Energy commodities and commodity derivatives on energy and emissions are of growing importance for the transition to a more carbon-neutral European economy. Climate Change Risks (CCRs), both physical and transitional, have already led to events with profound consequences for these markets and their participants. By analysing EMIR Trade Repository data on energy and environmental derivatives for the euro area we gain valuable insight into how energy markets and existing clearing practices function. Our research shows that the clearing rate is highly dependent on the type of product and that cleared markets are concentrating towards a single central counterparty (CCP). We further show that CCR- related events impact the business of CCPs. As CCRs are here to stay, it is important for market participants, as well as authorities and regulators, to take these risks into account.

This research on European Market Infrastructure Regulation (EMIR) Trade Repository (TR) data of the Euro Area (EA) intends to promote knowledge and a better understanding of how the EA commodity derivatives on Energy and Emissions and related clearing practices interact. The recent volatility in energy markets triggers the question of how these markets function. Furthermore, commodities (energy) and commodity derivatives on energy and emissions are of growing importance for the transition to a more carbon-neutral European economy. Greater knowledge of how these markets interact, in combination with existing clearing practices, is therefore of increasing relevance. Climate Change Risks (CCRs), both physical and transitional, have already led to some events with profound consequences for these markets and their participants. This may pose a challenge in the future as it is expected that commodities and commodity derivatives markets will become increasingly important. Overall, specific disruptions in the commodity derivatives market caused by CCRs could potentially have an impact on the business of a CCP.

We start this brief with a market overview of energy and environmental derivatives. We then describe the impact of the climate related Nasdaq event on these markets. The results provide valuable insight into market participants and their clearing behaviour. We conclude with our main observations relevant for market participants and policy makers.

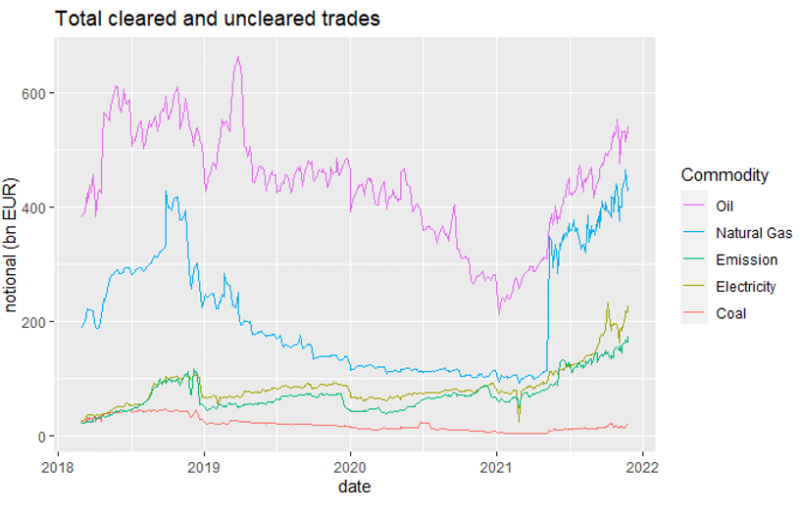

Figure 1 provides a complete market overview of the main energy and environmental derivatives market per commodity type (March 2018 until November 2021).

Figure 1: Market overview of the complete market in notional in bn EUR for the period March 2018 until November 2021

A correlation between the total notional of emission and electricity derivatives is clearly visible. This correlation can be explained by the requirement to hold emission certificates for electricity generation that causes greenhouse gas emissions, such as burning coal. The falls in the notional for all commodities at the end of every calendar year could be driven by accounting rules (year-end as reference date for capital requirements, prompting counterparties to decrease their exposures).

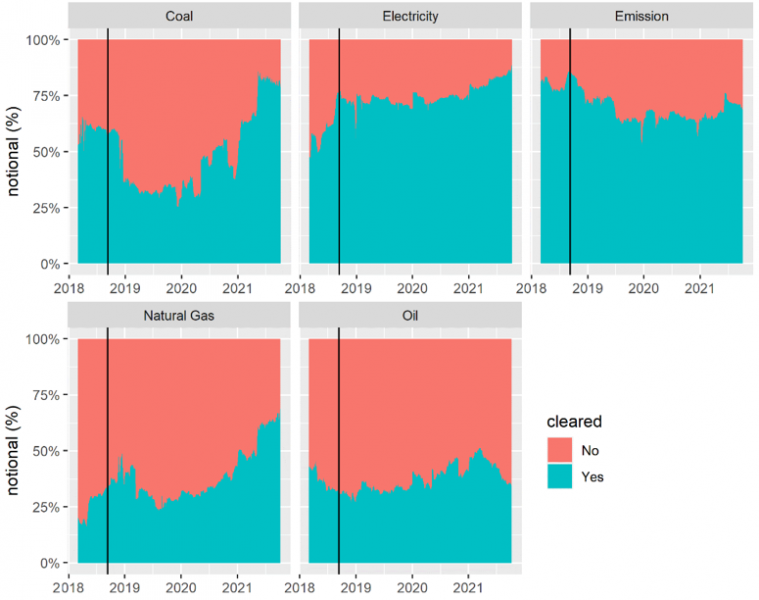

Figure 2 below shows the notional per commodity that is cleared at a CCP as a percentage of the total notional of cleared and uncleared trades over time, also called clearing rates. The black line indicates the time of the climate-related event we will discuss in Section 3. We find significant differences in these clearing rates between commodities. Looking at the years from 2018 till 2021, the clearing rate is the highest for the electricity and emission derivatives markets. For coal and natural gas derivatives, the clearing rate increased significantly after 2018, reaching levels of around 65% and 75% respectively of notional being cleared in November 2021. We find that these increased clearing rates in 2021 are the result of growth in the cleared market, while the size of the uncleared markets stays the same. Only around 30% of the outstanding notional in oil derivatives was cleared, which was significantly less than other energy commodities.

Figure 2: Percentage of notional cleared over time per commodity

Although oil derivatives have the lowest clearing rate of all energy commodities, it is the largest cleared market in absolute terms, since its total market share is much larger than the other commodity derivatives. It was not until the end of 2021 that the cleared notional of natural gas surpassed that of oil, due to the significant increase in natural gas prices. The same is true for the cleared electricity market, which was around the same size as oil at the end of 2021.

The second part of our research focuses on the impact of a climate-related event in September 2018. This so-called “Nasdaq event” caused a clearing member to default as the result of a combination of changes in the EU emissions policy and volatile electricity prices. The event took place in the electricity derivatives market, but as the event was also driven by a change in emissions policy, we provide overviews of both the cleared emission and electricity derivatives markets before zooming in on the event itself and the individual clearing members’ behaviour.

Considering the cleared emission derivatives market more broadly, this market has four active CCPs (each with a notional of over €1 bn a day). We find that the notional increased in 2018 for all CCPs up to the time of the event, and stabilised shortly thereafter until the end of 2018, when the notional fell drastically. As a result of the overall increased growth and volatility in energy prices, markets appear to have been experiencing substantial growth since the start of 2021. The more recent market turmoil since 2021 has not caused any default events among clearing members.

We also find an effect of an emissions policy change; the amendment to the Market Stability Reserve (MSR) was introduced in 2015 to control the flows of EU Allowances (EUAs) into the market each year with the aim of lifting carbon prices. Between May 2017 and September 2018, the prices of EUAs rose significantly, from €5 to €25 per tonne, due to the MSR policy change. We find that the notional increased for all CCPs up to the time of the event and stabilised shortly thereafter, reflecting the drastic price increase of emission rights in the first half of 2018, which came to a halt in September 2018 due to the MSR policy change. This behaviour is also visible in Figure 1, reflected by 300% growth in outstanding (cleared and uncleared) notional in September 2018 compared to March 2018. We find that the cleared market showed even stronger growth in notional of around 500%.

As for emissions, we analysed the notional per CCP in the electricity derivatives market and its movement over time. In the electricity derivatives market, more CCPs are found to be active (seven CCPs) compared to the emissions derivatives market (four CCPs). It is noteworthy that the electricity derivatives market is dominated by one large CCP. The smaller six CCPs have comparable market shares. Also, there is a strong correlation between the emission and electricity derivatives markets. Hence, we see a sharp increase in notional in the first half of 2018, followed by a drop at the end of the year. Since early 2019, the outstanding notional in electricity derivatives had remained stable, with no major impact at the start of the coronavirus pandemic in March 2020. Starting in 2021, however, and in parallel with emission derivatives, the outstanding notional in electricity derivatives increased strongly, with almost exponential growth as of summer 2021, which, in hindsight, appeared to foreshadow the further increases seen in 2022.

The Nasdaq event took place in September 2018. This event was triggered by the widening spread of Nordic and German electricity prices in combination with the previously mentioned emissions policy change (the amendment of the MSR). In September 2018, unanticipated high rainfall after a dry summer affected Nordic electricity prices. At the same time, German electricity prices increased because of the amendment of the MSR. Due to positions relying on the correlation between Nordic and German electricity prices, these margin calls eventually led to the default of a clearing member1. The default also affected other clearing members of Nasdaq who had to make contributions to compensate for losses.

Interestingly, no disruption in the market on the day of the event is visible, even though a default took place. This can be explained by the longer maturity of derivatives. It takes time for clearing members and clients to decrease their positions by either selling their contracts or waiting for them to mature. As in the case of the emissions market, we do find a larger drop in outstanding notional at the end of 2018 without a rapid recovery in the following year, indicating that matured contracts were not renewed.

We analysed the behaviour of clearing members around the time of the event to see whether clearing members moved their clearing business to other CCPs. Some movement is visible, however there is no evidence that this movement can be explained solely by the default at Nasdaq.

The management of the default also required a financial contribution from non-defaulting clearing members and their clients, that might have motivated clearing members to stop clearing at Nasdaq. However, this could also be the result of the new risk measures and policy changes made by Nasdaq in response to the event. The measures include, for example, stricter access policies for clearing members. It is also important to note that moving clearing businesses to another CCP is subject to limitations, as not all products are cleared at all CCPs, and restrictions.

The level of concentration of the clearing market for emissions and electricity merits further attention from policymakers. About 70% of the emission derivatives are cleared. The clearing market for this product is concentrated. Three out of four of the CCPs clearing these products are in the EU, one of which is in the EA. Due to the growing importance of the EU Emissions Trading System and the related importance of clearing facilities for market participants, this is an important finding that could merit further attention from policymakers, supervisors and market participants. About 80% of electricity derivatives are cleared. The clearing market for this product is less concentrated but is dominated by a single CCP. Of the seven CCPs, six are in the EU, of which four are in the EA and one in the rest of the world. The correlation between electricity and emissions is strong because electricity production often requires the use of emission allowances.

A specific feature of the electricity and emission derivatives market is its vertically connected structure, embedded in larger trading groups. The research shows a concentration of trading venues with a significant link to their own CCPs. Such a vertical structure can be beneficial for innovation and efficient trading and clearing. However, it often means little choice for market participants and the non-existence of a backup possibility.

Due to the limited number of trading venues and connected CCPs, market participants have little choice when it comes to diversifying their business. Trading venues and CCPs have their own access policies that can be adjusted when deemed necessary, for example after certain events. This could lead to a further reduction in choice, triggering further concentration or a movement towards non centrally-cleared trading.

Transmission channels in the ecosystem of energy and emission derivatives could lead to systemic risk. This research describes a climate change-related event that took place some years ago. In the meantime, several other climate change situations have occurred, for example at the beginning of 2021 due to an unusually chilly winter in the US. Moreover, as we were able to include data up to and including November 2021, the start of the turmoil in energy markets (significant rises in the price of natural gas in October) is also included in the data. This price volatility prompted both trading venues and CCPs to act and thus interact. Improved knowledge and understanding of these interactions and their influence on access, margin calls and other mitigation measures is deemed necessary to better understand possible risks.

This was an atypical clearing member, who, we expect, will not be allowed to be a direct clearing member in the current settings.