A lot of macroprudential research today focuses on quantifying the build-up of vulnerabilities in the financial system, as well as on quantifying risk materialization in the forms of financial stress that occurs in the system itself. However, there is still a lack of research linking the build-up of vulnerabilities to the risk materialization approach. This research tries to fill that gap. Focus is put on the prediction of the probability of (re)entering high financial stress (via a large set of cyclical risk accumulation indicators). The regime-switching models’ results indicate that some credit specifications, house price dynamics, and debt burden could be best monitored for the case of Croatian data.

By looking at the literature and empirical practice of macroprudential policy, it could be said that two streams of financial indicators analysis exist. One has a goal to predict the turning points of a financial cycle or financial crisis and the other has a goal of measuring the state of the financial system’s instability. The amount of literature that focuses on one or the other important aspects has grown in the last decade as macroprudential policy has developed. Duprey and Klaus (2017) is the first paper (to the knowledge of the author) that tries to merge the two approaches together, in order to try to evaluate the potential predictability of risk materialization measured via the financial stress indicator, based on the indicators that are preferred in EWS (early warning system) models.

Motivated by the results in the aforementioned paper, this study has the following contribution. It tries to find a set of indicators that help forecast financial stress, switching from one regime to another, while utilizing techniques to reduce their number. This study observes many different variables and their transformations in order to find the best ones. It is challenging to monitor a whole set of indicators of cyclical risk buildup but the results of this research could bring into clear focus a smaller group of essential variables. Furthermore, most existing research focuses on predicting the value of future stress and concludes that it is challenging to predict stress levels. An extensive analysis is made of over several hundred variants of indicators of cyclical risk accumulation. In that way, the quality of regime-switching models is examined in a fashion that has never been accomplished previously (to the author’s knowledge).

There are a couple of reasons why we focus on the regime-switching approach and Croatian data, and the combination of both approaches. First, regime-switching models have been extensively used and found to be useful in modelling business cycles (see, e.g. Doz, Ferrara and Pionnier, 2020) and financial markets (Ang and Timmermann, 2012). Furthermore, research has found that the interaction between financial stress and the real economy is not linear. Quite the opposite, the relationship is asymmetric and exhibits nonlinear behaviour, as seen in Giglio, Bryan and Pruitt (2016), Cardarelli, Elekdag and Lall (2011), or O’Brien and Wosser (2021). Moreover, Vermeulen et al. (2015) show that spikes in financial stress occur abruptly. Another important issue is that forecasting future crises does not rely solely on the value of a variable (i.e. the value of the stress indicator itself). Still, the probability of crisis occurrence is also important (Gneitinga and Ranjanb, 2011) and it is more important when making policy decisions.

Next, Croatian data are observed as this area of macroprudential policy practice is not sufficiently explored for this country. On the other hand, the country has known an extensive macroprudential approach over the last two decades. Croatia has a specific, i.e., unique experience regarding macroprudential policymaking and monitoring cyclical risk accumulation. It stands out due to it belonging to a group of countries that had the most intensive use of instruments before the global financial crisis (Vujčić and Dumičić, 2016). This means that macroprudential policy was active during the boom and bust phases of the financial cycle. Analysis regarding Croatian data could provide insights into the effects of macroprudential policy during all phases of the cycle, the effects on the financial stress, and other analyses of interactions of this policy with the rest of the economy.

Although researchers are often prejudiced against single country analysis, there is actually a potential in focusing on one system, as compared to panel data analysis. For example, Klomp (2010) examined 110 different countries and found heterogeneity in the causes of banking crises, alongside an overview of previous related research that found different variables to be significant in predicting future crises, alongside different estimated signs.

Although panel analyses are very important due to their advantages over single-country analysis, countries cannot copy measures and instruments one from another directly due to country specificities. In fact, previous research that focused on early warning systems of crises has often incorporated country-specific analysis: Kaminsky and Reinhart (1999) estimate country-specific thresholds in minimizing the noise-to-signal ratio in the modelling process. There are significant differences between the country-specific and global thresholds in the EWS results found in Davis and Karim (2008), who, focusing on banking crises conclude that generalized global models cannot replace country-specific macroprudential surveillance.

Based on the literature review, it seems reasonable to analyse the effects of early warning indicators on the probability of future higher or lower stress, as the value of the stress variable is hard to predict. However, the selected indicators were found useful in the early warning literature, regarding the signalling approach to future crisis modelling. Variables utilized in this study are based on the literature within this group of papers.

Quarterly data on the following six (according to the ESRB (2014) Recommendation) categories of measures of cyclical risk build-up have been collected from CNB (2022): credit dynamics, potential overvaluation of property prices, external imbalances, the strength of bank balance sheets, private sector debt burden and potential mispricing of risks. As the availability of data varies depending on the variable category (or even within the category itself), to produce comparability of the estimation results, all of the variables after the initial transformations were brought to the same initial starting point of 4Q 2005. By covering all six risk categories, and taking into consideration different ways of data transformation (differences, growth rates, different filters, etc.), in total 240 variants of different variables were considered.

As already mentioned, financial stress exhibits abrupt changes over time, which regime switching models capture relatively successfully. The basic approach of the present research is to observe how different measures of risk accumulation affect the future probability of transitioning from one regime to another regarding the financial stress variable. Thus, the Markov regime switching models (MRS) are the most appropriate. The baseline model with fixed transitional probabilities is compared to the model in which these probabilities depend on previous values of each of the 240 variables. Due to aiming for parsimony on one hand, and real-time decision making process on the other, lags of independent variables were changed ranging from 4 to 7 quarters. This means that over 900 different models were estimated for comparison purposes.

To select best performing variables in all models, several criteria were taken into consideration: information criterions, optimal value of the optimised functions, empirical density functions of optimal values, alongside significance of estimated coefficients, with having a correct sign. Comparisons were made in specific risk category, across categories, and across different lags. Based on all of the results, it can be seen that the optimal value of the goal functions increases as the lag of the indicator variable shortens across all of the categories of measures. This is in line with the EWS research (ESRB, 2018; Lang et al., 2019; Alessi and Detken, 2019; Candelon, Dumitrescu and Hurlin, 2012), where the indicators should show a consistent increase in their value before the peak of the financial cycle occurs and the risk materializes. The best-performing models are those regarding the credit, house price, and debt burden variable categories. In contrast, external imbalances are those that have the greatest variation of results. This means that in modelling the financial stress regime-switching behaviour, it would be useful to include credit and debt burden variables with a 4-quarter lag.

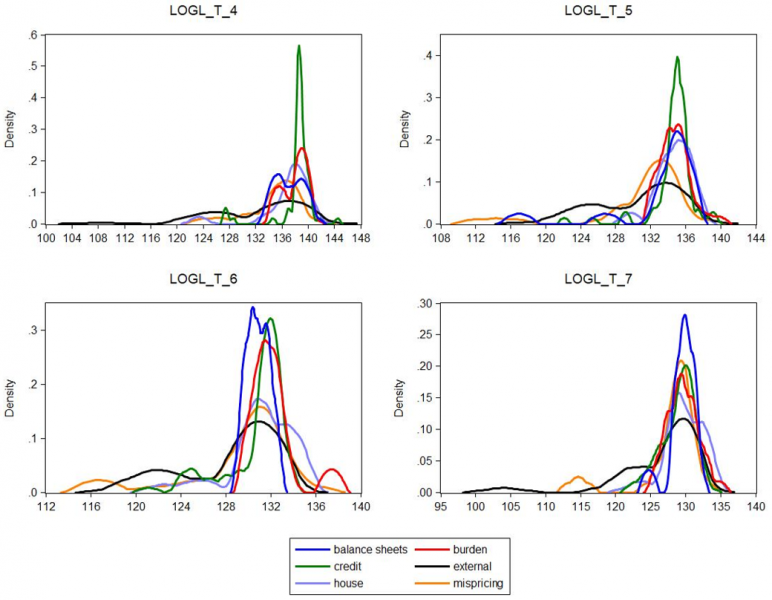

Figure 1: Empirical density functions of log likelihood values across all models

Note: “balance sheets”, “burden”, “credit”, “external”, “house” and “mispricing” denote the six categories of measures from table 1: strength of balance sheets, private sector debt burden, credit dynamics, external imbalances, potential overvaluation of house prices and mispricing of risks respectively. t_4, t_5, t_6 and t_7 denote models that include indicator variables lagged for 4, 5, 6 and 7 quarters respectively. Source: Author’s calculation.

Not all variables are best performing for the t-4 case, which is seen in figure 1. It observes the empirical density functions of each risk category for all four lags observed in the study. This helps determine which lag could be best for a variable category, or individual variables when deciding which variant it is best to use in practice. This figure tells the following for the credit series as we move from t-7 to t-4, the density function becomes tighter with higher peaks. However, the best performance is found for t-5 for the balance sheets category, as here, most of the observations are above the value of 132, with a high peak, compared to higher peaks of lower values for t-6 and t-7 cases. Other measures have the best performance for t-4 and t-5 for the house prices category; the external and mispricing categories have the worst performances overall, due to high dispersion, especially regarding the left tails.

To summarize the results, it is evident that the performance of the models gets better when the lag of the indicator variable gets smaller. There is a trade-off, however, as the information about some variables has a certain lag. The results found here are in line with previous literature. Credit dynamics is found to be the best predictor of financial crises in previous literature (Borio and Lowe, 2002; Borio and Drehmann, 2009; Aldasoro, Borio and Drehmann, 2018), with newer studies including Schularick and Taylor (2012), alongside Drehmann and Juselius (2014), where the debt service to income ratio is one of the best early warning indicators, as found in this study. The private sector debt burden category is relevant, as found by Detken et al. (2014), or Giese et al. (2014). Moreover, the mispricing and external imbalances categories were found to have poor performance, as found in Slingenberg and de Haan (2011). The reasoning could be found in the poor performance of the stock market index, which has had little dynamics in the last 10-12 years.

The house price-to-income ratio significance in this study is in line with Anundsen et al. (2016), who also found that the higher the value of this ratio, the more the probability of financial crisis increases. Although the results of this study are aligned with this mentioned research, it should be noted that the comparisons are made on a broader scale, i.e., this research looks at the effects of individual indicators on risk probabilities. In contrast, most of the work mentioned looks at the values of financial stress. As it is difficult to predict future values of financial stress, as the mentioned literature agrees, this research has the advantage of predicting just higher or lower stress regime probability, not actual values of financial stress.

Consequences for policymakers are as follows. The results show that some indicators of cyclical risk accumulation provide information about future financial stress dynamics. The policymaker could use this information to narrow the most important indicators that need to be tracked over time and, consequently, tailor policies that would mitigate those risks. Although CNB had timely measures that focused on the majority of the risk indicators over the entire observed period, better coordination among macroprudential, monetary and fiscal policies is needed to achieve healthier economic growth. As some asymmetry in results is found, this indicates that the tightening and loosening policy should not be considered similarly.

As Kauko (2014) observes, most of research on EWS utilizes binary variables as the dependent ones in the analysis. As crises rarely occur, meaning that not many observations are included in the regime of crisis occurrence, the combination of financial stress data as the dependent variable can be helpful. Macroprudential policymakers could use results from this study to track specific indicators in greater detail and try to estimate the stance concerning the instruments used over the observed period and the goals set during the boom-and-bust phases of the financial cycle. The Croatian case showed that the policymakers had a good focus on specific problems that were occurring during the entire observed sample. Most tightening and loosening measures were tailored according to some of the indicators found to be the best-performing ones in this study.

Alessi, L. and Detken, C., 2019. Identifying excessive credit growth and leverage. Journal of Financial Stability, 35. pp. 215-225. https://doi.org/10.1016/j.jfs.2017.06.005.

Ang, A. and Timmermann, A., 2012. Regime changes and financial markets. Annual Review of Financial Economics, 4, pp. 313-337. https://doi.org/10.11 46/annurev-financial-110311-101808.

Anundsen, A. K. [et al.], 2016. Bubbles and crises: The role of house prices and credit. Journal of Applied Econometrics, 31, pp. 1291-1311. https://doi.org/10.1002/jae.2503.

Borio, C. and Drehmann, M., 2009. Assessing the Risk of Banking Crises – Revisited. BIS Quarterly Review, (March), pp. 29-46.

Borio, C. and Lowe, P., 2002. Asset prices, financial and monetary stability: exploring the nexus. BIS Working Papers, No. 114. https://doi.org/10.2139/ssrn.846305.

Candelon, B., Dumitrescu, E-I. and Hurlin, C., 2012. How to Evaluate an Early-Warning System: Toward a Unified Statistical Framework for Assessing Financial Crises Forecasting Methods. IMF Economic Review, 60, pp. 75-113. https://doi.org/10.1057/imfer.2012.4.

Cardarelli, R., Elekdag, S. and Lall, S., 2011. Financial stress and economic contractions. Journal of Financial Stability, 7(2), pp. 78-97. https://doi.org/10. 1016/j.jfs.2010.01.005.

CNB, 2022. Statistical data. Zagreb: Croatian National Bank.

Davis, E. P. and Karim, D., 2008. Comparing early warning systems for banking crises. Journal of Financial Stability, 4(2), pp. 89-120. https://doi.org/10. 1016/j.jfs.2007.12.004.

Detken, C. [et al.], 2014. Operationalising the countercyclical capital buffer: indicator selection, threshold identification and calibration options. ESRB Occasional Paper, No. 2014/5. https://doi.org/10.2139/ssrn.3723336.

Doz, C., Ferrara, L. and Pionnier, P., 2020. Business cycle dynamics after the Great Recession: An extended Markov-Switching Dynamic Factor Model. OECD Statistics Working Papers, No. 2020/01. https://doi.org/10.1787/9626dda3-en.

Drehmann, M. and Juselius, M., 2012. Do debt service costs affect macroeconomic and financial stability? BIS Quarterly Review, September 2012.

Duprey, T. and Klaus, B., 2017. How to predict financial stress? An assessment of Markov switching models. ECB Working Paper, No. 2057. https://doi.org/10.2139/ssrn.2968981.

ESRB 2018. The ESRB handbook on operationalising macroprudential policy in the banking sector. European Systemic Risk Board.

ESRB, 2014. Recommendation of the European Systemic Risk Board of 18 June 2014 on guidance for setting countercyclical buffer rats (ESRB/2014/1). Official Journal of the European Union C 293/1.

Giese, J. [et al.], 2014. The credit-to GDP gap and complementary indicator for macroprudential policy: evidence from the UK. International journal of finance and economics, 19(1), pp. 25-47. https://doi.org/10.1002/ijfe.1489.

Giglio, S., Bryan, K. and Pruitt, S., 2016. Systemic Risk and the Macroeconomy: An Empirical Evaluation. Journal of Financial Economics, 119(3), pp. 457-471. https://doi.org/10.1016/j.jfineco.2016.01.010.

Gneitinga, T. and Ranjanb, R., 2011. Comparing Density Forecasts Using Threshold- and Quantile-Weighted Scoring Rules. Journal of Business and Economic Statistics, 29(3), pp. 411-422. https://doi.org/10.1198/jbes.2010.08110.

Kaminsky, G. L. and Reinhart, C. M., 1999. The Twin Crises: The Causes of Banking and Balance-of-Payments Problems. American Economic Review, 89(3), pp. 473-500. https://doi.org/10.1257/aer.89.3.473.

Kauko, K., 2014. How to foresee banking crises? A survey of the empirical literature. Economic Systems, 38(3), pp. 289-308. https://doi.org/10.1016/j. ecosys.2014.01.001.

Klomp, J., 2010. Causes of banking crises revisited. The North American Journal of Economics and Finance, 21(12), pp. 72-87. https://doi.org/10.1016/j.najef.2009.11.005.

Lang, J-H. [et al.], 2019. Anticipating the bust: a new cyclical systemic risk indicator to assess the likelihood and severity of financial crises. Occasional Paper Series, No. 219. https://doi.org/10.2139/ssrn.3334835.

O’Brien, M. and Wosser, M., 2021. Growth at Risk & Financial Stability. Financial stability notes, 2021(2)

Schularick, M. and Taylor, A. M., 2012. Credit booms gone bust: monetary policy, leverage cycles, and financial crises, 1870-2008. The American Economic Review, 1022, pp. 1029-1061.

https://doi.org/10.1257/aer.102.2.1029.

Slingenberg, J. W. and de Haan, J., 2011. Forecasting Financial Stress. De Nederlandsche Bank Working Paper, No. 292. https://doi.org/10.2139/ssrn.1951800.

Vermeulen, R. [et al.], 2015. Financial Stress Indices and Financial Crises. Open Economies Review, 26(3), pp. 383-406.

Vujčić, B. and Dumičić, M., 2016. Managing Systemic Risks in the Croatian Economy. BIS Paper, No. 861.