Over the past year, commodity prices and the US dollar have moved in tandem. This represents a stark contrast to the traditional relationship between the two variables. While some specific factors could account for some of the unusual joint behaviour of the US dollar and commodity prices, persistent structural factors were also at work. In particular, the United States’ emergence as a net energy exporter means that higher commodity prices now triggers an improvement in the US terms of trade – the ratio of US export prices to US import prices – rather than a deterioration, as in the past. Because there is a stable long-run positive relationship between the US terms of trade and US dollar appreciation, higher commodity prices are now more likely to coincide with US dollar appreciation, in contrast to historical patterns. Changing correlation between the US dollar and commodity prices has implications for commodity importers and exporters.

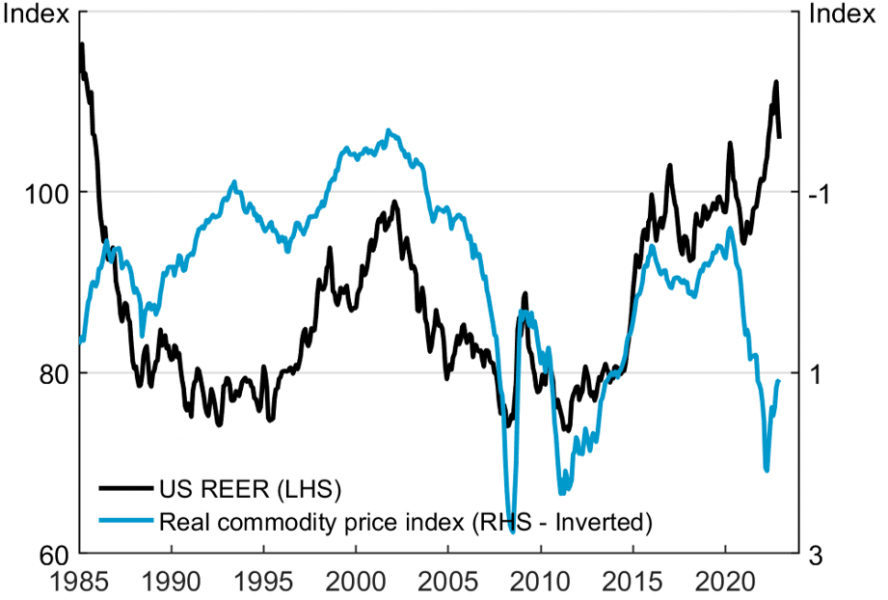

Over the past year, commodity prices and the value of the US dollar have moved in tandem. In early 2022, rising commodity prices went hand-in-hand with US dollar strength. More recently, commodity prices and the US dollar both retreated. These patterns are in stark contrast to the usual relationship between commodity prices and the US dollar (Figure 1). Historically, higher commodity prices have coincided with US dollar weakness.

Figure 1: US real exchange rate and commodity prices

Admittedly, the link between commodity price and US dollar movements is not hard-and-fast. Commodity prices and the dollar have at times moved at odds to the usual pattern. But the recent departure has been unusually large and persistent (Rees, 2023). It magnified the stagflationary effects of higher commodity prices on commodity importers and dampened the stabilising role of the exchange rate for commodity exporters (Hofmann et al, 2023).

Will familiar correlations between commodity prices and the US dollar return? Or will recent patterns become the norm?

There are some reasons to expect standard relationships to return. Economic developments in 2022 were unusual. The Russian invasion of Ukraine curbed oil and gas supply, raising commodity prices, while prompting a flight-to-safety in financial markets that boosted the dollar. Monetary tightening, which began earlier and proceeded faster in the United States than elsewhere, further bolstered the dollar. As the effects of these developments fade, traditional correlation patterns between the US dollar and commodity prices could re-assert themselves.

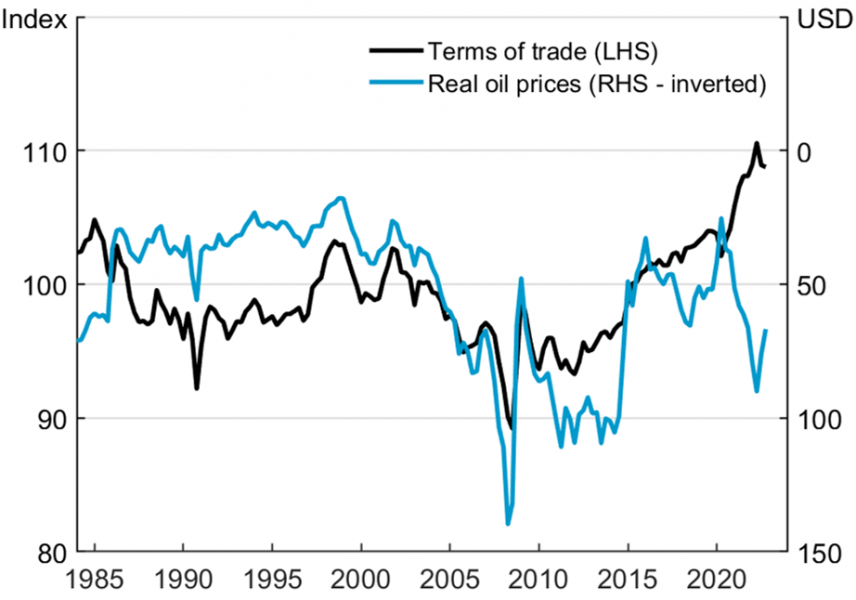

But there are also reasons to expect recent patterns to persist. A key one is a shift in US trade composition. Over the past decade, the United States has become a net energy exporter. This altered the relationship between commodity prices and the US terms of trade – the ratio of US export prices to US import prices. In the past, higher commodity prices worsened the US terms of trade. Today, the opposite is true (Figure 2). Formal econometric tests for structural breaks confirm this visual evidence, and reveal that the shift began around the start of the US shale oil boom and accelerated as the US became a net energy exporter.

Figure 2: US terms of trade and oil prices

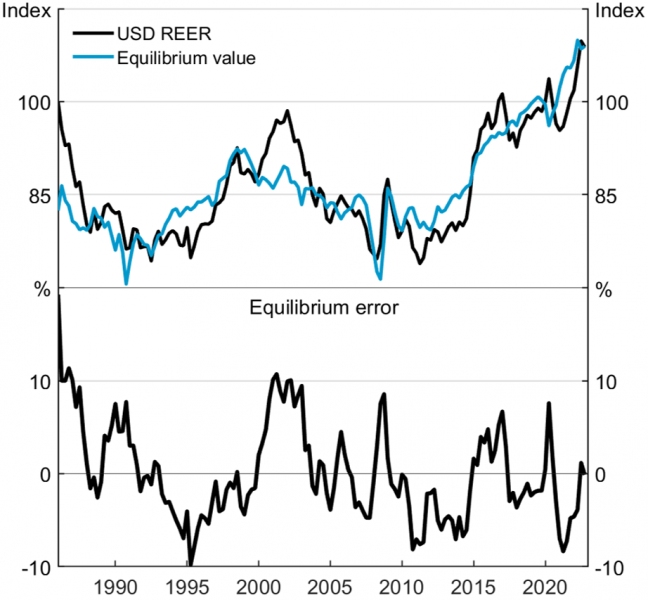

Shifting trade patterns matter because there is a strong and stable long-run relationship between the US dollar and the US terms of trade. When the US terms of trade improves, the dollar tends to appreciate. And when the US terms of trade worsens, the dollar typically weakens. In Rees (2023), I show that this relationship holds even after controlling for factors such as interest rate differentials and investor risk aversion. The relationship between the US dollar and US terms of trade resembles that previously documented for the “commodity currencies” of leading commodity exporters including Australia and Canada (Chen and Rogoff, 2003). When the US was an energy importer, past higher commodity prices would lower the US terms of trade and weaken the dollar. Today, the opposite is true. And, far from being an anomaly, this relationship suggests that the US dollar traded at about its fair value for much of 2022, given movements in commodity prices, interest rate differentials and risk aversion (Figure 3).

Figure 3: US real exchange rate and model-based “equilibrium” value

So long as the US remains a net energy exporter, higher commodity prices are likely to coincide with US dollar appreciation. This conclusion has several policy implications for non-US economies. Because commodity prices are quoted in US dollars, commodity importers will face greater commodity price volatility when measured in local currencies. Already, commodity price booms tend to be stagflationary for these economies – they raise inflation and lower growth. The stagflationary pressures will be even larger if coupled with a stronger US dollar, which also tends to be contractionary for the world economy (Bruno and Shin, 2015, 2023). Commodity exporters will also face challenges. Traditionally, flexible exchange rates have been a shock absorber for these economies, weighing on economic growth in commodity booms while supporting it when commodity prices fell (Manalo, Pereira and Rees, 2015). The shock absorbing capacity will be considerably reduced if commodity-exporter exchange rates no longer move as much relative to the US dollar in commodity booms and busts. As such, other policies – including monetary and fiscal policy – may need to play a larger role in stabilising these economies in the face of commodity price booms and busts.

Bruno, V. and H. S. Shin (2015), “Capital flows and the risk-taking channel of monetary policy”, Journal of Monetary Economics, 2015, vol 71, pp 119-132.

_ and _ (2023), “Dollar exchange rate as a credit supply factor – evidence from firm-level exports”, BIS Working Papers No. 819.

Chen, Y. and K. Rogoff (2003), “Commodity Currencies”, Journal of International Economics, vol 60, pp. 133-160.

Hofmann, B, D Igan and D Rees (2023), “The changing nexus between commodity prices and the dollar: causes and implications”, BIS Bulletin, no, 74.

Manalo J., D. Perera and D. M. Rees (2015), “Exchange rate movements and the Australian Economy”, Economic Modelling, vol 27, pp. 53-62.

Rees, D. M., (2023). “Commodity prices and the US Dollar”, BIS Working Papers No. 1083.