Environmental degradation (such as climate change and biodiversity loss) and the increasing difficulty of many low- and middle-income countries to repay their public debt are now widely recognised as two sources of risk to the stability of the international financial system. Many recent proposals aim at addressing both problems jointly through so-called “debt-for-nature swaps”, whereby a country’s debt is reduced in return for a commitment to spend a share of the reduction on environmental protection. Debt-for-nature swaps can indeed improve environmental sustainability and lower public debt and thus contribute to the stability of the international financial system. However, their implementation poses many technical, financial and governance-related challenges. They could thus be accompanied by adverse effects that need to be analysed in detail.

Debt-for-nature swaps are financial transactions that aim at reducing a country’s debt in return for a commitment to spend a portion of that reduction on nature conservation. For developing countries, debt-for-nature swaps can help address the growing two-pronged challenge of lowering excessive public debt and dealing with climate change, to which they are particularly vulnerable.

The fight against the pandemic has increased the risk of public debt sustainability for low and middle-income countries, due to the fiscal efforts required. According to the International Monetary Fund (IMF, 2022b), their level of public debt in 2021 was higher than before the crisis: 49.6% of GDP for low-income countries and 66.1% for middle-income countries, compared with 43.5% and 54.6% in 2019 respectively. This increase is accompanied by a rise in the relative share of debt held by private creditors, to 63% of the total in 2020, compared with 14% for bilateral official creditors.

Faced with this situation, international mechanisms have been set up to prevent the risk of overindebtedness and to help the most vulnerable countries regain some fiscal room for manoeuvre. Between May 2020 and December 2021, the international community (G20) decided on a Debt Service Suspension Initiative (DSSI). This initiative benefited 47 countries for a total amount of USD 12.9 billion.

However, there are some difficulties in implementing these mechanisms. In particular, the ramp-up of the G20’s “Common Framework for Debt Treatments”, which replaced the DSSI, has been slow (IMF, 2021b). To date, only a few countries have requested debt restructuring under this framework. Moreover, their procedures are subject to considerable delays. Finally, middle-income countries do not benefit from these tools.

According to the scientific community, several “planetary boundaries” have been crossed (Persson et al., 2022), as in the case of biodiversity (IPBES, 2019), or could be crossed, as in the case of climate change (IPCC, 2021). These limits correspond to the thresholds beyond which different biophysical systems essential to life on Earth (e.g. the carbon cycle, which helps regulate the climate) are likely to react in a non-linear and irreversible manner as a result of certain human activities (e.g. the burning of fossil fuels, which leads to an over-concentration of CO2 in the atmosphere). Overstepping these thresholds is likely to have systemic consequences for human societies (Ripple et al., 2017) and in particular for economic and financial systems (NGFS, 2019; NGFS & INSPIRE, 2022).

Low- and middle-income countries are directly affected by the crossing of these planetary boundaries in two ways.

On the one hand, they are more rapidly and more severely exposed to the consequences of this boundary crossing due to their low resilience and high socio-economic vulnerability (De Bandt et al., 2021). Indeed, certain symptoms and their economic and financial consequences are already materialising. For example, climate risk has already contributed to a substantial increase in the cost of their public debt (see Chart 1). The climate and environmental crises therefore probably weaken the sustainability of this debt.

Chart 1: Channels of transmission of climate risk to sovereign risk

Source: (Adapted from) Volz et al., 2020.

On the other hand, low- and middle-income countries play a key role in stabilising ecosystems and the climate, and thus global economic systems. Indeed, most of the biodiversity hotspots, whose destruction produces negative externalities for the Earth’s climate and other ecosystems (Lovejoy and Nobre, 2018), are located in these countries. For example, two regions are particularly affected by deforestation: Latin America and the Caribbean, and sub-Saharan Africa, which are home to two biodiversity hotspots, the Amazon rainforest and the Congo Basin forest. In addition, a significant share of the investments needed for transitioning to a low-carbon economy (a prerequisite for economic and financial stability) or for adjusting to climate change should be devoted to them. According to the International Energy Agency (IEA, 2021), investments in decarbonised energy solutions by emerging and developing countries should reach more than USD 1,000 billion per year by the end of the decade, compared to USD 120 billion in 2020.

Faced with the two-pronged challenge of fighting environmental degradation and maintaining public debt sustainability in low- and middle-income countries (see above), proposals have recently brought “debt-for-nature swaps” back to the fore. For central banks, climate and environmental transitions are major financial stability issues (NGFS & INSPIRE, 2022). These issues are being increasingly discussed in the multilateral forums.

Debt-for-nature swaps are financial transactions that aim at reducing a country’s debt in return for a commitment to spend a portion of that reduction on nature conservation. Nature conservation actions seek to preserve or generate ecological gains (rehabilitation, enhancement or creation of protected areas, or mitigation of climate change), or even to compensate quantitatively and qualitatively for ecological losses due to human activities (Levrel, 2020).

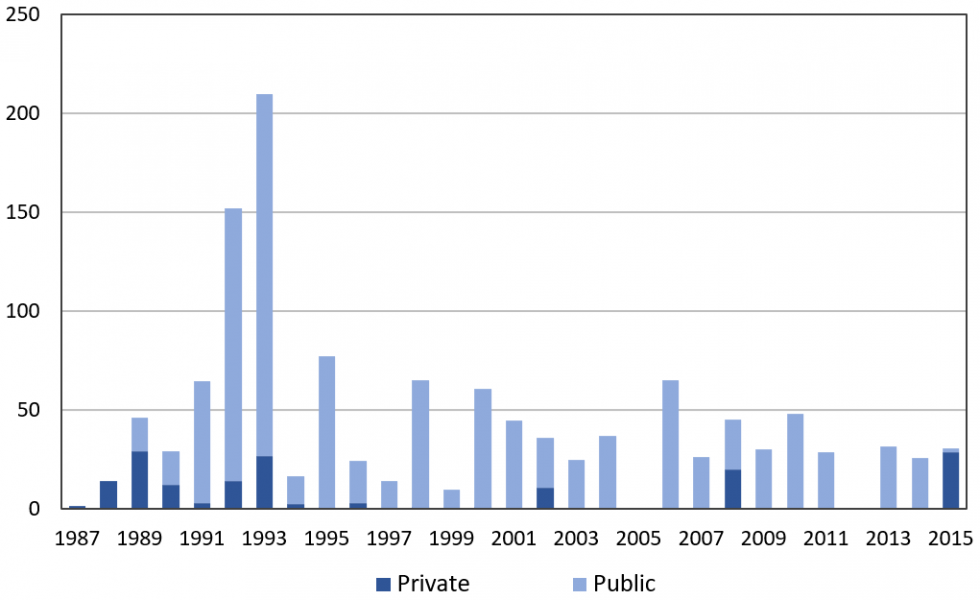

As regards players, two broad categories of debt-for-nature swaps have developed in practice: public and private swaps (see Chart 2). Between 1987 and 2015, most nature conservation funds funded by debt-for-nature swaps, amounting to approximately USD 1.25 billion, stemmed from public agreements (77% of the amounts).

Chart 2: Funds generated by debt-for-nature swaps, by category of players (USD billions)

Note: “Private” refers to non-governmental creditors (private sector entities or NGOs), “Public” refers to government. Sources: Sheikh (2018), authors’ calculations.

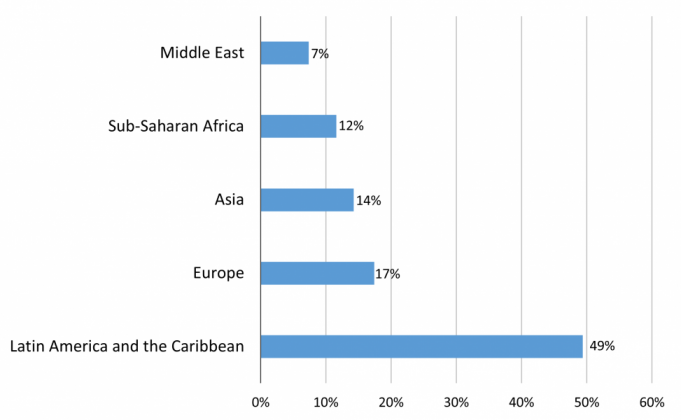

Geographically, most debt-for-nature swaps concerned Latin American and Caribbean countries, accounting for almost half of the funds generated (See Chart 3). In total, 39 countries benefited from debt-for-nature swaps between 1987 and 2015 (Sheikh, 2018).

Chart 3: Funds generated by debt-for-nature swaps, by debtor country (%)

Source: Sheikh (2018).

As regards the destination of the funds, most of the debt-for-nature swaps to date have given rise to compensations primarily aimed at limiting deforestation (Sommer et al., 2019).

This renewed interest first stems from the scientific community. Several publications (Essers et al., 2021; Caliari, 2020; CEPR, 2022; Volz et al., 2021; Weder di Mauro, 2021) call for the promotion of debt-for-nature swaps both in the post-pandemic context and in the context of the fight against climate change.

This interest can also be found, to some degree, among international and government circles. In April 2021, the IMF and the World Bank, for example, indicated that they were preparing proposals in this field.

Creditor countries have also taken an interest in the subject. In 2021, the US Treasury Department set up a working group on debt-for-nature swaps, and the European Commission commissioned a report on the subject (Lazard, 2021). In addition, several policy briefs from Chinese think tanks have highlighted the opportunity for China to enter into debt-for-nature swaps with countries along the New Silk Road (Steele and Patel, 2020; Yue and Nedopil Wang, 2021). This renewed interest in swaps is part of a broader movement to deploy new mechanisms linking debt sustainability and development assistance.1

Finally, several debtor countries have also expressed interest in reviving debt-for-nature swaps. For example, in June 2021, Argentina declared itself in favour of implementing debt-for-nature swaps to reduce its public debt while preserving the ecosystem services2 provided by its natural capital. Ecuador has proposed a 60,000 km² extension of the Galapagos Islands nature reserve, financed by a debt-for-nature swap.

Indeed, the current context calls for expanding debt-for-nature swaps to new areas. Recent proposals mention debt-for-climate swaps; the aim would be to enable low and middle-income countries to find some of the budgetary resources they lack to finance the heavy investments required for transitioning to a low-carbon economy or adjusting to climate change (IEA, 2021; Weder di Mauro, 2021; Volz et al., 2020).

In principle, the benefits of debt-for-nature swaps are clear. For recipient countries, the reduction in its public and external public debt burden eases the balance of payments constraint and enables funds to be reallocated to investments that are essential to mitigate climate change and protect biodiversity. For creditors, the debtor’s repayment capacity improves. Finally, for the international community, risks to financial stability and the environment are reduced.

In practice, however, reviving this mechanism poses major financial, environmental and governance-related challenges. It must also be supported by developments in financial engineering and market standards.

Economic and financial challenges

In order to produce sustainable results, debt-for-nature swaps must take place in a stable macroeconomic context. Practice shows, for example, that exchange rate instability, possibly coupled with high inflation, can erode the real value of a country’s nature conservation commitments and undermine their implementation over time (Resor, 1997).

Financially, the past practice of debt-for-nature swaps brings to light several difficulties.

On the one hand, their negotiation, especially when it is multilateral, is often complex and therefore lengthy (Essers et al., 2021). For example, the negotiations concluded in the Seychelles in 2015 lasted almost four years.

On the other, the swap is efficient if the principle of additionality is respected in two respects. For the creditor, this implies that debt relief is fully financed by additional resources, according to the Monterrey Consensus (UN, 2002). For the debtor, this means that the ecological compensation measures would not have been implemented in the absence of the debt swap. However, the assessment of additionality remains difficult (Cassimon et al., 2011).

Governance-related challenges

Debt-for-nature swaps pose governance-related challenges.

At the national level, the swap can lead to, or be perceived as leading to, a loss of sovereignty in the allocation of budgetary and natural resources by the debtor country. The funds generated by the swap are often paid out according to donor preferences, which are more or less aligned with national priorities in terms of nature conservation and meeting the needs of local populations.3

At the international level, the lack or, on the contrary, the abundance of standards for assessing, protecting and restoring ecosystems that are the subject of a debt-for-nature swap impedes the development of such mechanisms. The highly localised and specific nature of each swap partly explains this situation. In some respects, the absence of internationally recognised frameworks exposes creditors to a form of moral hazard. Indeed, the debtor country that benefits from a partial debt cancellation may end up developing solutions that contribute less than expected to nature conservation and the fight against global warming. Recent developments in the international financial system may reinforce a governance constraint. This lies in particular in the fact that largest creditors of certain indebted countries are not part of the collective forums for dealing with sovereign overindebtedness, most notably the Paris Club (Zettelmeyer, 2022). This new context penalises complex negotiations, such as those concerning debt-for-nature swaps.

Assessing the environmental gains from debt-for-nature swaps is difficult for two reasons.

First, the biophysical data needed to identify and assess the measures on a site-specific basis are not always available and are subject to considerable uncertainty. Systematically quantifying the ecological gain obtained from a euro of debt swap is therefore tricky. This partly explains the limited and mixed literature on this point: Sommer et al. (2019) consider that higher amounts of debt reduction and conservation funds generated by US debt swaps were associated with lower deforestation rates, while Kraemer and Hartmann (1993) do not identify an empirical relationship between these two variables. In the case of debt-for-climate swaps, measuring the real impact and additionality of a swap might seem simpler, but this depends on the existence of credible and consensual scenarios for comparing the gain obtained from the swap with a no-swap scenario. However, the diversity of scenarios and the uncertainty surrounding them mean that to each unit of debt relief may correspond different quantities of CO2 not emitted.

Second, the countries with the most urgent need for debt-for-nature swaps are not necessarily those with the greatest need for ecosystem protection. The correlation between deforestation and potential financial fragility is weak. The issues surrounding ecosystem stability are therefore not systematically linked to those surrounding economic and financial stability.

The fact that a debt-for-nature swap is not easily replicable limits its appeal. However, the attractiveness of debt-for-nature swaps can be enhanced by improving the financial engineering of the swaps, in several possible ways. The first approach is based on the development of certified “environmental credits”4 (e.g. carbon credits) that would be offered to the creditor at the time of the debt swap (Stiglitz and Rashid, 2020). This approach was implemented in a debt-for-wind power swap between Spain and Uruguay in 2005 (Essers et al., 2021). It aims to enable the creditor to meet the climate targets of the Paris Agreement (2015). The second approach consists in replacing debt with green bonds (including a haircut).

However, the large-scale development of these types of approaches depends on the stringent standardisation of the carbon offset market and/or the establishment of standards that make it possible to translate a unit of debt relief into a unit of ecological gain. Moreover, these market mechanisms could be perceived as a means for creditors to claim the environmental and climate efforts made by debtor countries as their own. This perception could be all the more prevalent as the production and consumption patterns of advanced countries are not changing. Furthermore, the discussions on Article 65 of the Paris Agreement at COP26 (2021) illustrate the sensitive nature of these issues.

———

In sum, swapping unsustainable debt for nature protection is a relevant proposal in principle. However, it cannot be seen as a systematic solution. From a climate and environmental point of view, debt-for-nature swaps do not (or only partially) meet the demand for solidarity expressed by low- and middle-income countries. In financial terms, such swaps will only moderately reduce the vulnerability of debtor countries to global financial cycles, whether these are driven by environmental degradation, economic development or a combination of both. Debt-for-nature swaps are therefore only a partial solution which, to be fully effective, must be part of a more comprehensive discussion on the evolution of the international financial system in the face of ecological challenges (Weder di Mauro, 2021).

IEA, International Energy Agency (2021). Financing Clean Energy Transitions in Emerging and Developing Economies, June.

World Bank (2021). International Debt Statistics 2021.

Caliari (A.) (2020). Linking Debt Relief and Sustainable Development: Lessons from Experience, coll. « Debt Relief for Green and Inclusive Recovery Project », background paper, No. 7, Heinrich Böll Foundation, Center for Sustainable Finance (SOAS, University of London) and Global Development Policy Center (Boston University), November.

Cassimon (D.), Prowse (M.) and Essers (D.) (2011). «The pitfalls and potential of debt‑for‑nature swaps: A US‑Indonesian case study», Global Environmental Change, Vol. 21, No. 1, February, p. 93‑102.

Unctad, United Nations Conference on Trade and Development (2021). “Debt relief and productive capacities key to recovery in middle-income countries”, June.

CEPR, Centre for Economic Policy Research (2022). Climate and Debt, coll. « Geneva Reports on the World Economy », No. 25, October.

De Bandt (O.), Jacolin (L.) and Lemaire (T.) (2021). « Climate Change in Developing Countries: Global Warming Effects, Transmission Channels and Adaptation Policies », Working Paper, No. 822, Banque de France, July.

Essers (D.) Cassimon (D.) and Prowse (M.) (2021). « Debt‑for‑climate swaps in the COVID‑19 era: Killing two birds with one stone? », Analysis and Policy Brief, No. 43, University of Antwerp, March.

IMF, International Monetary Fund (2021a). Fiscal Monitor. Strengthening the Credibility of Public Finance, October, p. 15 (box 1.2).

IMF (2021b). « The G20 common framework for debt treatments must be stepped up », IMF Blog, 2 December.

IMF (2022b). World Economic Outlook and Fiscal Monitor (Database), April.

IPCC, Intergovernmental Panel on Climate Change (2021). « Summary for policymakers », Climate Change 2021: The Physical Science Basis. Contribution of Working Group I to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change, October.

IPBES, Intergovernmental Science-Policy Platform on Biodiversity and Ecosystem Services (2019). The global assessment report on biodiversity and ecosystem services, May.

Jayachandran (S.) et al. (2017) « Cash for carbon: A randomized trial of payments for ecosystem services to reduce deforestation », Science, Vol. 357, No. 6348, July, p. 267‑273.

Kraemer (M.) and Hartmann (J.) (1993). « Policy responses to tropical deforestation: Are debt‑for‑nature swaps appropriate? », The Journal of Environment & Development, Vol. 2, No. 2, Summer, p. 41‑65.

Lazard (2021). Debt‑for‑SDGs swaps in indebted countries: The right instrument to meet the funding gap? – A review of past implementation and challenges lying ahead, September.

Levrel (H.) (2020). Les compensations écologiques, Éditions La Découverte, coll. « Repères », No. 749, November.

Lovejoy (T. E.) and Nobre (C.) (2018). « Amazon Tipping Point », Science Advances, Vol. 4, No. 2, February.

NGFS, Central Banks and Supervisors Network for Greening the Financial System (2019). A call for action. Climate change as a source of financial risk, First comprehensive report, April.

NGFS and INSPIRE (2022). « Central banking and supervision in the biosphere: An agenda for action on biodiversity loss, financial risk and system stability. Final Report of the NGFS‑INSPIRE Study Group on Biodiversity and Financial Stability », NGFS Occasional Paper, March.

UN, United Nations (2002). Monterrey Consensus of the International Conference on Financing for Development, 18‑22 March, p. 17 (§ 49).

Persson (L.) et al. (2022). « Outside the safe operating space of the planetary boundary for novel entities », Environmental Science & Technology, No. 56(3), p. 1510‑1521, January.

Resor (J. P.) (1997). « Debt‑for‑nature swaps: A decade of experience and new directions for the future », unasylva, Vol. 48, FAO (Food and Agriculture Organization of the United Nations), January.

Ripple (W.) et al. (2017). « Extinction risk is most acute for the world’s largest and smallest vertebrates », PNAS (Proceedings of the National Academy of Sciences of the United States of America), Vol. 114, No. 10, September.

Sheikh (P. A.) (2018). Debt for Nature Initiatives and the Tropical Forest Conservation Act (TFCA): Status and Implementation, United Nations Congress, July.

Sommer (J. M.) et al. (2020). « The United States, bilateral debt‑for‑nature swaps, and forest loss: A cross‑national analysis », The Journal of Development Studies, Vol. 56, No. 4, p. 748‑764.

Steele (P.) and Patel (S.) (2020). « Tackling the triple crisis. Using debt swaps to address debt, climate and nature loss post‑COVID‑19 », Shaping Sustainable Markets Papers, International Institute for Environment and Development (IIED), September.

Stiglitz (J.) and Rashid (H.) (2020). « Averting catastrophic debt crises in developing countries. Extraordinary challenges call for extraordinary measures », CEPR Policy Insights, No. 104, Centre for Economic Policy Research, July.

Volz (U.) et al. (2020). Climate Change and Sovereign Risk, Center for Sustainable Finance (SOAS, University of London), Asian Development Bank Institute, World Wide Fund for Nature, Four Twenty Seven and INSPIRE, October.

Volz (U.) et al. (2021). Debt Relief for a Green and Inclusive Recovery: Securing Private‑Sector Participation and Creating Policy Space for Sustainable Development, coll. « Debt Relief for Green and Inclusive Recovery Project », Heinrich Böll Foundation, Center for Sustainable Finance (SOAS, University of London), Global Development Policy Center (Boston University), June.

Weder di Mauro (B.) (2021). « Debt for climate swaps make sense », PS Quarterly, Project Syndicate, December.

Yue (M.) and Nedopil Wang (C.) (2021). Debt‑for‑Nature Swaps: A Triple Win Solution for Debt Sustainability and Biodiversity Finance in the Belt and Road Initiative (BRI)?, IIGF Green BRI Center, January.

Zettelmeyer (J.) (2022). « Using debt‑for‑climate swaps to solve two crises at once », webinar, Boston University Global Development Policy Center, 13 January.

See in particular the C2D mechanism (Debt Reduction- Development Contract) for debt restructuring.

Sound ecosystems provide so-called ecosystem services (supply of materials and water, climate regulation, pollination, etc.) on which economic activities depend.

See, in particular, Jayachandran et al (2017): this randomised controlled trial (RCT) carried out in Uganda shows that a cash payment made to households owning forest plots in return for adopting “sustainable” management practices makes it possible to significantly limit deforestation.

“Environmental credits” are certificates or benefits (grants, donations or other) certified by a competent authority in return for a measure to protect, compensate or restore a natural environment.

Article 6 of the Paris Agreement aims to establish mechanisms for voluntary cooperation between States to achieve the greenhouse gas emission reduction targets set out in their nationally determined contributions (NDCs).