References

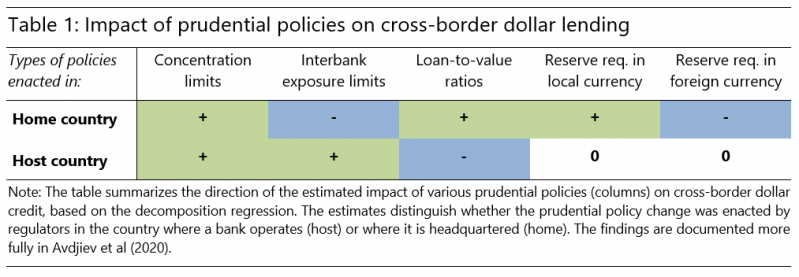

Avdjiev, S, B Hardy, P McGuire and G von Peter (2020) “Home sweet host: Prudential and monetary policy spillovers through global banks”, BIS Working Paper 853, https://www.bis.org/publ/work853.htm.

Avdjiev, S, McCauley, R, Shin, H S, (2016) “Breaking free of the triple coincidence in international finance”, Economic Policy 31(87), July, 409-51.

Amiti, M, and D Weinstein (2018) ”How Much Do Idiosyncratic Bank Shocks Affect Investment? Evidence from Matched Bank-Firm Loan Data”, Journal of Political Economy 126(2).

Amiti, M, P McGuire, and D Weinstein (2019) “International Bank Flows and the Global Financial Cycle“, IMF Economic Review 67, 61-108.

Basel Committee on Banking Supervision (BCBS) (2008) “Liquidity risk: management and supervisory challenges”.

Basel Committee on Banking Supervision (BCBS) (2017) “Basel III: Finalising post-crisis reforms”, December 2017.

Bank for International Settlements (BIS) (2018) “Moving forward with macroprudential frameworks”, BIS Annual Economic Report 2018.

Boissay, F, C Cantú, S Claessens and A Villegas (2019) “Impact of financial regulations: insights from an online repository of studies”, BIS Quarterly Review, March 2019. https://stats.bis.org/frame/

Cerutti, E, R Correa, E Fiorentino, and E Segalla (2017) “Changes in Prudential Policy Instruments – A New Cross Country Database”, International Journal of Central Banking 13(1), 477-503.

European Systemic Risk Board (ESRB) (2018) “A Review of Macroprudential Policy in the EU in 2017”, April 2018.

ESRB (2019) “A Review of macroprudential policy in the EU in 2018”, European Systemic Risk Board.

Financial Services Authority (FSA) (2009) “Strengthening liquidity standards”, Policy Statement 09/16, October.

Financial Stability Board (FSB) (2019) “FSB Report on market fragmentation”, June 2019, www.fsb.org.

Hohl, S, M C Sison, T Stastny, and R Zamil (2018) “The Basel framework in 100 jurisdictions: implementation status and proportionality practices”, FSI Insights on policy implementation No 11, November 2018.

Institute of International Finance (2019) “Addressing market fragmentation: the need for enhanced global regulatory cooperation”, IIF Report, 24 January 2019.

Lane, P, and G M Milesi-Ferretti (2007) “The external wealth of nations mark II: Revised and extended estimates of foreign assets and liabilities, 1970-2004”, Journal of International Economics 73, 223-250.

McCauley, R, A Bénétrix, P McGuire and G von Peter (2019) “Financial deglobalisation in banking?” Journal of International Money and Finance 94.