Politics and Banking in Russia: The Rise of Putin. Post-Soviet Affairs, 36 (5-6), 451-474.