This policy brief is based on European Central Bank Working Paper Series No. 2849. The views expressed are those of the authors and do not necessarily reflect those of the European Central Bank (ECB).

This brief examines how risk-sharing channels have evolved over time in the United States and the Euro Area, and whether they have operated as ‘complements’ or ‘substitutes’, i.e. if they have reinforced each other or if the improvement of one channel has been associated with the weakening of another one. We focus on the capital channel (income from cross-border ownership of assets), the credit channel (interstate and cross-country lending, or domestic savings), and the fiscal channel (federal or international fiscal transfers). We offer three main contributions. First, we propose an empirical model which allows us to formally quantify time variation in risk-sharing channels, over the last decades. Second, we develop a new test of the complementarity vs. substitutability hypothesis of the three risk-sharing channels, based on the correlation between the impulse responses of these channels to idiosyncratic output shocks. Third, for the United States, we explain time variation in the risk-sharing channels based on some key macroeconomic and financial variables. Our results have important implications for the reform of the EMU’s governance framework. We show that there is substantial room to strengthen the shock-absorption capacity of the EMU.

There are two fundamental and nested dimensions in the debate about how countries in monetary union can counteract macroeconomic shocks affecting locally their economies. The first concerns the mechanisms available at a national level to reduce exposure to risks or to mitigate their effects (e.g., eliminating price and wage rigidities, building fiscal buffers and using them in a countercyclical way). The second concerns the notion of international risk-sharing, which plays a central role in this debate, given that it relates to the cross-border channels available to insure against idiosyncratic or country-specific output shocks (as opposed to shocks hitting the monetary union as a whole).

This brief focuses on this latter dimension, and analyses how states within the United States (US) and countries in the euro area (EA) have “shared risks” over the last decades. In particular, we focus on how countries and states have insured risks via capital and credit markets, and via fiscal transfers. Indeed, agents in a given country or state hit by a negative idiosyncratic shock may alleviate the effects of such shock by receiving income, such as dividends from financial assets held in other regions not affected by this shock (capital channel), by obtaining bank loans and official financial assistance from other jurisdictions, or using domestic savings (credit channel), and by benefiting from fiscal transfers from abroad (fiscal channel).

We offer a fresh view in this debate along three different dimensions. First, we assess whether the contribution of these three risk-sharing channels has varied over time, which might be explained by several structural and institutional changes that have occurred in the US and the EA over the last decades. Second, we analyse whether a possible increase (decrease) in the contribution of one channel has been associated with an increase (decrease) in the contribution of the other channels. In other words, we study whether the capital, credit and fiscal channels have operated as ‘complements’ or ‘substitutes’. Third, in the case of the US, we identify potential macroeconomic and financial factors underlying the dynamics of the time-varying risk-sharing channels.

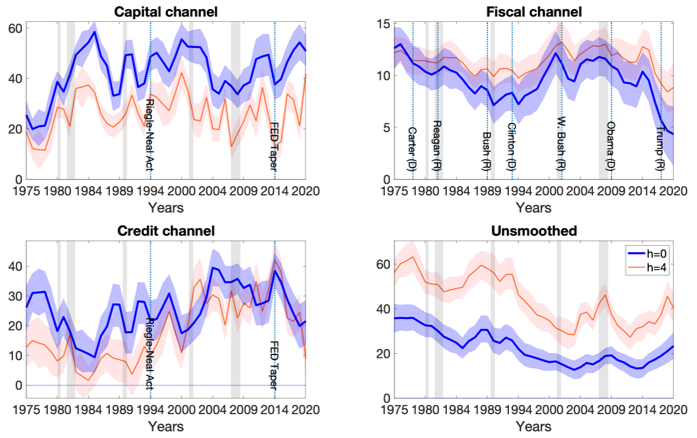

Based on the 1975-2020 sample for the US, and on the 1998-2023 sample for the EA, we find substantial time variation in the risk-sharing mechanism, for both regions, as displayed in Figures 1 and 2 respectively. The overall level of shock absorption has increased since the 1970s in the US, as reflected in a declining share of unsmoothed shocks. However, this improvement has halted in the last decade, in particular since the Great Financial Crisis (GFC) of 2008-2009. The developments of the first three decades have been mainly driven by private risk-sharing channels (i.e., the capital and credit channels), whereas the federal tax/transfer system absorbed around 10% of the shock initially, which decreased to below 5% in recent years.

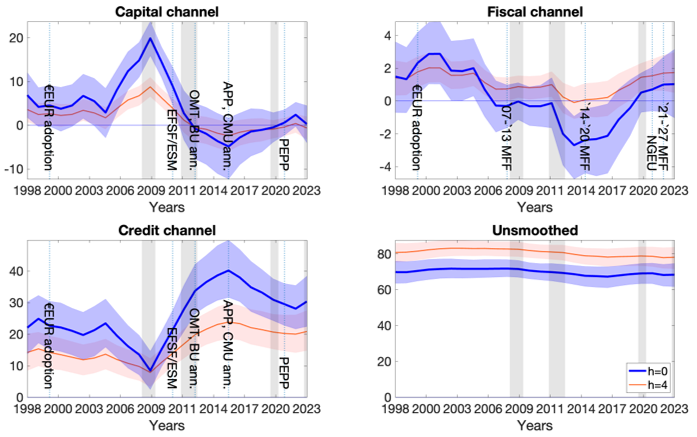

We document that the overall level of risk-sharing in the EA is much lower. Only around 30% of an output shock is smoothed, with a slight increase towards the end of our sample. The most striking finding is that the capital and credit channels move in opposite directions: the capital channel was dominant until the GFC. After that, it collapsed, probably due to financial market fragmentation and flight-to-safety occurring during the Crisis. On the contrary, the credit channel significantly increased during the GFC and the subsequent European Sovereign Debt Crisis (ESDC), probably also on the back of ESM-IMF financial assistance programmes implemented for countries under financial stress. The role of international fiscal transfers is negligible, but shows a slight improvement after the ESDC, and in particular during the 2020-2022 Covid-19 crisis.

Figure 1: Impulse responses to a state-specific output shock in the US

Notes: Blue line: impact effect. Red line: cumulative effect four years after the shock. The effects of the shock are normalized to one hundred in each horizon. Shaded areas are the 16th and 84th percentile posterior bands around the median. Vertical shaded (grey) areas indicate NBER recessions, vertical dotted lines indicate the dates of the presidential elections, the start of the FED tapering, and the Riegle–Neal Interstate Banking and Branching Efficiency Act.

Figure 2: Impulse responses to a country-specific output shock in the EA

Notes: Blue line: impact effect. Red line: cumulative effect four years after the shock. The effects of the shock are normalized to one hundred in each horizon. Shaded areas are the 16th and 84th percentile posterior bands around the median. Vertical shaded (grey) areas indicate recessions. Dotted lines indicate the dates of the activation of the EFSF/ESM support programs, the APP and PSPP of the ECB, the NGEU program and the years of the EU multi-annual financial framework (MFF) budget.

We then assess the interactions between the three channels, by looking at the correlations between their time-varying impulse responses to idiosyncratic output shocks. We find strong evidence for substitution between the capital and the credit channels. This result is evident in both regions, although it is statistically significant only for the US. Interestingly, we find that in the US the fiscal and the private (e.g. capital and credit) channels have reinforced each other. This result tends to support the hypothesis of Fahri and Werning (2017) who suggested potential complementarity between public and private risk-sharing channels.

Finally, for the US, we attempt to explain the time variation in the responses of the risk-sharing channels to output shocks with some macroeconomic and financial determinants, motivated by the existing literature. We proceed in two steps. First, we collect the median time-varying impulse responses of the three risk-sharing channels. Second, we regress the impulse responses on some potential explanatory variables, based a system of seemingly unrelated regressions (SUR), estimated with Bayesian methods. We focus only on the US because this allows us to exploit 45 years of observations, whereas, for the EA, we have only two decades, which limits the feasibility of such an analysis.

Our results suggest that the federal tax/transfer system and the capital channel provide more smoothing during weak economic conditions. In addition, we find that stronger financial integration leads to better functioning fiscal and credit channels. We also show that a higher government debt-to-GDP ratio is associated with a weaker fiscal and credit channel.

Our results have important implications for the improvement of the EMU’s governance framework. We show that there is substantial room to strengthen the shock-absorption capacity of the EMU. The Capital Market Union and the Credit Market Union could reinforce risk-sharing and enhance the resilience of the EA to macroeconomic shocks by contributing to smooth output shocks through the capital and the credit channel. However, policymakers should be mindful of substitution effects between these two channels. The US experience also points to positive externalities between the fiscal channel and the private risk-sharing channels. When translating this finding for the EA, this suggests that progress on the Fiscal Union could also have a beneficial effect on private risk-sharing mechanisms in the EMU.

Cimadomo, J., Giuliodori, M., Lengyel, A., and H. Mumtaz (2023). “Changing patterns of risk-sharing channels in the United States and the euro area” ECB Working Paper Series 2849.

Farhi, E. and I. Werning (2017). “Fiscal Unions” American Economic Review, 107 (12): 3788-3834.