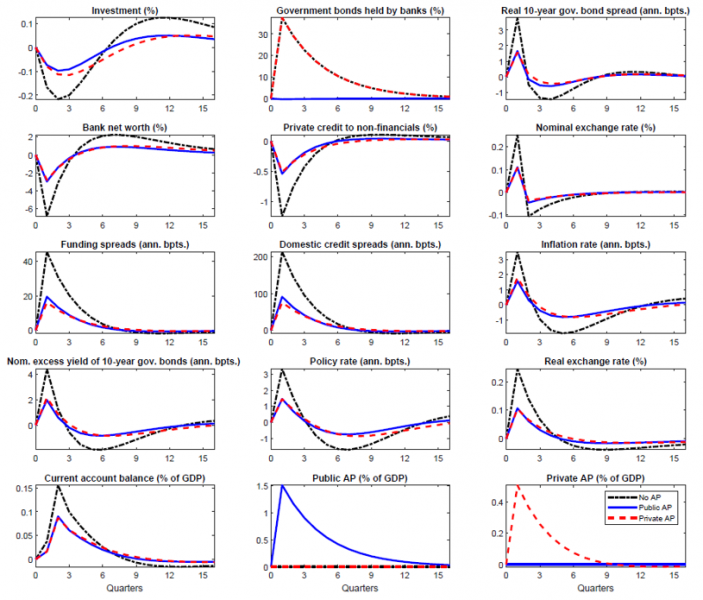

We show that the exposure of EME sovereigns to foreign investors can tighten overall financial conditions when foreign lenders sell off government bonds of these countries during a stress episode (dotted dashed lines in Figure 1). If the central bank does not undertake asset purchases, domestic commercial banks absorb the bonds sold off by foreigners, which pushes down their price and raises the excess yield on sovereign bonds over US interest rates. This crowds out bank credit to non-financial firms, bids down private firm bond prices and leads to a widening of intermediation margins. Hence, the external bond sell-off shock has adverse spillover effects on domestic financial conditions. The foreign borrowing capacity of domestic banks is hindered by their weaker balance sheets due to depressed asset prices, exacerbating the initial net capital outflows from the sovereign bond sell-off. The ensuing depreciation of the currency raises import prices and passes through to aggregate prices, inducing conventional monetary policy to tighten to stabilise inflation.

Figure 1: Asset purchases counteract bond sell-off shocks

We find that central bank bond purchases could address the market dislocation so that commercial banks are no longer required to absorb the bond sell-off by foreign investors (solid lines in Figure 1). This would limit the crowding out of credit to firms and the collapse in sovereign bond and non-financial corporate bond prices. Stronger asset prices would in turn reduce the tightening of financial conditions as measured by excess bond yields and loan-deposit spreads. Stronger private domestic bank balance sheets would provide better foreign-borrowing prospects for banks, limit capital outflows, reduce currency depreciation and create room for manoeuvre for monetary policy. Private asset purchases bring about a similar degree of stabilisation in response to the bond sell-off shock (dashed lines in Figure 1). In this case, the total credit base expands with central bank pur-chases of firm securities and commercial banks’ utilisation of the safe asset role of government bonds is preserved.

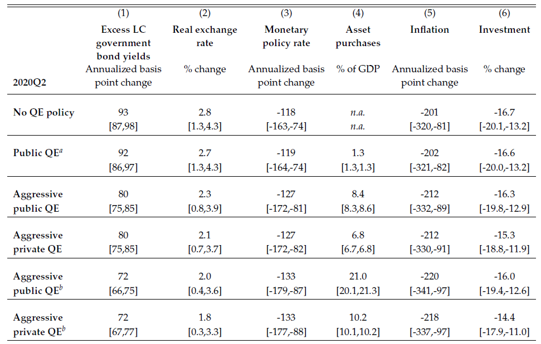

Although potentially useful in extreme stress episodes, central bank bond purchases in EMEs are not always effective. Firstly, high-frequency estimates suggest that asset purchases during the pandemic resulted in only short-lived reductions in bond yields (Arslan et al., 2020; Fratto et al., 2021; Hartley and Rebucci, 2020; IMF, 2020; and WB, 2021). Indeed, by using an estimated version of our model, we show that the level of bond purchases in EMEs observed during the pandemic was not large enough to bring a sizeable and persistent easing of financial conditions (second row of Table 1 named as “Public QE”). On the other hand, when public bond purchases by the central bank are counterfactually increased to the levels observed in large, advanced economies during the pandemic, the central bank could have reduced excess government bond yields in a statistically significant manner (third row of Table 1 named as “Aggressive Public QE”). In addition, the 6-day average bond yield compression of more than 20 basis points in EMEs as estimated by the IMF (2020) could have survived a full quarter only if public (private) asset purchases had been as large as 21% (11%) of GDP, which is arguably untenable for EMEs (the last two rows of Table 1). This leads to the policy implication that asset purchases by credible emerging-market central banks can be useful to guide price discovery in times of stress but the degree of its effectiveness depends on the size of the purchases. Moreover, deploying asset purchases to systematically manage aggregate demand is likely to hinder central bank credibility in EMEs as it requires sizable asset purchases. Secondly, if bond purchases lead to a de-anchoring in inflation expectations, we find that they bring a smaller reduction in real excess bond yields while leading to higher and more persistent inflation. Finally, a larger central bank balance sheet, especially if not scaled down once domestic financial conditions normalise, could elevate fiscal dominance risks, and raise concerns that investors perceive future monetary policy tightening as less likely because of the potential for central bank losses on bond holdings.

Table 1: The implications of baseline and alternative EME central bank asset purchases in response to the COVID-19 shock

Note: One quarter-ahead effects of adopting baseline and counterfactual asset purchase policies during the COVID-19 crisis. Changes relative to the HP-filtered trend at quarterly frequency. Increases in the real exchange rate denote depreciations. Asset purchases are as a share of steady state GDP. Ranges in square brackets are 90% confidence intervals. a) This row constitutes the baseline case and coincides with the cross-country averages of the actual data in 2020Q2. The remaining rows represent the outcome of counterfactual exercises. b) Asset purchase sizes in these rows are calibrated to match the 6-day average bond yield compression of 22 basis points in EMEs as estimated by the IMF (2020) report.

Arslan, Yavuz, Mathias Drehmann, and Boris Hofmann, “Central bank bond purchases in emerging market economies,” 2020. BIS Bulletin No. 20.

Calvo, Guillermo A. and Carmen M. Reinhart, “Fear of Floating,” Quarterly Journal of Economics, 2002, 117(2), 379–408.

Cordella, Tito, Pablo M. Federico, Carlos A. Vegh, and Guillermo Vuletin, Reserve Requirements in the Brave New Macroprudential World number 17584. In ‘World Bank Publications – Books.’, The World Bank Group, 2014.

Fratto, Chiara, Brendan Harnoys Vannier, Borislava Mircheva, David de Padua, and He le ne Poirson, “Unconventional Monetary Policies in Emerging Markets and Frontier Countries,” 2021. IMF Working Paper, 21/14.

Hartley, Jonathan S. and Alessandro Rebucci, “An Event Study of COVID-19 Central Bank Quantitative Easing in Advanced and Emerging Economies,” 2020. CEPR Discussion Paper Series, DP14841, June.

IMF, “Bridge to Recovery,” Global Financial Stability Report, 2020. October.

Kaminsky, Graciela L., Carmen M. Reinhart, and Carlos A. Ve gh, “When It Rains, It Pours: Procyclical Capital Flows and Macroeconomic Policies,” in “NBER Macroeconomics Annual 2004, Volume 19” NBER Chapters, National Bureau of Economic Research, Inc, November 2005, pp. 11–82.

Mimir, Yasin and Enes Sunel (2023): “Fear (no more) of Floating: Asset Purchases and Exchange Rate Dynamics”, ESM Working Papers, No 57.

WB, “Global Economic Prospects,” 2021. January, World Bank.