In Gradzewicz (2022) we aim to identify the granular demand and productivity shocks, their properties, and the firm-level responses of the important variables to these shocks. We use comprehensive data from the Polish enterprises from years 2002-2019 that cover almost 80% of employment in the enterprise sector. We show that the distributions of the two shocks differ: i.e., supply (productivity) shocks are symmetrically distributed, and the distribution of demand shocks is negatively skewed, but both have fat tails. Productivity shocks have more persistent effect on firms’ outcomes than demand shocks. We find that following demand shocks, there are short-lived increases in output, market share, productivity, real wages, and markups, whereas investment and employment demand remain elevated for a longer period. We also find a very limited transmission of productivity into wages, and we showed that proxies for prices increase after demand shocks, and they decrease after the supply shock, in a theory-consistent way.

Most of the existing literature uses macroeconomic data and macroeconomic identification schemes (like structural vector autoregressions or dynamic factor models) to derive the dynamic responses of economic variables to demand or supply shocks. Following the routes pioneered by Cochrane (1994), in Gradzewicz (2022) we try to identify the impulse-responses on a granular level: using the reactions of individual firms to supply (productivity) and demand shocks, both measured at a firm level. Our results can be seen as a cross-check for the impulse responses identified using macroeconomic models, as stressed by Buera et al. (2021). Moreover, we describe the properties of distributions of these shocks. The studies that are the closest to ours are Pozzi and Schivardi (2016) and Carlsson et al. (2021), but our approach stresses the dynamic nature of impulse-responses and provides additional insights into the properties of shocks and of firms’ adjustment mechanisms.

We use the shock identification scheme proposed by Kumar and Zhang (2019), where the uncertainty about the demand schedule create a gap between the expected and the realized sales and introduce a time variation in inventories, which allows to pin down the demand shock. The identification of supply (productivity) shocks utilizes the control function approach pioneered by Olley and Pakes (1996). We additionally adjust the specification to addresses the issues raised in the recent literature, for example controlling for the demand conditions (which is stressed by Doraszelski and Jaumandreu, 2021) and including a firm’s market share (which addresses the critique in Bond et al., 2020).

In the empirical part of the paper we use a comprehensive dataset of all firms from Poland with more than nine employees, covering the 18-year period (2002-2019). The dataset covers more than 80% of employment and 70% of output output in the enterprise sector. This rich dataset allows us to derive findings that are representative from a macroeconomic perspective.

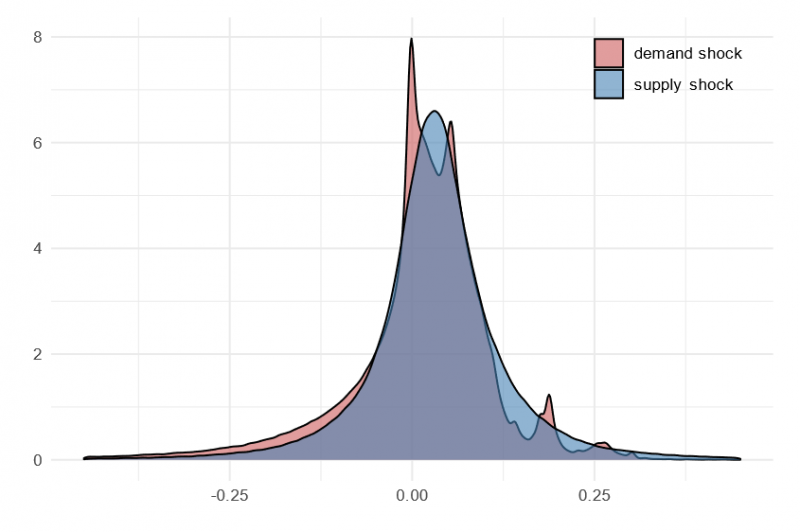

We show that the distributions of both shocks differ significantly (see Figure 1). The distribution of the demand shocks is centered at zero, while the supply shocks are centered at 4%, which indicates that demand shocks have redistributive effects whereas supply shocks have both redistributive and growth effects. The distribution of demand shocks is more dispersed and both have very fat tails. The two distributions also differ in terms of skewness, as the productivity shocks are symmetrically distributed, whereas the demand shocks are negatively skewed. Moreover, the demand shocks are persistent, while the autocorrelation of the supply shocks is essentially zero. The two shocks are essentially uncorrelated. The relative volatility of a supply shock to output volatility, measured on a firm level is higher than for demand shocks, indicating their relatively more important role in explaining the time variation of the firm-level output growth.

Figure 1. Densities of demand and supply shocks

Having derived the productivity and demand shocks, we use the local projection method pioneered by Jorda (2005) to estimate the responses of variables related to firms’ reactions to these shocks. It allows us to extract robustly estimated dynamic impulse-responses, which can be interpreted analogously to their counterparts derived using macroeconomic tools.

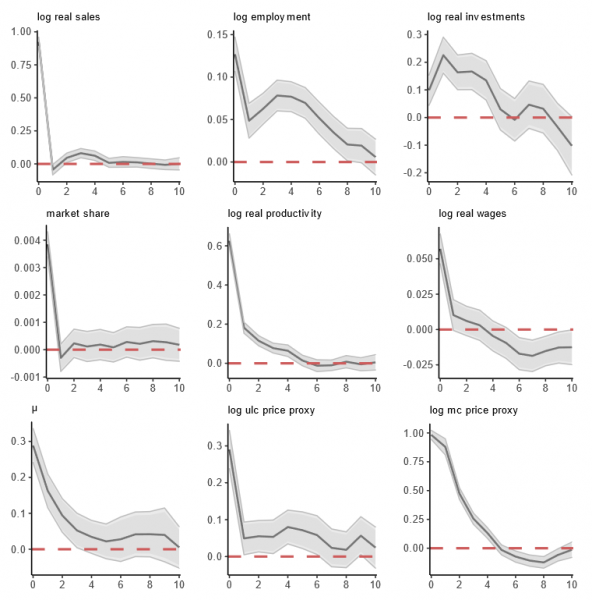

Figure 2. Responses to demand shocks

Notes: The dark and light gray areas represent 90% and 95% confidence intervals, respectively. The horizontal axis is expressed in years. μ denotes a measure of firm-level markups.

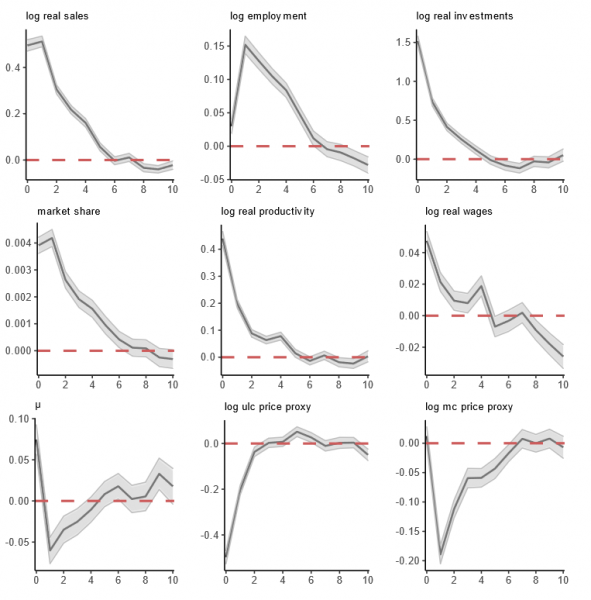

Figure 2 and Figure 3 displays the responses of a set of variables to a one-period positive firm-level demand and supply shock, respectively. There are both notable differences and similarities between them. First, our empirical results indicate that the changes in firms’ outcomes are much more persistent in response to productivity shocks than to demand shocks. Second, demand shocks result in short-lived increases in output, market share, productivity, real wages, and markups (μ, measured using De Loecker, Warzynski, 2012); and in increases in investment and employment for a couple of periods. The proxies for prices (we do not observe individual prices in the dataset, and we proxy for them using marginal costs and markups) tend to rise, generating a positive output-price correlation, as is expected after a demand shock. Third, firms’ reactions to supply shocks are qualitatively similar, but they are more persistent. Moreover, the proxies for prices tend to decrease temporarily after the supply shock, generating a negative output-price correlation, as predicted by macroeconomic models. Fourth, regardless of the nature of the shock, the resulting increases of labor productivity only partially translate into higher wages. The short-term passthrough of productivity into wages is close to 0.1 after a demand shock and is even smaller for a productivity shock. Fifth, the reaction of employment is prolonged in time, especially after a supply shock, indicating the importance of labor market rigidities and employment protection, which is quite strong in Poland (as measured by the OECD indicators).

Figure 3. Responses to supply shocks

Notes: The dark and light gray areas represent 90% and 95% confidence intervals, respectively. The horizontal axis is expressed in years. μ denotes a measure of firm-level markups.

Our main results are robust to significant changes in the identification scheme (including the definition of capital, the supply shock, shape of the production function and the sample selection), although there could be some uncertainty in the magnitudes of some of the responses, especially in case of employment.

The differences we found in the persistence of both shocks and responses to shocks are consistent with the results of many macroeconomic models (in which the persistence of the technology shocks is usually assumed in the calibration, like, e.g., in the canonical DGSE models, see Smets and Wouters, 2003). The behavior of markups, which rise (at least initially) after both a positive demand and a positive supply shock, is consistent with the findings of Nekarda and Ramey (2020) who used macroeconomic data to identify markups and their impulse responses. Moreover, a positive correlation between markups and market share, conditional on both demand and supply shocks that we found in the microeconomic data, is in line with sectoral oligopolistic models of the economy (see e.g. Burstein et al., 2020). The incomplete pass-through of productivity shocks to wages that we find was also stressed by Guiso et al. (2005), who attributed it to risk-sharing considerations.

The positive reactions of output and demand for production factors we observed are also consistent with the findings of many macroeconomic models. In addition, the other observations we made are in line with assumptions that are frequently found in macroeconomic models. In particular, our finding that markups increase after a productivity shock suggests that prices are sticky, as rising productivity does not fully translate into prices. By contrast, the limited impact of both productivity and demand shocks on wages we found is consistent with nominal wage rigidities. Moreover, the sluggish response of employment to both types of shocks points to the importance of labor market frictions, which are, for example, emphasized in search models.

Bond, S., A. Hashemi, G. Kaplan, and P. Zoch (2020): “Some Unpleasant Markup Arithmetic: Production Function Elasticities and Their Estimation from Production Data,” Working Paper 27002, National Bureau of Economic Research.

Buera, F. J., J. P. Kaboski, and R. M. Townsend (2021): “From Micro to Macro Development,” Journal of Economic Literature.

Burstein, A., V. M. Carvalho, and B. Grassi (2020): “Bottom-up Markup Fluctuations,” Working Paper 27958, National Bureau of Economic Research.

Carlsson, M., J. Messina, and O. Nordstrom Skans¨ (2021): “Firm-Level Shocks and Labour Flows,” The Economic Journal, 131, 598–623.

Cochrane, J. H. (1994): “Shocks,” Carnegie-Rochester Conference Series on Public Policy, 41, 295–364.

De Loecker, J. and F. Warzynski (2012): “Markups and Firm-Level Export Status,” American Economic Review, 102, 2437–2471.

Doraszelski, U. and J. Jaumandreu (2021): “Reexamining the De Loecker & Warzynski (2012) Method for Estimating Markups,” CEPR Discussion Papers DP16027, CEPR.

Gradzewicz, M. (2022): “How do firms respond to demand and supply shocks?,” NBP Working Paper No. 344, Narodowy Bank Polski.

Guiso, L., L. Pistaferri, and F. Schivardi (2005): “Insurance within the Firm,” Journal of Political Economy, 113, 1054–1087.

Jorda,O. (2005): “Estimation and Inference of Impulse Responses by Local Projections,” American Economic Review, 95, 161–182.

Kumar, P. and H. Zhang (2019): “Productivity or Unexpected Demand Shocks: What Determines Firms’ Investment and Exit Decisions?” International Economic Review, 60, 303–327.

Nekarda, C. J. and V. A. Ramey (2020): “The Cyclical Behavior of the Price-Cost Markup,” Journal of Money, Credit and Banking, 52, 319–353.

Olley, G. S. and A. Pakes (1996): “The Dynamics of Productivity in the Telecommunications Equipment Industry,” Econometrica, 64, 1263–1297.

Pozzi, A. and F. Schivardi (2016): “Demand or Productivity: What Determines Firm Growth?” The RAND Journal of Economics, 47, 608–630.

Smets, F. and R. Wouters (2003): “An Estimated Dynamic Stochastic General Equilibrium Model of the Euro Area,” Journal of the European Economic Association, 1, 1123–1175.