This Policy brief is based on Oesterreichische Nationalbank Working Paper No 256. Opinions expressed are those of the author and do not necessarily reflect the official viewpoint of the OeNB or of the Eurosystem.

The current account balance is a key concept in international macroeconomics and finance. Its frequent conflation with the trade balance is problematic in the context of financial globalization: international current account imbalances are increasingly driven by international income payments. The economic mechanisms driving these payment flows differ from other current account determinants. Often, they are negatively correlated with the trade balance. This gives rise to opposing patterns that are hidden within the overall current account. These opposing patterns call for a re-assessment of the gains from globalization and new tools to monitor international imbalances and vulnerabilities.

Policymakers often debate international imbalances. We are used to sentences like “Our deficit with China hurts US jobs”, or: “Germany is exporting too much”.

Most of those policy debates focus on trade. Yet, what matters for international imbalances is the current account balance, which records all foreign transactions of an economy. It includes the trade balance but is a more comprehensive concept. Given that the trade balance used to be a dominant part of the current account, both are frequently equated or confused, even in several economic textbooks and models.

But due to financial globalization, the trade and current account balance have increasingly diverged from another. This is particularly due to international investment income flows, which result from assets held abroad. They are also part of the current account balance and include, for example, profits of multinationals from foreign affiliates or dividends on a foreign bond. In a new research paper I show that such international investment income payments (IIPs) account for a considerable part of the current account in many economies.

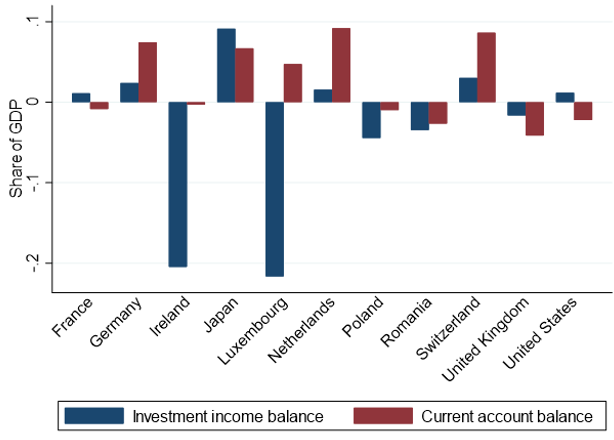

For example, movements in Japan’s current account were almost fully due to movements in the balance of international investment income payments in recent years. And even for Germany, net IIPs contributed about one third to the overall current account surplus (see Figure). Conversely, many economies of Central and Eastern Europe record net outflows of IIPs, which often turns their current account into deficit, despite a positive trade balance. And in small offshore financial centers, investment income payment to the rest of the world quickly amount to 20% of GDP on a net basis. In this case, IIPs are often profits from intangible assets that are parked in low-tax jurisdictions. The investment income balance of the current account is hence an informative account summarizing the real and financial interactions in the world economy.

Figure 1: Investment income and overall current account balances in selected countries

Source: own calculations based on data from Eurostat, FRED, Japanese MOF and Cabinet Office. Data are averaged for quarters since 2012.

Source: own calculations based on data from Eurostat, FRED, Japanese MOF and Cabinet Office. Data are averaged for quarters since 2012.

The economic factors driving these investment income payments can differ from other current account determinants. E.g., population aging and the savings rate, two traditional current account determinants, are negatively associated with the investment income balance, but positively associated with the remaining current account balance (notably, the trade balance). Moreover, investment income balances are more persistent and often negatively correlated with the rest of the current account. These stylized facts prevail in a sample of 34 countries that I investigate over about two decades in the referenced research paper.

This importance of the investment income balance for the current account balance creates at least three new policy-relevant perspectives towards the international division of labor and international imbalances: