China has continuously gained market shares in the EU import market since 2000. At the same time, Germany’s share in EU imports has declined since 2005. This divergence is particularly relevant for sophisticated manufacturing products in which Germany is specialized. The diverging trends can be found for all depicted 2-digit-sectors. Moreover, China’s gains and Germany’s losses in the EU market accelerated between 2020 and 2022 in many respects – which would be in line with China plans to upgrade its production structure, e.g. in the course of the strategy ‘Made in China 2025’. This development raises questions about the competitive distortions emanating from China’s state capitalism and about appropriate trade policy responses.

A recent study by Matthes (2023a) examined whether China is increasingly outcompeting with Germany in those manufacturing sectors where the German economy has its strengths. To investigate this question, the changes in China’s and Germany’s shares of EU imports are analysed descriptively over the period 2000 to 2022.

The overall results are remarkable:

The analysis is carried out on different levels of aggregation in the trade statistics based on the CPA-goods classification and on data from Eurostat.

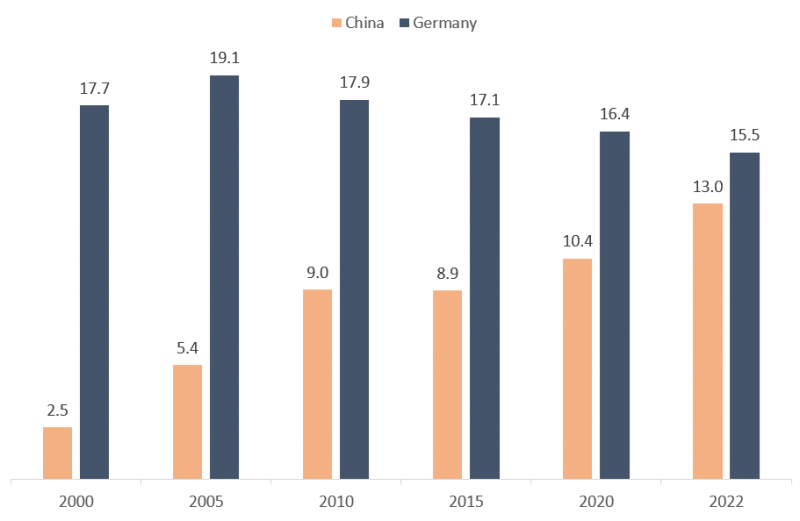

First, on a highly aggregate level, total merchandise EU-imports are considered as well as total EU-imports of sophisticated manufacturing goods, in which the German economy specialises (Figure 1). The share of EU-imports from Germany in sophisticated manufacturing goods stood at 19.1 percent in 2005. It was thus significantly higher than for merchandise goods overall (15.3 percent), indicating that Germany specializes in the depicted sophisticated manufacturing goods. However, Germany’s share in EU imports in sophisticated manufacturing goods declined to 15.5 percent in 2022. In parallel, Chinas share in EU imports in sophisticated manufacturing goods increased from only 2.5 percent in 2000 (and 5.4 percent in 2005) to 13.0 percent in 2022. A particularly sharp increase is registered between 2020 (10.4 percent) and 2022.

Another interesting feature underscores China’s increasing focus on higher value sectors. The share of sophisticated manufacturing goods in EU-imports from China increased continuously and significantly from 51 percent in 2000 to nearly 73 percent in 2022. At the same time, the share of sophisticated manufacturing goods in EU-imports from Germany has recently declined somewhat to 61 percent.

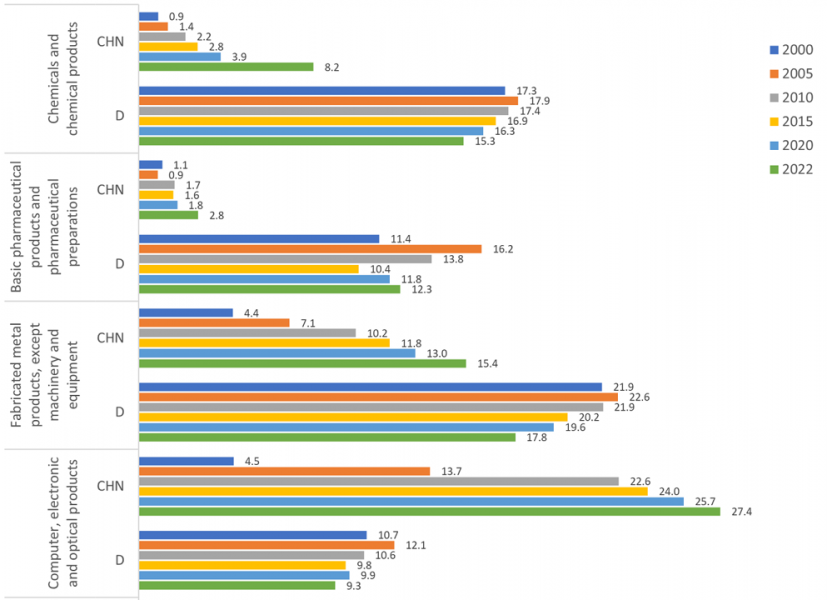

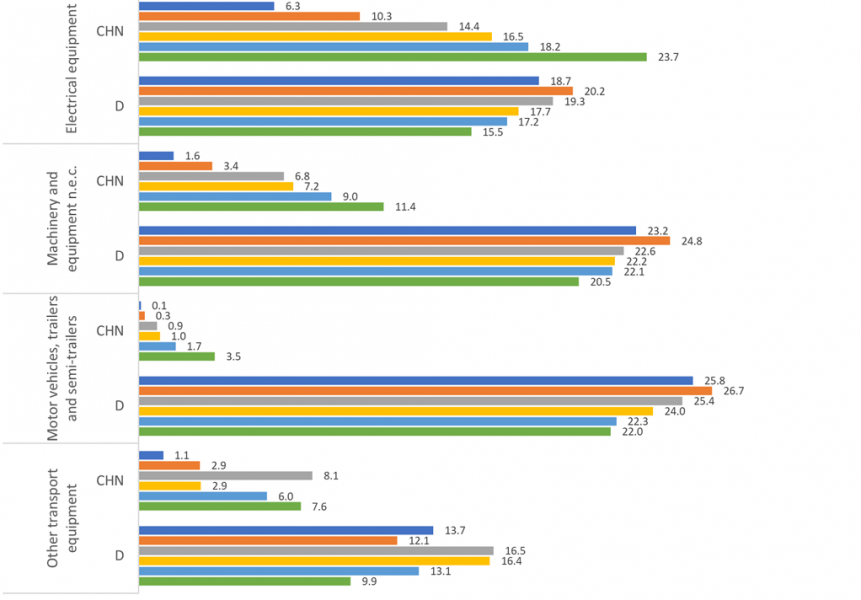

In a second step, EU imports of sophisticated manufacturing goods are analysed in more detail at the 2-digit product level of the CPA classification (Figure 2). First, share levels in 2022 are considered and then share changes over time. The level of EU import shares from China and from Germany differs significantly between the groups under consideration. In most product groups, the German economy is more strongly represented on the EU market than the Chinese. This is quite clearly the case for motor vehicles and for machinery, with shares of just over 20 per cent, and not quite as pronounced for pharmaceutical products. However, China has been clearly ahead of Germany for more than ten years in IT and optical equipment etc. Regarding electrical equipment, China only recently overtook Germany, but it significantly increased its lead between 2020 and 2022. While China was only 1 percentage point ahead of Germany in 2020, by 2022 it was already a good 8 percentage points in front.

Figure 1: EU-Imports of sophisticated manufacturing goods from China and Germany

Note: Selection of product groups included: CPA-Classification on 2-digit level: Chemicals and chemical products (Classification no. 20), Basic pharmaceutical products and pharmaceutical preparations (21), Fabricated metal products, except machinery and equipment (25), Computer, electronic and optical products (26), Electrical equipment (27), Machinery and equipment n.e.c. (28), Motor vehicles, trailers and semi-trailers (29), Other transport equipment (30).

Sources: Eurostat, 2023; German Economic Institute (Institut der deutschen Wirtschaft).

Figure 2: Figure 2: EU-Imports of sophisticated manufacturing goods from China and Germany in 2-digit product groups (CPA-Classification)

Shares in percent

Sources: Eurostat, 2023; German Economic Institute (Institut der deutschen Wirtschaft).

The development of EU import shares over time is also cause for certain concern in several other industrial sectors. China has recently been able to further increase its share in all of the industrial product groups considered, in some cases very significantly. In contrast, Germany’s share of EU imports continued to fall almost everywhere:

In many cases, the changes were significant between 2020 and 2022 compared to former periods, indicating also from this perspective that the diverging trends appear to have accelerated.

Third, when 4-digit product groups of sophisticated manufacturing products are considered, a similar picture emerges. Out of 85 a total of product groups, in 77 groups China’s share in EU imports increased between 2020 and 2022. Germany’s share changes, however, are negative in 69 out of 85 cases. Obviously, Chinese share gains in sophisticated industrial products are accompanied by German share losses in most cases (62 out of 85).

As shown, Chinese share gains and German share losses often go hand in hand. Although no causality is examined in this report, this finding strongly suggests that China is increasingly competing with the German economy in its EU home market and in sectors where it has been traditionally strong.

The problem is that China’s export successes are likely to be also based on extensive and widespread subsidies, which raises the question of trade policy responses. It is true that China is also catching up in terms of technology, education and research. However, it is combining the resulting true and basic competitiveness with intensive industrial policy subsidies (Matthes, 2020a; Chimits, 2023; OECD, 2023). With the Made in China 2025 strategy, the government uses massive subsidies to make the Chinese economy an innovation leader in the long term, including in sectors in which the German economy has its specialisation advantages (Zenglein/Holzmann, 2019). This combination poses threats to German export markets worldwide – including the risk of welfare losses for Germany as a whole (Matthes, 2020b). The information on the relevance of competitive pressure from China is surprisingly sparse in the economic literature (Matthes, 2021a; 2021b). According to a survey by the German Economic Institute (IW), German industrial companies already attributed significantly greater importance to competitive pressure from Chinese companies than to protectionism at the end of 2020 (Matthes, 2021b).

More generally, the empirical findings raise concerns about the German industrial export model – not only regarding increasing competitive pressures from China but also in view of the energy transition challenges and the fundamental competitiveness problems in Germany.

Overall, the German industrial export model seems to be getting into trouble.

Chimits, François, 2023, What Do We Know About Chinese Industrial Subsidies?, CEPII Policy Brief No. 2023- 42, Paris What Do We Know About Chinese Industrial Subsidies? (cepii.fr) [4.8.2023]

Eurostat, 2023, CPA 2008 – Statistical Classification of Products by Activity, CPA 2008 – CPA – Eurostat (europa.eu) [16.7.2023]

Matthes, Jürgen, 2020a, China’s Market Distortions and the Impact of the Covid-19 Crisis, in: CESifo Forum, Nr. 3, S. 42–48, München, https://www.cesifo.org/DocDL/CESifo-Forum-2020-3-matthes-china%E2%80%99s%20market%20distortion-september.pdf [4.8.2023]

Matthes, Jürgen, 2020b, Technologietransfer durch Unternehmensübernahmen chinesischer Investoren, in: Wirtschaftsdienst, 100. Jg., Nr. 8, S. 633–639, https://www.wirtschaftsdienst.eu/inhalt/jahr/2020/heft/8/beitrag/technologietransfer-durch-unternehmens-uebernahmen-chinesischer-investoren.html [4.8.2023]

Matthes, Jürgen, 2021b, Konkurrenzdruck durch China auf dem EU-Markt. Ein tiefer Blick in Außenhandelsstatistik und Industriebranchen, IW-Report, Nr. 30, Köln, Konkurrenzdruck durch China auf dem EU-Markt: Ein tiefer Blick in Außenhandelsstatistik und Industriebranchen – Institut der deutschen Wirtschaft (IW) (iwkoeln.de) [4.8.2023]

Matthes, Jürgen, 2021a, Wettbewerbsverzerrungen durch China – Akademische Evidenz und Ergebnisse einer Befragung deutscher Unternehmen, IW-Report, Nr. 10, Köln https://www.iwkoeln.de/fileadmin/user_upload/Studien/Report/PDF/2021/IW-Report-2021_Wettbewerbsverzerrungen-China.pdf [4.8.2023]

Matthes, Jürgen, 2023a, Entwicklung des Konkurrenzdrucks durch China auf dem EU-Markt, IW-Report, Nr. 39, Köln https://www.iwkoeln.de/fileadmin/user_upload/Studien/Report/PDF/2023/IW-Report_2023-China-Konkurrenz-in-EU.pdf

Matthes, Jürgen, 2023b, Wie ist der starke Importanstieg aus China im Jahr 2022 zu erklären und wie haben sich die Import-Abhängigkeiten entwickelt?, IW-Report, Nr. 34, Köln https://www.iwkoeln.de/studien/juergen-matthes-wie-ist-der-starke-importanstieg-aus-china-im-jahr-2022-zu-erklaeren-und-wie-haben-sich-die-import-abhaengigkeiten-entwickelt.html [4.8.2023]

OECD – Organisation for Economic Co-operation and Development, 2023, Government support in industrial sectors, A synthesis report, OECD Trade Policy Paper, Nr. 270, Paris, https://www.oecd-ilibrary.org/docserver/1d28d299-en.pdf?expires=1691133139&id=id&accname=guest&checksum= D1CC3904170A08EEAB34D134708D16D0 [4.8.2023]

Zenglein, Max J. / Holzmann, Anna, 2019, Evolving made in China 2025. China’s industrial policy in the quest for global tech leadership, Merics Papers on China, Nr. 8, Berlin