Both authors are grateful to the Bureau of Economic Research (BER) for the data and to the South African Reserve Bank (SARB) where both authors are external research fellows. Comments from George Kershoff and Hugo Pienaar on an earlier draft are greatly appreciated.

The anchoring of inflation expectations is today widely accepted to be an important facet of monetary policy. One important dimension along which the degree and nature of anchoring can be assessed is according to the level of disagreement between the expectations of a group. Within macroeconomics, there is an increasing focus on heterogeneity and information that we gather about disagreement is naturally an important contribution to this endeavour.

While there has been strong interest in the evidence from the studies about disagreement, the results across the literature remain inconclusive. There remains debate about the relationship between forecast disagreement and uncertainty (Glas and Hartmann (2015) and Boero et. al. (2015)), and far more work is needed to provide insight about the sources of disagreement. There are studies that consider things like the role of macroeconomic news (for example Bauer, 2015) on disagreement amongst US Blue Chip and SPF forecasts, but there is little evidence about what drives the behaviour of other important economic decision makers within an economy.

Furthermore, much of the literature has relied on survey data from financial professionals or households because that is the data that are more readily available. However, there is increasing interest in the expectations of firms, which are viewed as a more accurate representation of price setters. In this paper, we use disaggregated South African firm level data gathered by the Bureau for Economic Research. These data are complemented with similar survey data about the expectations of trade unions (labor organizations) as well as financial analysts (professional forecasters).

The main contributions of this paper are threefold. We introduce a valuable survey dataset of disaggregated firm level data from South Africa. After considering the choice of measures of disagreement and forecast revision, we investigate the determinants of these econometrically. Importantly, we are able to analyze the impact of expectations at different levels of aggregation (e.g., industry level) as well across different occupations of respondents (e.g., economists versus CEOs). Finally, we consider how these results respond to shocks such as labor unrest, problems with electrical generation capacity, a severe drought, the Global Financial Crisis and we are able to offer preliminary results of the COVID 19 pandemic.

The BER survey dataset, which we analyse in this paper, offers rich time series. They are quarterly data, gathered since 2000, and the surveys includes questions about a range of other relevant macroeconomic and financial variables, together with the forecast of inflation. They also forecast for a range of horizons – the current year, following year and 5 years into the future, so we can comment on differences in anchoring of both shorter and longer term expectations.

There is no universally agreed upon measure of inflation forecast disagreement. We generated results using the inter-quartile range (IQR) of forecasts (in line with Mankiw, Reis, and Wolfers (2003), Capistrán and Timmermann (2008)) as well as a measure of forecast dispersion. The dispersion measure has the advantage that it incorporates all the information, but faces the vulnerability that it could therefore be sensitive to extreme outliers. We find that there are only a small number of extreme forecasts and that the changes in forecast disagreement generated using the firm-level data seems insensitive to the choice of disagreement measure employed. We therefore choose to report the results of the dispersion measure to retain all the information. We also explore the behavior of forecast revisions. The extent and regularity to which agents revise their expectations may give some idea of the extent to which they are inattentive to the latest information, for example.

Preliminary data analysis reveals considerable variation and differences in disagreement about inflation over time and across the three groups surveyed. Respondents in the business sector who forecasted relatively low inflation rates appear very sensitive to certain events relative to the same respondents who predicted higher inflation. For example, we observe great volatility in the expectations of respondents with low expectations during periods when South Africa experienced labour strikes, problems with electrical generation capacity, and a severe drought. The impact of these events is less noticeable from the group of businesses that expected relatively higher inflation. A similar asymmetry between the two groups is evident in the face of the COVID-19 pandemic. In contrast, the difference between the high and low forecasts of the financial experts is far smaller and does not display the relationship described below.

The average size of revisions is mostly negative, and the standard deviations of revisions falls when the forecast horizon increases in 9 of the 17 categories. This suggests greater consensus about expected inflation at longer horizons.

Using the measure of disagreement, we econometrically explore the determinants of the forecast disagreement measures. We investigate whether forecast disagreement about inflation is linked to disagreement in other macroeconomic or financial variables that might be linked to these according to economic theory. We also analyse the response of disagreement inflation to the level of expectations of these same variables. This permits us to ask whether current disagreement in inflation expectations is driven by beliefs about how well or how poorly economic activity is expected to perform as measured by the other forecasts generated by the survey. This is followed by an estimation of a factor model, which allowed us to use the large number of series jointly. It offers a more parsimonious way of combining the relationship between sources of disagreement across the different macroeconomic and financial variables.

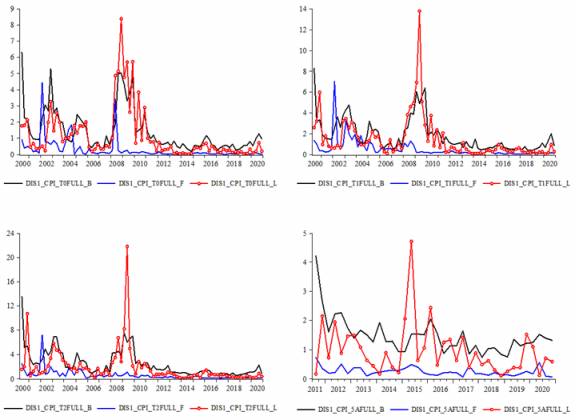

Econometric estimates reveal a number of insights. The GFC (2009-2010) has the largest impact on forecast disagreement at all horizons1, and when forecasters disagree about future inflation it is because they also disagree about the future course of other key macro-financial variables. This is clearly seen in Figure 1. Labour unions (L) tend to display the higher levels of disagreement than firms and financial analysts (F). In fact, disagreement among financial analysts also tends to decrease further over longer horizons. Across all 3 groups (B,F,L), but most notably for financial analysts, forecast disagreement generally decreased after the adoption of inflation targeting. While disagreement did increase in response to large shocks over the period, it has been notably stable after the GFC, and particularly from approximately 2012.

We then consider forecast disagreement for more disaggregated data – considering differences across different firm sizes, different industries and based on the views of the CEOs of the business’ surveyed. Disagreement in the mining and manufacturing sectors are more sensitive to macroeconomic developments than, for example, the retail sector. There are also persistent differences in forecast disagreement that are sensitive to firms’ size and the occupation of the respondents (e.g., economists versus CEOs).

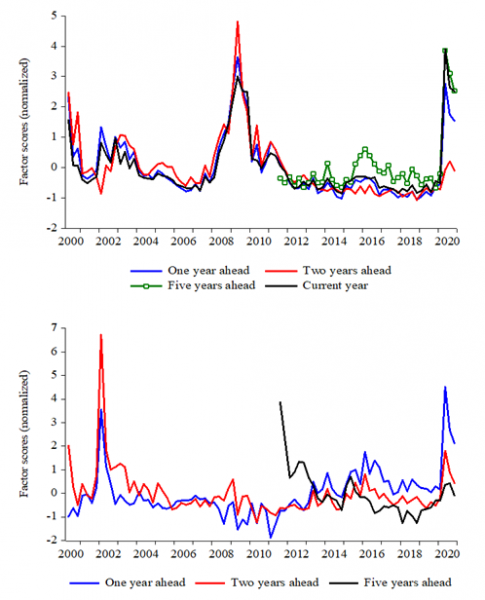

Neither aggregate nor disaggregated forecast disagreement rises greatly at the beginning of the COVID-19 pandemic, until we analyse macroeconomic forecast disagreement using an indicator we created that combines forecasts for all available variables. This is seen in Figure 2 below. The indicator also reveals that in response to the GFC, disagreement in some sectors or industries did not rise as sharply as in the data aggregated across sectors surveyed and for the entire data set combined.

Figure 1. Forecast disagreement by major groups surveyed

Note: DIS1 refers to our indicator of forecast disagreement. See the full paper for details. CPI refers to the Consumer Price Index. T0FULL, T1FULL, T2FULL and 5AFULL refer to the forecast horizons (current year (0), 1, 2, and 5 years ahead (1,2,5). FULL means that data from all respondents was used. B, F, and L refer to the business sector, financial analysts, and labour representative, respectively.

Figure 2. Disagreement based on factor model generated inflation expectations

Note: The top figure uses all forecast data (inflation, wages, GDP, prime, rand) from the B, F, and L sectors. The bottom figure uses forecast data generated at the firm size level (i.e., micro, small, medium, large). Factor models for current year (T0) include disagreement for inflation, real GDP growth, the Prime interest rate, the Rand/USD exchange rate and wage growth. The one year ahead (T1) factor model includes current and one year ahead disagreement; the two year (T2) ahead factor model includes two year ahead disagreement for inflation and one and current year disagreement for the remaining variables. The five year ahead (5a) factor model includes one year ahead disagreement and two year ahead inflation disagreement. Disagreement for the business, labor and financial analysts are included. The T0 factor model includes 15 variables; 30 variables in the T1 factor model; 18 variables in the T2 and 5a factor models. Estimation via principal components with number of factors set at 1 for the current year model and 2 for the remaining factor models. In the case of 2 factors the scores are estimated following a rotation via the Varimax method.

In summary, we find the following. Our findings reveal that when forecasters disagree about future inflation it is because they also disagree about the future course of other key macro-financial variables. Moreover, inflation forecast disagreement is also partially driven by past observations of the series being forecast. We are also able to conclude not only that forecasters disagree about future inflation, because they also have different expectations about other key variables, but that the source of disagreement is sensitive to the level of aggregation in the data. Indeed, when we construct a measure of macroeconomic disagreement that combines all the variables being forecast in a statistical manner we observe that forecasters responded sharply in early 2020 as the pandemic emerged. That said, our findings on the determinants of inflation forecast disagreement are unable to tell us whether this is due to a form of inattention, to differences in what the past portends for the future, certain socio-economic characteristics of the forecasters we are unable to quantify, or some type of bias in how disagreement about future inflation emerges. Nevertheless, the results do point to the value added in individual level forecasts and how these can possibly provide insights into how a central bank might consider communicating differently with different audiences.

Bauer, M. (2015), “Inflation Expectations and the News”, International Journal of Central Banking (March): 1-40.

Boero, G., J. Smith, and K. Wallis (2015), “The Measurement and Characteristics of Professional Forecasters’ Uncertainty”, Journal of Applied Econometrics 30 (November/December): 1029-1046.

Capistrán, C. and A. Timmermann (2008), “Disagreement and Biases in Inflation Expectations”, Journal of Money, Credit and Banking 41 (March-April): 365-396.

Glas, A. and M. Hartmann (2015), “Inflation Uncertainty, Disagreement and Monetary Policy: Evidence from the ECB Survey of Professional Forecasters”, Heidelberg University, February.

Mankiw, N.G., R. Reis, and J. Wolfers (2003), “Disagreement About Inflation Expectations”, NBER working paper 9796, June.

Unfortunately, the data for the 5 year horizon was not yet collected over this period.