This policy brief documents patterns in the use of big data in Asian central banks, leveraging on a survey conducted among the members of the Irving Fisher Committee. Interest in big data appears particularly high in Asia, compared to central banks in other regions, including at the senior policy level. Big data is already used in a variety of areas, from research to monetary policy and financial stability, and Asian central banks use big data more extensively than their peers in most areas. The advent of big data, however, poses new challenges, with specific attention paid in the region to cyber security and data strategy. International policy cooperation, especially among public authorities in Asia, could help to facilitate the use of payments data and promote innovative technological solutions.

Central banks have shown an increasing interest in big data in recent years (Tissot 2017, Doerr et al 2021). Several central banks already use big data in a variety of areas, including monetary policy and financial stability as well as research and the production of official statistics. This trend is particularly pronounced in Asia: the share of Asian central banks currently using big data has almost tripled since 2015 and risen to nearly 90% by 2021.

This policy brief provides an overview of the use of big data and machine learning in Asian central banks, as well as associated challenges. Along the way, it establishes a comparison with the use of big data by their peers in other regions. The brief builds on recent research (Cornelli et al, 2022) and leverages on a survey conducted in 2020 among the institutional members of the Irving Fisher Committee on Central Bank Statistics (IFC) of the Bank for International Settlements (BIS).

Around 60% of central banks in Asia reported that they discuss big data issues extensively, a ratio that is significantly above the 42% observed in the rest of the world. Furthermore, all Asian respondents indicated a high to very-high level of interest at the senior policy level, compared to only 58% outside the region.

Big data is used in a variety of areas, including research as well as monetary policy and financial stability, and Asian central banks do so more extensively than their peers in almost all areas, with the exception of research purposes. In particular, they process non-traditional data to a greater extent to support monetary and financial stability policies – including for specific supervisory and regulatory purposes.

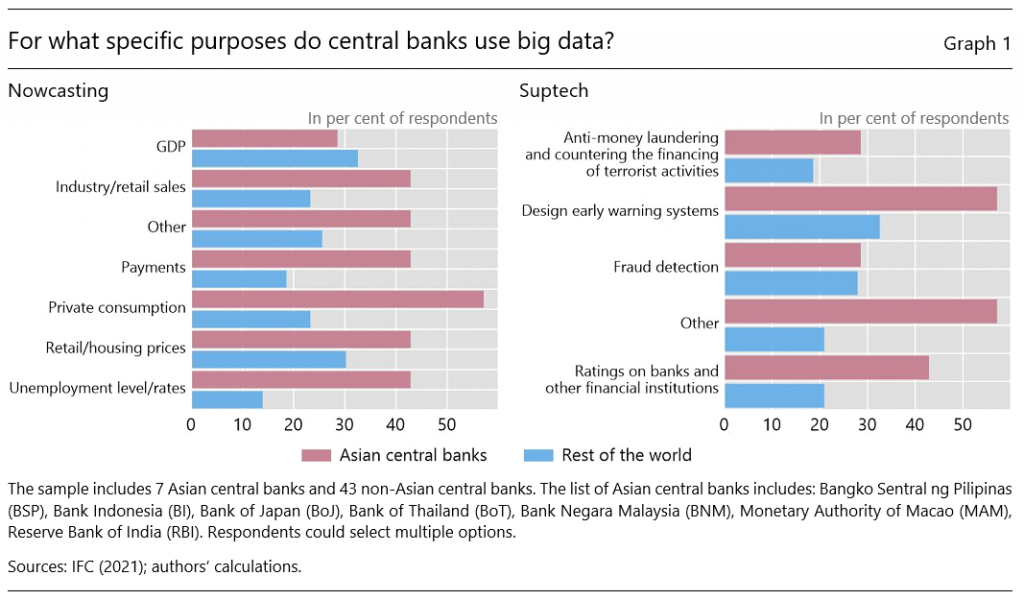

The big data projects undertaken by Asian central banks involve four main types of applications: Natural Language Processing (NLP), nowcasting exercises, applications to extract economy wide insight from granular financial data and other non-traditional sources, and suptech/regtech applications.

NLP is used, for example, to compute so-called economic policy uncertainty indices or to quantify the monetary policy stance that is communicated to the public via the publication of meeting minutes. Nowcasting models, used by more than 40% of Asian central banks (24% in the rest of the world) provide real-time information on eg private consumption, industry/retail sales, retail/housing prices, payments and unemployment conditions (Graph 1, left-hand panel). They can also help to fill statistical gaps, eg when reference series do not exist, are available only at a low frequency or are suddenly disrupted, as during the Covid-19 pandemic (De Beer and Tissot, 2020). To extract economy-wide insights, Asian central banks rely on granular financial data or other non-traditional sources of micro data. For instance, trade repositories’ records have helped identify networks of exposures in Thailand (Chantharat et al, 2017). Finally, suptech and regtech applications leverage big data to support micro-supervisory tasks (Graph 1, right-hand panel). Firm-level information gathered from financial statements or newspapers, for example, can be used to support early warning exercises or enhance credit scoring (mentioned by about 55% and 45% of Asian central banks, respectively).

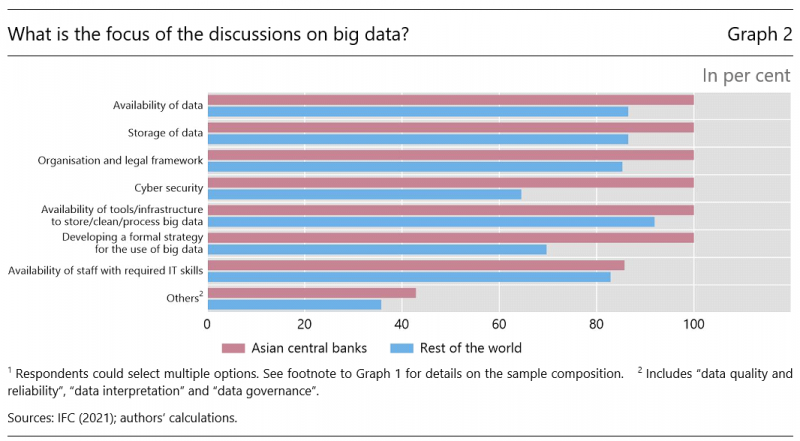

The use of big data poses various challenges, which are actively discussed by central banks in Asia (Graph 2, in red), especially in comparison to their counterparts in the rest of the world (in blue). All the Asian central banks considered mentioned that they have active discussions on a wide range of topics, such as the availability of IT infrastructure, legal, security and privacy issues, as well as the availability and strategic use of big data. Interestingly, cyber security and the development of a formal strategy for the use of big data are areas that Asian central banks discuss more actively than their counterparts in the rest of the world.

More specifically, the survey has highlighted four main challenges for Asian central banks in the use of big data. The first one consists in providing adequate computing power and software, which involves high up-front costs. Many central banks have, however, already undertaken important initiatives to develop big data platforms to facilitate the storage and processing of large and complex data sets. A reliable and safe IT infrastructure is a prerequisite not only for big data analysis, but also to prevent cyberattacks.

Second, central banks need to build up human capital to exploit big data. Yet the supply of data scientists is scarce and they are in high demand (Coeuré, 2020), in both the public and the private sector. The challenge is exacerbated by the difficulties to attract and retain talent, due to intense competition from the private sector.

A third group of challenges are the legal underpinning and ethical aspects for the use of private and confidential data. Reputational aspects may hinder the use of information sourced from the internet when little is known about its accuracy. For instance, web-based indicators such as search queries and messages on social media may not be representative of the real economy – not everybody is on Twitter, or only a subset of the CPI basket prices can be scraped from online stores. Related, much of the new big data is collected as a by-product of economic or social activities and needs to be curated before proper statistical analysis can be conducted.

Further, citizens might feel uncomfortable with the idea that central banks are scrutinising their search histories, social media postings or listings on market platforms. For example, in a representative survey, US consumers reported that they trust traditional financial institutions more to safely handle their data compared to government agencies, with big techs being the least trustworthy (Armantier et al, 2021). Similar patterns are present in Asian countries (Chen et al, 2021).

A fourth challenge is “algorithmic fairness”. This consideration can be less relevant for some tasks (eg nowcasting), but it may matter greatly for others (eg evaluating the suitability of regtech applications), and in general any application of machine learning that effects individuals would need to be subject to fairness validations.

Cooperation could foster central banks’ efficient use of big data, in particular through collecting and showcasing successful projects and facilitating the sharing of experiences. A promising area for collaboration in Asia could be in global payments data. More than 85% of central banks in the region (65% for the rest of the world) reported an active use of high frequency payment data in their institutions, with a primary focus on either the type of instruments, counterparties involved or both. One application could be to develop surveillance exercises with a focus on interconnectedness in the financial system.

International financial institutions can foster cooperation around big data. For instance, they can help develop in-house big data knowledge, in turn reducing central banks’ reliance on big data services providers, which can be expensive and entail significant legal and operational risks. Indeed, the IFC has been actively supporting such exchange of experience at the global level, and several complementary initiatives are being developed in the Asian region.

International bodies can also facilitate innovation by promoting technological solutions and initiatives to enhance the global statistical infrastructure. In this regard, the BIS Innovation Hub has identified as strategic priorities, among others, effective supervision (including regtech/suptech) and open banking/finance that could benefit from drawing on big data sources and tools.

Armantier, O, S Doerr, J Frost, A Fuster and K Shue (2021): “Whom do consumers trust with their data? US survey evidence”, BIS Bulletin, no 42.

Chantharat, S, A Lamsam, K Samphantharak and P Tangsawadirat (2017): “A new perspective on Thai household debt through credit bureaus’ big data”, PIER discussion paper, October.

Chen, S, S Doerr, J Frost, L Gambacorta and H S Shin (2021): “The fintech gender gap”, BIS Working Papers, no 931.

Coeuré, B (2020): “Leveraging technology to support supervision: challenges and collaborative solutions”, speech at the Financial Statement event series, Peterson Institute for International Finance.

Cornelli, G, S Doerr, L Gambacorta and B Tissot (2022): “Big data in Asian central banks”, IFC Working Papers, no 21.

Cornelli, G, S Doerr, L Gambacorta and B Tissot (forthcoming): “Big data in Asian central banks”, Asian Economic Policy Review.

De Beer, B and B Tissot (2020): “Implications of Covid-19 for official statistics: a central banking perspective”, IFC Working Papers, no 20.

Doerr, S, L Gambacorta and J M Serena (2021): “Big data and machine learning in central banking”, BIS Working Papers, no 930.

Irving Fisher Committee (2021): “Use of big data sources and applications at central banks”, IFC Report, no 13.

Tissot, B (2017): “Big data and central banking”, IFC Bulletin, no 44.

All authors are from the Bank for International Settlements (BIS). The views in this paper are those of the authors only and do not necessarily reflect those of the BIS nor the IFC and its members. This policy brief is based on the survey conducted by the IFC (IFC, 2021) and the analysis presented in Cornelli et al (2022). A more extensive and detailed version of the study is forthcoming in the Asian Economic Policy Review (Cornelli et al, forthcoming).