This paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

The last few decades have been accompanied by disruptive changes to the structure of employment within advanced economies. On the one hand, this has led increasing demand of jobs which requires high level of skills, an increase that Branko Milanović (2019) has described as a natural trait of meritocratic capitalism. On the other hand, this same process have led to deterioration in demand for middle-skill occupations, a process known as job polarisation. This process has twofold impact: it heterogeneously impacts on future income expectations and, additionally, it affects job insecurity conditionally on skill.

The connections between rising polarisation and income inequality have been thoroughly studied. However, it is unclear whether these changes in income across occupation classes can loop back into the credit system, and affect the lending behaviour of credit institutions, or whether this process impacts on the households’ self-assessment of their opportunities to borrow money. As the demand for middle-skill workers shrinks, expectations about household income though their lifetime horizon are adjusted. Practically, this is an unexpected downwards adjustment of permanent income and it changes individuals’ as well as finance institutions’ assessment of individual’s future income. This has an impact on both applying for a loan and it being granted. This is the result of the European Central Bank Working Paper “Job polarisation and household borrowing” by Michele Cantarella (University of Helsinki) and Ilja Kristian Kavonius (European Central Bank and University of Helsinki), in which the process of job polarisation affects credit demand and supply is studied, focusing on its relationship with credit constraint and credit quality. The result is significant as it finds another mechanism fostering increasing inequality. As Sen (2000, p. 13) has pointed out “not having access to the credit market can, through causal linkages, lead to other deprivations such as income poverty, or the inability to take interesting opportunities that might have been both fulfilling and enriching but which may require an initial investment and use of credit”.

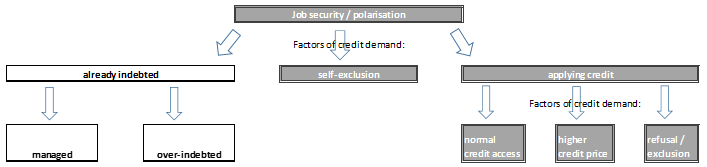

Increased job insecurity and job polarisation can lead to credit constraint in three ways, which are illustrated in Figure (1.). First, the household might already be indebted. If the increased insecurity is unexpected, the level of indebtedness is either such that the household can maintain the existing credit or it is not able to amortise it, i.e., the household is over-indebted. In our current research, we are not focusing on these households, which are indicated with a white in the figure, and these aspects will be focus of the second part of project. Second, the household needs either additional or new credit, but decides not to apply for it as the household believes that the credit application will fail. The former scenario is indicated in Figure 1 as self-exclusion. In the last scenario, the household enters the credit market instead. In this case, there are three possible outcomes. First, the household has normal access to the credit markets and obtains the requested amount of credit. Second, that the household receives credit but with higher interest than the average household or receives less than initially requested. Third, the bank refuses to issue credit to the household. This second part, which is highlighted with grey in the graph, is also focus of this study.

Figure 1: A sketch of the possible relationship between job security, polarisation and credit behaviour.

The starting point of the analysis is the permanent income hypothesis (Friedman, 1957). According to Friedman, consumption and, by extension, saving, is determined by long-term considerations, so that any transitory changes in income lead primarily to additions to assets or to the use of previously accumulated balances rather than to corresponding changes in consumption. To know how much transitory changes impact consumption the growth in income, consumption and wealth should be followed over a lifetime (Boushey, 2019). This also implies that if there is an unexpected shock in the income then adjustment of absolute consumption and savings can be expected.

The concept of job polarisation is relevant in this context, as recent decades have shown the deterioration of middle-skill jobs (see Autor, 2019; Fernández-Macías and Hurley, 2016; Goos et al., 2009) and the consequent rise of income inequality. We intend to test whether job security and job polarisation can affect income expectations in the long run, and in turn affect access to credit. The key mechanism in the problems in financing is job polarisation. The problems in financing are defined in this paper from three perspectives: (1.) from the households’ own demand for credit and self-exclusion from credit; (2.) from the willingness of financial institutions to supply credit, and; (3.) from the quality of credit and terms of borrowing themselves.

The contrast between perceived job security and polarisation is also relevant in the context of information asymmetries, which can play a role in credit access (Stiglitz and Weiss, 1981). When requesting credit, household will disclose their occupation status, but not their idiosyncratic job security. Comparing how much job polarisation and security differ in terms of credit access and supply can provide a measure of these asymmetries and how well banks can compensate for the lack on information on job stability beyond income, tenure and employment status information.

The analysis of this paper is based on two data sources: Household Consumption and Finance Survey (HFCS) and Labour Force Survey (LFS). These two data sources are linked and the job polarisation indicators are based on the LFS. The short-term (five years) job polarisation are analysed at the ISCO-08 two-digit level and the medium-term job polarisation at the ISCO08 one-digit level. Access to finance and job security are analysed by using specific variables defined for the issues in the HFCS. We analyse the inter-relation of job polarisation and access to finance/job insecurity by defining two regression models: a naive model, and a self-selection one.

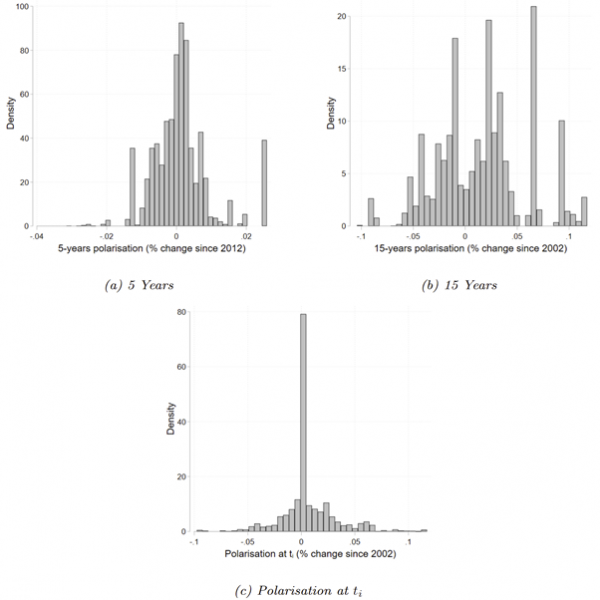

The fundamental difference of the two models is that in the naive model we assume that the job polarisation is an exogenous factor, i.e., that the household is not able to control it. The second model instead controls the self-section issue caused by individuals self-selecting into occupations that were already experiencing polarisation. Figure 2 shows this phenomenon in action: over the last 15 years since 2017, a non-negligible amount of individuals entered jobs whose share in the economy has been growing or decreasing in a substantial way.

Figure 2: Frequency histograms of 5 (a) and 15 (b) years polarisation, relative to the total employment in each country in 2012 and 2002, and (c) polarisation on the year the individual started their last job.

The paper finds medium-term polarisation to prevail over long-term polarisation when it comes to demand and supply of household debt. Our results indicate that, overall, for every 1% decrease in weekly hours in a given occupation over the last five years, equal (on average) to 25,000 full time jobs, the probability of a household (whose head is employed in that occupation) being refused credit increases by 0.7%. This happens regardless of the financial situation of the household, and holding the total number of jobs in an economy as fixed, meaning that these constraints are entirely generated by expectations on changes in labour demand. We found job polarisation to be largely unrelated to perceived job security, with the former playing a larger role for credit supply, and the latter prevailing in terms of credit demand. Another shorter analysis by using the first model and the same data set was published in a publication of the Finnish Economic Association (Cantarella and Kavonius 2022b). The results for Finland indicate that this relation between job polarisation and access to finance is not evident. This is likely related to the absence of informational asymmetries in the context of job stability, as the banks in Finland are not using credit-scoring models and have direct access to the individual’s tax files. Thus, there is no need to proxy the financial situation of the loan applicants.

Autor, D. H. (2019). Work of the past, work of the future. AEA Papers and Proceedings, 109:1–32.

Boushey, H. (2019). Unbound: how inequality constricts our economy and what we can do about it. Harvard University Press, Cambridge, Massachusetts London, England.

Cantarella, M., & Kavonius, I. K. (2022). Job polarisation and household borrowing. (Working paper series – European Central Bank; No 2683). European Central Bank. https://doi.org/10.2866/092600

Cantarella, M., & Kavonius, I. K. (2022b). Työmarkkinoiden polarisaatio ja kotitalouksien lainanotto. Kansantaloudellinen Aikakauskirja, 118(1), 62-77. https://www.taloustieteellinenyhdistys.fi/wp-content/uploads/2022/02/31871983_KAK_1_2022_Taloustieteellinen_Yhdistys_WEB-64-79.pdf

Fernández-Macías, E. and Hurley, J. (2016). Routine-biased technical change and job polarization in Europe. Socio-Economic Review, 15(3):563–585.

Friedman, M. (1957). A Theory of the Consumption Function. National Bureau of Economic Research, Inc.

Goos, M., Manning, A., and Salomons, A. (2009). Job polarization in Europe. American Economic Review, 99(2):58–63.

Milanović, B. (2019). Capitalism, alone: the future of the system that rules the world. The Belknap Press of Harvard University Press, Cambridge, Massachusetts.

Sen, A. (2000). Social exclusion : concept, application, and scrutiny. Office of Environment and Social Development, Asian Development Bank, Manila, Philippines.

Stiglitz, J. E. and Weiss, A. (1981). Credit rationing in markets with imperfect information. The American Economic Review, 71(3):393–410.