This policy brief examines Italian banks’ bond issuance from the global financial crisis in 2007-08 onwards, considering the broader macroeconomic context and the unconventional monetary policies in the euro area. Following the sovereign debt crisis, there was a gradual decline in overall bank bond issuance, along with an increase in retail deposits and in the use of Eurosystem refinancing operations. Granular securities data reveal that Italian banks partly replaced bond issuance with alternative funding sources. This strategy reduced the impact of financial shocks on funding costs but increased the dependence on quantitative monetary policy tools. Monetary policy normalization may induce banks to boost bond financing as their existing funds reach maturity. This could considerably tighten private sector funding conditions. Monitoring overall bank funding costs is thus crucial to prevent financial tensions from materializing within the banking sector.

Bond issuance represents a significant source of funding for banks, along with customer deposits, primarily from households, wholesale funding through the interbank market, and other short-term debt instruments. In addition to these traditional funding sources, banks can access central bank liquidity and raise capital through equity (Van Rixtel and Gasperini, 2013).

This article examines the bond issuance activity of Italian banks from 2008 to mid-2023, summarizing the findings of Ceci, Montino, Pinoli, and Silvestrini (2023). During the period from the outbreak of the global financial crisis to the beginning of the ECB’s tightening cycle in December 2021, bond issuance as a percentage of the total funding of Italian banks decreased from 25% to 7%. This decline can be attributed in part to the progressive replacement of bonds with longer-term refinancing operations provided by the Eurosystem under favourable terms (Bank of Italy, Annual Report on 2021). Additionally, the decrease in gross bond issuance was offset by an increase in bank deposits, which have, on average, shown positive annual growth rates over the past 15 years.

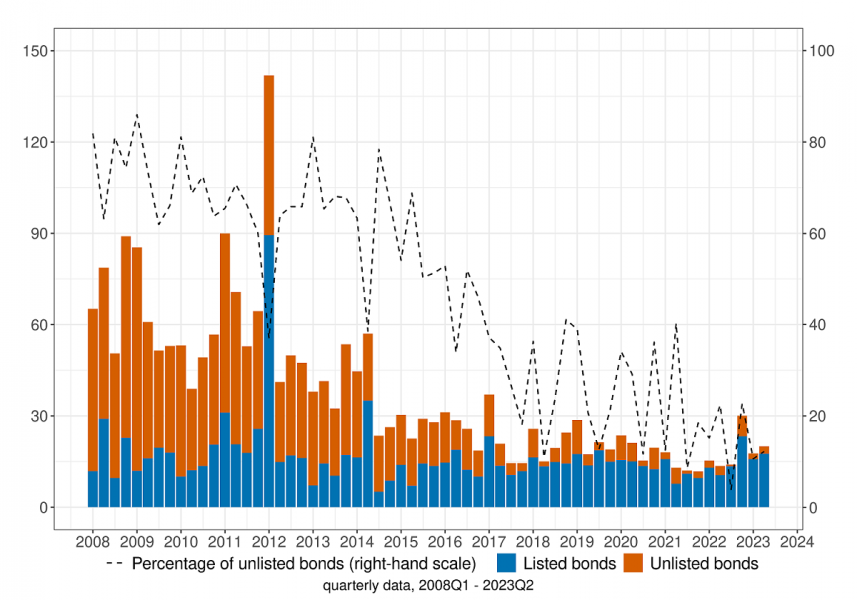

The type of securities issued and placed with investors changed considerably during the period under consideration. Until the sovereign debt crisis, banks primarily issued unlisted ordinary bonds, which were directly offered to retail investors. Since 2011, the issuance of unlisted bonds has steadily declined, while the issuance of listed bonds has remained relatively stable (Figure 1).

Figure 1: Gross bond issuance by banks with maturity at issuance longer than 1 year: disaggregation by listing (left-hand scale: billions of euro; right-hand scale: percentage of unlisted bonds on total bonds issued)

Source: Based on Bank of Italy data (security registry database).

Since the global financial crisis, Italian banks changed the composition of their debt securities by increasing the share of covered bonds (including those backed by public guarantees) and reducing the share of ordinary bonds.

The share of securitization in the total number of issued bonds, which averaged around 5% from 2008 to 2022, notably increased at the end of 2008, in 2015-16, and again at the end of both 2020 and 2022. These increases followed various legislative measures enacted by Italian and European authorities. Key measures promoting securitization included the following.

During the most acute phase of the sovereign debt crisis in 2011-12, more than half of bond issuances were repurchased and used for Eurosystem credit operations. This trend was driven by increased market uncertainty, which made it challenging to sell bonds on the wholesale market. At the same time, unconventional monetary policy measures provided banks with lower-cost funding opportunities, allowing the use of bonds as collateral in Eurosystem refinancing operations. Subsequently, the use of bank bonds as collateral decreased, although Italian banks continued to access refinancing operations with the Eurosystem by providing bank loans as collateral, thanks to the inclusion of Additional Credit Claims (ACC) established by the ECB in December 2011.

Looking specifically at securities placed among retail investors with a maturity longer than one year, gross bond issuance of bank bonds gradually declined during the period under review. Between 2011 and 2016, bond placements decreased by approximately 15% per year, eventually stabilizing at levels below €50 billion. This trend can be attributed to reduced issuance of unlisted bonds, which experienced a significant fall between 2011 and 2021. In contrast, with the beginning of the tightening cycle at the end of 2021, in 2022 there was a notable 43% increase in the issuance of listed bonds compared to the previous year.

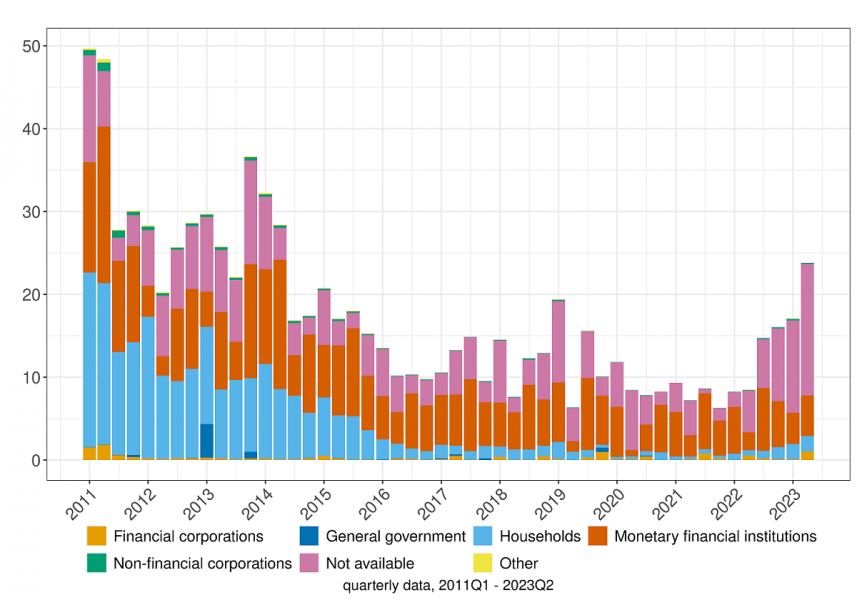

As shown in Figure 2, after the sovereign debt crisis the share of bank bonds in households’ portfolios declined markedly, and became negligible in recent years. Conversely, bank bonds held by wholesale investors, specifically monetary financial institutions, represented a significant portion of total bank bond issuance, and their share remained relatively stable. Bonds held by monetary financial institutions experienced a decline only in the years following the sovereign debt crisis, occurring from the summer of 2011 to mid-2012. This decline was a result of credit rating agencies downgrading Italian sovereign debt and the subsequent challenges faced by Italian banks in accessing international financial markets.

Figure 2: Marketed gross bond issuance by banks with maturity at issuance longer than 1 year: disaggregation by borrower type (billions of euro)

Source: Based on Bank of Italy data (supervisory statistical reports and security registry database).

Specifically, the share of unlisted bonds placed with households dropped from nearly €70 billion in 2011, which accounted for about half of unlisted placements, to €5 billion in 2016, which constituted only one-fifth of unlisted placements. Several factors contributed to this decline. On the supply side, the introduction of unconventional monetary policy measures enabled banks to borrow from the Eurosystem at a lower cost, thereby reducing the issuance of bank bonds. On the demand side, owing to the progressive reduction in global interest rates, the attention received from bondholders decreased due to the lower remuneration for new issues. Additionally, changes in tax policy in Italy had a negative effect on the demand for bonds among investors. The tax rate on bank bond coupons rose from 12.5% to 20% as of January 2012 and further to 26% in July 2014. The increase in tax rates induced a positive shock on bank deposits and a negative shock on bond financing (Carletti et al., 2021).

Another factor that likely influenced banks’ propensity to issue bonds was the introduction of the general principle of “bail-in” in 2014 through the Banking Recovery and Resolution Directive (BRRD, European Directive 2014/59). The implementation of the “bail-in” principle may have deterred retail savers from investing in bank bonds, as these latter were no longer perceived as risk-free, especially in light of the banking crises of the past decade. Additionally, banks adjusted their funding strategies, giving priority to the sale of insurance products, pension funds, and investment funds to enhance fee and commission income (Bank of Italy, Financial Stability Report, 1, 2014).

The observed substitution of bank bonds, especially unlisted bonds, with alternative sources of funding, such as bank deposits and longer-term refinancing operations, has, on one hand, attenuated the transmission of financial shocks to borrowing costs through financial markets. However, as a side effect, it has also increased the banking system’s reliance on unconventional monetary policy measures.

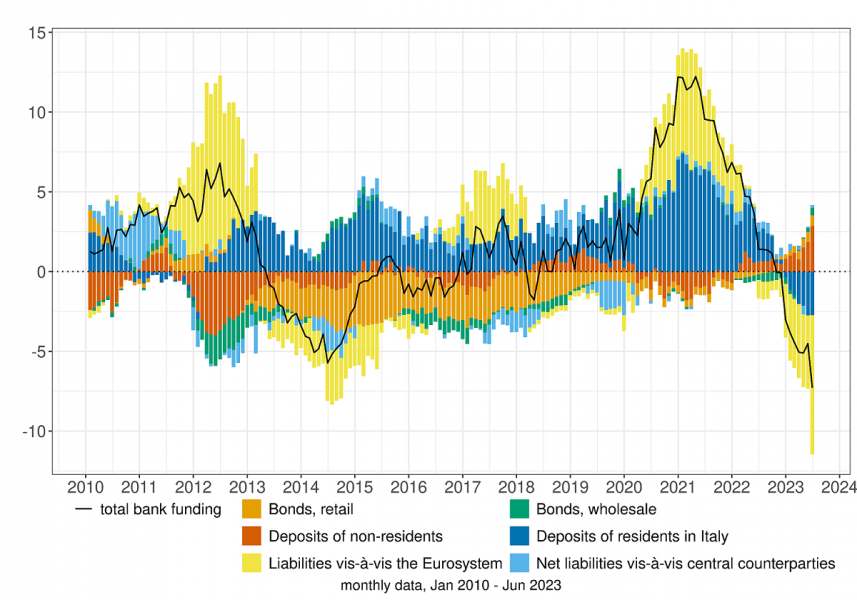

Since December 2021, the normalization of monetary policy prompted banks to change their funding strategies, decreasing their reliance on Eurosystem longer-term refinancing operations (TLTRO) and favouring alternative funding sources. Furthermore, the rise in nominal interest rates encouraged investors to explore additional investment opportunities for their available funds rather than solely depending on bank deposits. Consequently, since the end of 2022, there has been a decline in overall bank funding (Figure 3). This decline can be attributed to a substantial reduction in financing from the Eurosystem and resident deposits, despite an increase in bond issuances and foreign deposits.

Figure 3: Growth in bank funding: contributions from the various components (12-month percentage changes)

Source: Based on Bank of Italy data (supervisory statistical reports). Notes: The growth rate of total funding is equal to the sum of the contributions of the individual components. Percentage changes are adjusted to take account of the effects of securitizations, reclassifications, write-downs, exchange rate adjustments and other changes not due to transactions. Net liabilities to central counterparties represent funding in repurchase agreements with non-residents carried out through them.

With mounting inflationary pressures in the economy, in late October 2022 the ECB announced that the interest rate for all remaining TLTRO III operations would be indexed to the average of the prevailing ECB policy rates over the period, eliminating the preferential treatment applied until then. The recalibration of existing TLTRO III operations to align with the broader monetary policy normalization process prompted banks to frontload their repayments and initiate a process of repayment and replacement of this funding source with other forms of funding.

Another factor that may impact banks’ funding strategies is the introduction of MREL (Minimum Requirement for Own Funds and Eligible Liabilities) starting from January 1, 2024. MREL regulations will require financial intermediaries to structure their liabilities to ensure they always have sufficient eligible instruments to support the preferred strategy in case of resolution. According to European regulations, equities, subordinated bonds, unsecured senior bonds, and non-retail customer deposits with a maturity exceeding one year can be used to meet MREL requirements. While the Italian banking system maintains, on average, an adequate funding composition, some banks still need to issue eligible instruments to comply with MREL. Since these instruments must be absorbed by financial markets, a sudden increase in their issuance could have a significant impact on funding conditions (Bank of Italy, Financial Stability Report, 1, 2023).

Within this framework, banks could resort to bond issuance again, even if the tightening of the ECB monetary policy leads to higher costs. The combination of outstanding debt service obligations and TLTRO III operations maturing in 2023 could further encourage bond financing, potentially leading to an increase in the required coupon rate. In the present context of restrictive monetary policy and slowing economic activity, it is thus crucial to regularly monitor the increase in the cost of bank funding and its potential effect on the tightening of financial conditions for the private sector.

Bank of Italy, Annual report on 2008.

Bank of Italy, Annual report on 2021.

Bank of Italy, Financial Stability Report, n. 1, 2014.

Bank of Italy, Financial Stability Report, n. 2, 2014.

Bank of Italy, Financial Stability Report, n. 2, 2020.

Bank of Italy, Financial Stability Report, n. 1, 2021.

Bank of Italy, Financial Stability Report, n. 1, 2023.

Carletti, E., De Marco, F., Ioannidou, V., and E. Sette (2021). Banks as patient lenders: Evidence from a tax reform. Journal of Financial Economics, Volume 141, Issue 1, July 2021, pp. 6–26.

Ceci, D., Montino, A., Pinoli, S., and A. Silvestrini (2023). Gross bond issuance by Italian banks: key trends in times of crisis and unconventional monetary policy, Banca d’Italia Occasional paper 778.

Van Rixtel, A., and G. Gasperini (2013). Financial crises and bank funding: recent experience in the euro area, BIS Working Papers 406, Bank for International Settlements.