We evaluate the consequences of super-active fiscal policy rules – rules that call for tax cuts and/or spending increases as the government’s debt level rises. When monetary policy is constrained by the zero lower bound (ZLB) on nominal interest rates, such a seemingly irresponsible, debt-financed fiscal stimulus, unbacked by any promise of future tax increases or spending cuts, not only improves economic stability by acting as an automatic stabilizer, but also, somewhat paradoxically, reduces government debt accumulation. When evaluated using a model-consistent measure of welfare, fiscal rules calibrated to the U.S. response during both the Great Recession and COVID recession, combined with a weak monetary policy response to inflation, outperform a monetary policy that responds strongly to inflation and reduce the frequency of episodes at the ZLB.

During the years between the global financial crisis of 2008-09 and the COVID-19 pandemic of the past two years, central banks faced limitations on using the traditional tool of monetary policy due to the zero lower bound (ZLB) on nominal interest rates. In the case of Japan, the limited ability of monetary policy to stimulate the economy dates back even further. While the recent surge in inflation due to COVID-19 disruptions and the Russian invasion of Ukraine has shifted attention away from ZLB concerns, the general consensus that average real returns have fallen over the past two decades suggests that the ZLB is likely to hinder monetary policy in the future.

If so, it may be necessary to rethink macroeconomic stabilization policies and go beyond minor adjustments to the policy framework of central banks by investigating whether fiscal policy could, and should, play a more prominent role in controlling inflation. At the ZLB, monetary policy may be constrained, but fiscal policy is not.

To that end, in a recent paper (Billi and Walsh 2022), we consider the implications of reversing the respective roles of monetary and fiscal policy. Rather than have the central bank charged with controlling inflation while the fiscal authority passively adjusts taxes and/or spending to ensure debt sustainability, we ask how the economy behaves if fiscal policy follows rules that, on their face, appear to be irresponsible – cutting taxes and/or increasing spending when debt levels rise. We call these super-active fiscal policies.

Consider what happens in the face of a severe contraction in aggregate demand that pushes output and inflation down. The lower inflation increases the real interest payments on the debt. A responsible fiscal policy would raise taxes or cut spending rather than simply borrowing to finance the higher interest payments. The fiscal rules we consider would call for the reverse – tax cuts or spending increases. Debt financed tax cuts, for example, would increase households’ disposable income without creating any expectations that taxes will be raised to pay off the additional borrowing. With higher income, households increase spending. The resulting boost to aggregate demand helps the economy recover, pushing up output and inflation.

For super-active fiscal policies to have these effects, they must be combined with a weak monetary response as inflation rises to ensure the recovery is not choked off. The central bank must violate the Taylor principle – the classic prescription for sensible monetary policy that dictates central banks should lower (or raise) interest rates more than one-for-one with declines (increases) in inflation.

One example of an active fiscal policy is a rule that adjusts neither net taxes nor government purchases in response to deviations of debt from its steady state. A contractionary shock to the economy that pushes output and inflation down causes an increase in the real value of the government’s nominal outstanding debt. With no fiscal response to raise taxes or cut spending, the public holds more debt in real terms but faces no future tax increases to repay the debt. The public sees itself as better off and so consumption increases. This stimulates output and causes inflation to rise, exactly the response one wants when the economy is in a recession at the ZLB.

A super-active fiscal policy goes one better by cutting taxes or raising spending as the debt level rises. At the ZLB, this supercharges the consumption increase, helping to get output back to normal and inflation back up to target.

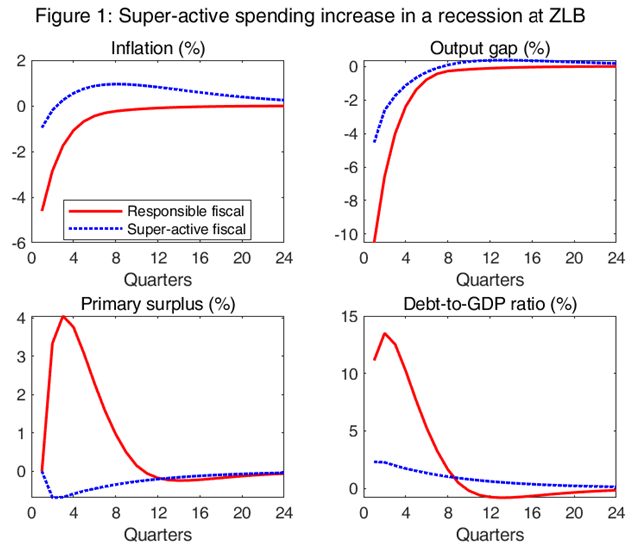

We illustrate in Figure 1 how the economy responds to a severe contractionary demand shock, pushing the economy into a ZLB episode, in the two different policy scenarios described above – responsible fiscal policy and super-active fiscal policy. In the case of a responsible fiscal policy (solid red lines), output and inflation fall and so the government must increase taxes or cut spending to finance the higher interest payments on its outstanding debt. Nonetheless, the debt-to-GDP ratio rises due to the sharp fall in GDP. Instead, a super-active fiscal policy (dashed blue lines) that increases spending as the debt level rises pushes up output and inflation, resulting in a mild overshooting of inflation during the economic recovery. This super-active fiscal policy dampens the fall in output and produces a smaller increase in the debt-to-GDP ratio than the responsible fiscal policy.

Notes: The figure reproduces some of the simulations from our paper Billi and Walsh (2022). In particular, the solid red lines show the model economy’s outcome in the presence of the ZLB under an active monetary and passive fiscal policy (so-called policy regime M in our paper). The dashed blue lines show the outcome in the presence of the ZLB under a passive monetary and super-active fiscal policy in which the government increases spending when the debt level rises (scenario G in our paper).

A rule-based, active fiscal policy – that is, a credible commitment to behave in ways that to many academics and policymakers would appear to be irresponsible and shortsighted – can endogenously generate movement in expected inflation that stabilizes the economy. This is an advantage if, due to the ZLB, monetary policy’s response is limited. However, the economy is likely to experience periods when the ZLB binds and periods when it doesn’t. Even if a super-active fiscal policy performs best when at the ZLB, it may perform much worse when the ZLB is not a constraint on monetary policy. Thus, a welfare comparison of whether monetary policy or fiscal policy should be active will depend on their relative performances both at the ZLB and away from it and on the frequency with which the ZLB occurs under each policy alternative.

We carry out such a welfare comparison employing a model-consistent measure of the welfare costs of fluctuations. When we calibrate our model to match the observed frequency of episodes at the ZLB to that observed for the U.S., we find the superior performance of super-active fiscal policy at the ZLB more than offsets its poorer performance when the ZLB does not limit monetary policy. This remains the case when the steady-state debt level is increased and when the government issues long-term debt. However, super-active fiscal policies are most effective with a high debt level and when debt is short-term. The normative assessment suggests that both the existing literature and policy discussions based on conventional wisdom have focused too exclusively on the role of active monetary policies in the face of the ZLB.

One reason super-active fiscal policies work well is because such policies reduce time spent at the ZLB. When monetary policy is relied on to promote macroeconomic stability, the central bank cuts interest rates aggressively in the face of a severe contractionary shock. This is just what the Fed did during the Global Financial Crisis and in the face of the COVID-19 shock. But when rates are cut in this way, the economy quickly ends up at the ZLB, at which point, the effectiveness of monetary policy is limited. However, with super-active fiscal policies, monetary policy needs to respond weakly, cutting rates less. As a consequence, the economy is much less likely to end up at the ZLB. In simulations in which the contractionary shock is calibrated so that the economy ends up at the ZLB 25 percent of the time under a standard monetary policy rule that follows the Taylor principle, the frequency of the ZLB falls to less than 12 percent under super-active fiscal policies.

In our research, we also calibrate the fiscal rules to reflect the size of the fiscal responses seen in the U.S. during the Great Recession and the COVID recession. We show that these super-active fiscal policies are effective in stabilizing inflation and output in the face of the ZLB.

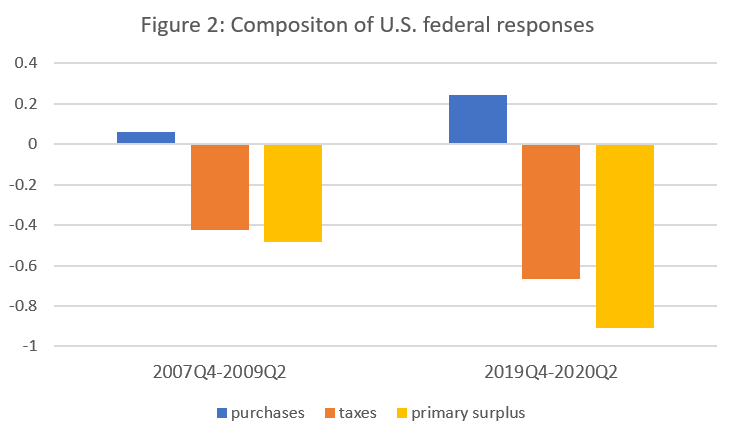

During both the Great Recession that followed the 2008-09 global financial crisis and the COVID induced recession of early 2020, large fiscal expansions occurred accompanied by increases in debt-to-GDP levels. As is well-known, the U.S. federal debt held by the public as a percent of GDP has been rising steadily since 2007; it was 35% at the start of the Great Recession (2007Q4) and had risen to 80% at the onset of the COVID recession (2019Q4).

To illustrate the size and composition of the U.S. federal response during these recessions, Figure 2 shows the change in government purchases and net taxes as a share of GDP, divided by the change in debt as a share of GDP. Also shown is the change in the primary surplus (net taxes minus purchases) relative to the change in debt. The bars on the left refer to the fiscal response during the Great Recession (2007Q4 to 2009Q2), while the bars on the right show the response in the COVID recession (2019Q4 to 2020Q2). The fiscal response in the U.S. during the Great Recession primarily took the form of tax cuts and increases in transfers, with the fall in net taxes equaling 42% of the rise in debt. Government purchases (consumption plus investment) rose by only 6% of the change in debt, implying the primary surplus fell by 48% of the rise in debt. During the COVID recession, the fiscal response measured relative to the debt level was larger overall, with the primary surplus falling by 91% of the rise in debt and with the debt level at the end of 2019 much higher than during the Great Recession. Government purchases rose notably more during COVID (24% of the rise in debt) and cuts in net taxes were larger (67% of the rise in debt) compared to the previous recession.

Accounting for the ZLB, the welfare costs of fluctuations under these policies are slightly lower than achieved by active monetary policy. The fiscal response during the Great Recession was concentrated on tax cuts and transfer increases, while that in 2020 during the COVID pandemic represented a more balanced increase in purchases and reduction in net taxes. Comparing outcomes under the COVID policy to those under the Great Recession policy when the economy experiences the same contractionary shock, the COVID response reduced inflation volatility and resulted in a welfare improvement relative to the Great Recession fiscal response. Both examples of super-active fiscal policies are particularly effective if they are combined with a passive monetary policy that pegs the nominal interest rate to its steady state, eliminating the occurrence of the ZLB.

Notes: The data source is the Federal Reserve Bank of St. Louis FRED database (https://fred.stlouisfed.org). The variables used (and their FRED identifiers) are the following: U.S. federal government receipts (FGRECPT), expenditures (FGEXPND), interest payments (A091RC1Q027SBEA), transfer payments (W014RC1Q027SBEA), debt held by the public as a percent of GDP (FYGFGDQ188S), and GDP (GDP). Net taxes are equal to receipts minus transfers, while government purchases are equal to expenditures minus transfers minus interest payments. The primary surplus is equal to net taxes minus government purchases. For example, the bar shown for government purchases is given by (g(end) – g(start))/(debt(end) – debt(start)), where g and debt are expressed as a percent of GDP and where `start’ and `end’ refer to the quarter in which the recession begins and ends.

Have there been examples of super-active fiscal policies? Jacobson, Leeper, and Preston (2019) cite President Franklin Roosevelt’s distinction during the Great Depression between the regular budget and the 1933 temporary emergency budget. The regular budget was governed by conventional budget-balancing concerns; in contrast, there was no promise that future taxes would be raised to fund the deficit created by the temporary emergency budget. Thus, the emergency budget of 1933 was an example of an active fiscal policy, and Jacobson, Leeper, and Preston argue that the emergency budget helped generate the recovery of 1933. The emergency budget represented the type of unfunded fiscal expansion that Sims (2016) called for as necessary at the ZLB to replace ineffective monetary policy.2

A large literature has investigated active fiscal policies in which taxes are not raised enough or spending is not cut enough when debt levels rise to ensure the debt remains sustainable. Prominent contributions include Leeper (1991), Jacobson, Leeper, and Preston (2019), and the survey by Leeper and Leith (2016). We find that seemingly irresponsible super-active policies, policies that cut taxes or increase spending as debt levels rise, can outperform monetary policy at the ZLB while also reducing the occurrence of ZLB episodes.

These results depend critically on the ability of the fiscal authority to credibly commit to rules that call for it to behave in ways that seem irresponsible. The literature commonly assumes central banks can commit to rules. If fiscal authorities can also commit, our findings call into question the traditional view that an independent central bank should focus on maintaining low inflation and supporting macro stability while the fiscal authority should follow responsible rules to ensure debt sustainability. When the ZLB is a frequent concern, fiscal policy can contribute to economic stability by running, in the words of Chris Sims (2016), “deficits aimed at, and conditioned on, generating inflation. The deficits must be seen as financed by future inflation, not future taxes or spending cuts.”

The effects of super-active fiscal policy operate through the effects of inflation on the real value of the government’s nominal debt. This means our analysis applies only to governments that can issue debt in their own currency. The flip side of the fiscal rules we analyzed requires the fiscal authority to raise taxes and/or cut spending when, as currently, increases in inflation reduce the real outstanding value of debt. Thus, governments would need to credibly commit to not spending the revenue they earn from the inflation tax. Achieving such credibility may not be easy.

Bianchi, Francesco, Renato Faccini, and Leonardo Melosi. 2020. “Monetary and Fiscal Policies in Times of Large Debt: Unity Is Strength.” NBER Working Paper 27112.

Billi, Roberto M., and Carl E. Walsh. 2022. “Seeming Irresponsible but Welfare Improving Fiscal Policy at the Lower Bound.” Sveriges Riksbank Working Paper No. 410.

Jacobson, Margaret M, Eric M Leeper, and Bruce Preston. 2019. “Recovery of 1933.” NBER Working Paper 25629.

Leeper, Eric M. 1991. “Equilibria under ‘Active’ and ‘Passive’ Monetary and Fiscal Policies.” Journal of Monetary Economics 27 (1): 129–47.

Leeper, Eric M., and Campbell Leith. 2016. “Understanding Inflation as a Joint Monetary-Fiscal Phenomeon.” In Handbook of Macroeconomics, edited by John B. Taylor and Harald Uhlig.

Sims, Christopher A. 2016. “Fiscal Policy, Monetary Policy and Central Bank Independence.” Federal Reserve Bank of Kansas City Jackson Hole Symposium, 1–17.

Contacts: Roberto M. Billi, Advisor, Sveriges Riksbank, roberto.billi@riksbank.se; Carl E. Walsh, Distinguished Professor Emeritus, University of California, Santa Cruz, walshc@ucsc.edu.

Bianchi, Faccini, and Melosi (2020) analyze temporary shock-specific polices (emergency budgets and temporary inflation targets) that can also be interpreted as capturing Roosevelt’s distinction between the regular and emergency budgets.