The views expressed in this paper are those of the authors and do not necessarily reflect those of the Eurosystem or the Oesterreichische Nationalbank (OeNB).

The secular rise in globalization has led to a substantial increase in the interconnectedness of global financial markets. This has important implications for the conduct of monetary policy, as central bank policies may diverge across countries, potentially affecting key transmission channels of domestic policy actions. In this study, we propose a novel nonlinear multivariate time series model with weekly data to examine the influence of U.S. monetary policy on the transmission of monetary policy in the euro area. Scenario-specific impulse responses show that the transmission of euro area monetary policy through financial markets does indeed depend on the prevailing monetary policy regime of the Federal Reserve and has significant effects on a variety of euro area financial market variables. Our approach enables us to examine how the term structure of real interest rates responds to ECB monetary policy shocks, contingent upon the prevailing U.S. monetary policy regime. Our analysis reveals that hawkish ECB surprises elicit a stronger increase of short-term real government bond yields when the Fed’s stance aligns with hawkishness, compared to situations where monetary policies diverge.

In response to rising inflation, most major central banks have begun to tighten their monetary policy stance. However, as macroeconomic fundamentals, financial dynamics or cyclical positions may differ across countries, these policy adjustments may diverge internationally. In 2022, some central banks, such as the Bank of England or the Federal Reserve (Fed), have started their tightening cycle relatively early, while others, notably the European Central Bank (ECB), raised policy rates later. This can lead to divergence in monetary policy, which opens up potential interaction effects between central banks.

However, most models assume that a central bank’s reaction function is driven purely by domestic factors, a rather strong assumption given the increased financial and real linkages in the world economy. Even if domestic quantities are somewhat affected by foreign activity through, e.g., the trade balance, foreign monetary policy is often a neglected dimension in these analyses. In Huber et al. (2023), we suggest explicitly considering the influence of the Fed’s policy stance on the ECB’s monetary policy, given the Fed’s prominent role in the global financial cycle (Miranda-Agrippino and Rey 2020).

Our analysis focuses on the financial aspect of the economy, incorporating weekly data on various indicators of the euro area (EA). This includes government bond yields, inflation-linked swaps to gauge market-based inflation expectations, the euro’s exchange rate against the U.S. dollar, and the EuroStoxx50 index.1 Given the diverse maturities of government bonds and inflation-linked swaps, we employ a term structure model to extract key features such as the level, slope, and curvature of the yield curve. This comprehensive approach not only examines the term structure of interest rates (i.e., the yield curve) and inflation expectations but also enables us to compute real interest rates. Our model consists of two linear vector autoregressions (VAR), each associated with the Fed’s stance being either expansionary or restrictive. These states are linked by a nonlinear function that governs the transition between the two regimes. This function is bounded between zero and one and incorporates the Fed’s monetary policy stance as an input variable.2

We gauge the Fed’s monetary policy stance by assessing the deviation of the effective federal funds rate from an estimate of the U.S. equilibrium real interest rate (Laubach and Williams, 2003). This estimate represents the rate at which the economy operates at its potential output while maintaining stable inflation. Consequently, deviations from this rate capture the actual stance of monetary policy. For subsequent analysis, we identify ECB monetary policy shocks by examining high-frequency financial market reactions within a narrow window around scheduled events associated with monetary policy announcements (Altavilla et al., 2019). These shocks are then aggregated on a weekly basis. This approach enables us to flexibly track how the impact of ECB policy surprises changes depending on the Fed’s stance.

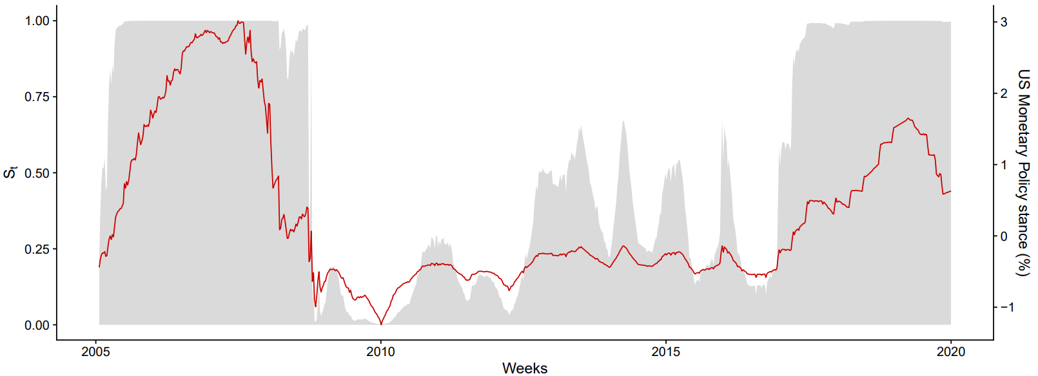

In Figure 1, we present our estimate of the nonlinear transition function (depicted by the gray areas), derived from the input variable – the Fed’s policy stance (shown in red). Values of the function close to zero show periods predominantly marked by an expansionary Fed, while those close to unity indicate periods characterized by a restrictive stance. Our findings indicate that the Fed maintained a relatively restrictive stance leading up to the financial crisis and following 2016. However, the period in between was characterized by expansionary periods punctuated by several restrictive but transitory policy regimes.

Figure 1: Assessment of the transition function (gray areas) based on the deviation of the effective federal funds rate from the U.S. equilibrium real interest rate (red line)

Notes: The gray areas show the transition function, where 0 (1) indicates an expansionary (contractionary) monetary policy stance of the Fed regime. The red line shows the US monetary policy stance indicator, which is the percentage deviation of the effective federal funds rate from the US equilibrium real interest rate (r*).

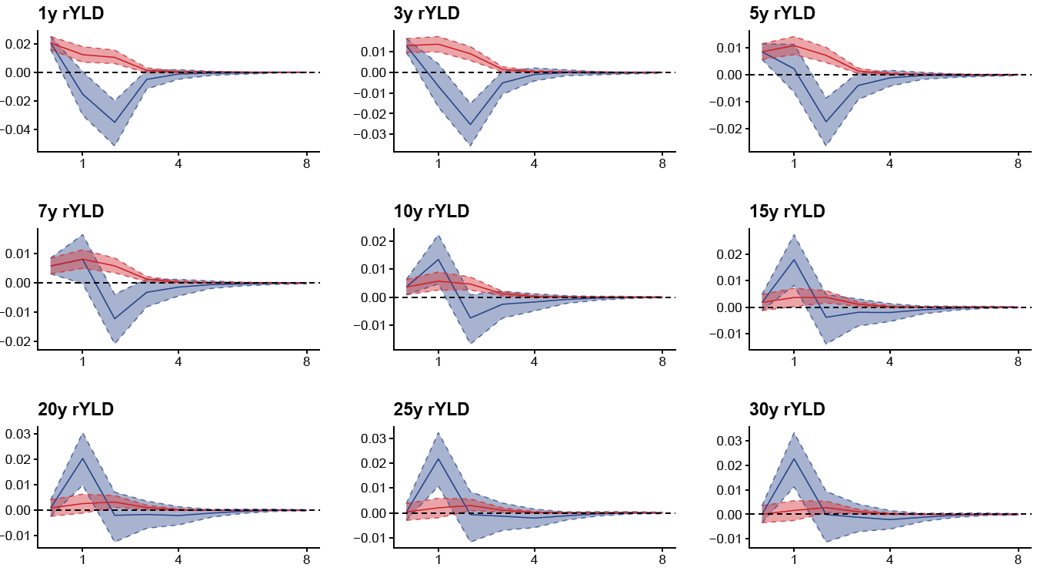

We conduct a simulation of a restrictive monetary policy shock in the euro area, explicitly considering the prevailing U.S. monetary policy stance as a conditioning factor. Through an impulse response analysis, we aim to understand how the effects of ECB monetary policy might vary in response to a divergent Fed policy. Figure 2 illustrates selected first differences of real government bond yields in response to ECB monetary policy shocks, conditional on the prevailing U.S. monetary policy regime. Specifically, we examine the impact of a restrictive EA shock under two scenarios: when U.S. monetary policy is very tight (depicted in red, representing the 95th percentile of the threshold) and when it is very expansionary (depicted in blue, representing the 5th percentile of the threshold). Our findings reveal that when monetary policy is evaluated based on its impact on real interest rates, a policy surprise under a restrictive U.S. stance initially results in positive real interest rate reactions during the first four weeks post-shock. However, under an expansionary Fed stance, the immediate increase in real interest rates transitions into a sharp negative reaction after approximately two weeks, particularly evident for short-term maturities. The observed differences in the impulse response function, though not depicted here, are statistically significant, except for some medium-term maturities.

Figure 2: Impulse response functions of a restrictive monetary policy shock in the euro area for selected real government bond yields in the euro area.

Notes: The figure shows the responses to a contractionary ECB monetary policy shock on selected real government bond yield changes (maturities ranging from 1 to 30 years) in the euro area, conditional on two scenarios: A restrictive US monetary policy stance (95% percentile of the stance indicator, colored in red) and an expansionary US monetary policy stance (5% percentile of the stance indicator, colored in blue). The horizontal axis indicates the weeks following the shock.

Our analysis highlights the significant influence of the Fed’s stance on the dynamic responses of euro area financial markets to contractionary monetary surprises, revealing strong evidence of nonlinear interaction effects. The relationship between impulse responses and U.S. monetary policy exhibits heterogeneity in both form and magnitude across the term structure. Specifically, we find that nominal bond yields in the EA experience more pronounced effects from contractionary EA monetary policy when the Fed pursues an expansionary stance. However, these effects reverse after approximately two weeks, as bond yields may tend to decline due to capital inflows into the EA economy, leading to higher bond prices.

Conversely, when the EA shock coincides with a restrictive Fed stance, we observe milder reactions across different maturities of bond yields, indicating heterogeneity in response. Analysis of the term structure of inflation-linked swaps shows muted differences when controlling for the U.S. stance. Generally, our results indicate negative reactions at the time of the shock, with varying dynamics thereafter based on the prevailing U.S. monetary policy stance. Although there is some evidence of nonlinearities, their significance is marginal.

After analyzing the reaction of other variables in our model to contractionary monetary policy shocks in the euro area, several key observations emerged. Firstly, we noted that following such shocks, the euro tends to appreciate against the U.S. dollar regardless of the Fed’s policy stance. However, the extent of this appreciation varied depending on whether the U.S. stance was expansionary or restrictive. Specifically, during periods of an expansionary U.S. stance, characterized by widened yield differentials, the euro’s appreciation was somewhat more pronounced. Secondly, we found that stock markets react negatively to the shock, irrespective of the Fed’s stance. This negative reaction persisted even during periods of a restrictive Fed stance. However, in instances of an expansionary Fed stance, we observed a notable rebound in stock markets approximately a week after the shock, followed by mean reversion. One potential explanation for these observations is the aggregate nature of the Euro Stoxx 50 index, which may obscure underlying cross-sectional heterogeneity.

Our approach offers a significant advantage by enabling us to examine how the term structure of real interest rates responds to ECB monetary policy shocks, contingent upon the prevailing U.S. monetary policy regime. Through our nonlinear model, where the Fed’s monetary policy stance serves as a transition variable in the smooth transition VAR, we uncover notable interaction effects between U.S. and EA monetary policy in weekly financial market reactions. Our analysis reveals that hawkish ECB surprises elicit stronger reactions when the Fed’s stance aligns with hawkishness, compared to situations where monetary policies diverge.

Altavilla, C., Brugnolini, L., Gürkaynak, R. S., Motto, R., and Ragusa, G. (2019). Measuring euro area monetary policy, Journal of Monetary Economics 108, 162-179.

Hauzenberger, N., Huber, F., and Zörner, T. O. (2023). Hawks vs. Doves: ECB’s Monetary Policy in Light of the Fed’s Policy Stance, OeNB Working Paper Series, No. 252. https://www.oenb.at/Publikationen/Volkswirtschaft/Working-Papers.html.

Laubach, T., and Williams, J.C. (2003). Measuring the Natural Rate of Interest, Review of Economics and Statistics 85(4), 1063-1070.

Miranda-Agrippino, S. and Rey, H. (2020). US monetary policy and the global financial cycle, The Review of Economic Studies 87(6), 2754-2776.

We utilize euro area AAA-rated government bond yields, measured by yield curve instantaneous forward rates, sourced from data compiled by the ECB. In addition, we incorporate inflation-linked swaps, which are derivative products tied to the harmonized consumer price index (HVPI) excluding tobacco for the euro area. These swaps function as forward contracts between two parties, where the buyer pays a fixed nominal rate and receives a real rate from the seller. As such, swaps serve as instruments for hedging inflation and offer valuable insights into market-based expectations for future inflation.

In technical terms, we introduce a smooth transition vector autoregression (ST-VAR) model, wherein the Fed’s policy stance serves as a signal variable determining the corresponding regime. The transition function is assumed to be smooth and defined by a first-order logistic function.