This paper should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

In the Basel III framework, capital buffers are supposed to help banks to absorb losses in times of stress while maintaining the provision of credit to the real economy. This policy brief analyses bank lending behavior during the pandemic to gain insights into banks’ propensity to use capital buffers as intended by the framework. By exploiting euro area credit register data, we isolate credit supply effects and find that little headroom above regulatory capital buffers induced banks to reduce their lending supply during the pandemic compared to other banks, indicating an attempt to avoid dipping into regulatory buffers. Firms’ inability to reallocate their credit needs to less constrained banks had real economic effects as their headcount went down, although state credit guarantee schemes acted as partial mitigants. These findings raise concerns that the capital buffers introduced by Basel III may not be as countercyclical as intended.

A core goal of the Basel III capital buffer framework is to reduce amplification effects of the banking system on the economic cycle. The framework envisages that bank capital is built up during boom periods when risks accumulate. Capital is then employed when risks materialize during downturns and crises to absorb losses and meet credit demand, thereby supporting output and employment. Regulatory capital buffers sit on top of minimum capital requirements and constitute the combined buffer requirement (CBR) (BCBS (2019)2).3 While banks should meet minimum capital requirements on an ongoing basis, they should meet the CBR in normal times, but are allowed to draw on it in crisis time, provided they meet some restrictions on their capital distribution (dividends, share buybacks and bonuses). As such, the CBR fits the main purpose of the Basel III capital buffer framework by making banks entering a crisis with large capital ratio but making this capital usable during the crisis. Nevertheless, some concerns have been raised about whether some factors could impair the functioning of the framework. Specifically, banks may be unwilling to dip into the CBR due to limitations to distributions that are triggered when capital ratios fall within the CBR and market stigma associated with the consumption of capital ratios (Abad and Garcia Pascual (2022)).4

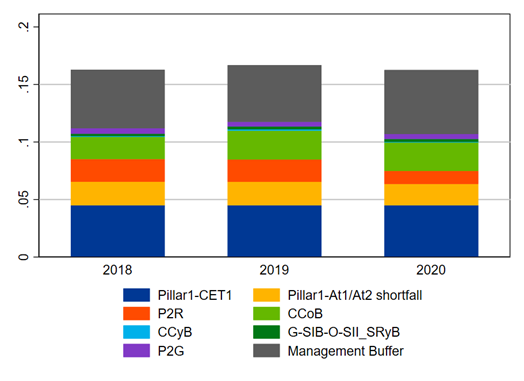

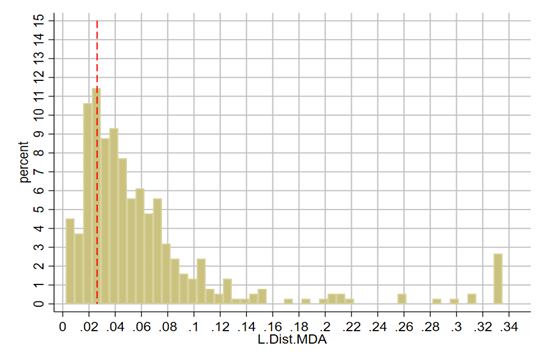

The COVID-19 pandemic constitutes the first opportunity to test the effectiveness of the CBR framework during a major systemic crisis. Restrictions on personal mobility and nonessential business operations strongly affected business revenues, causing a surge in firms’ liquidity needs. At the same time, those containment measures caused a major global economic contraction. As such, banks faced simultaneously a surge in credit demand and the prospect of serious deterioration in asset quality and profitability; a typical case calling for the use of the regulatory buffers. From an aggregate perspective, the euro area banking sector was able to meet credit demand and withstand stress, thanks to banks entering the Covid-19 pandemic with on average strong capital ratios (Figure 1), which were further supported by extraordinary policy measures throughout the pandemic. However, this favorable outcome reflects general equilibrium effects on credit, including the impact of support policies, and does not say much about the functioning of the Basel III capital buffer framework and banks’ propensity to use capital buffers. In our paper (Couaillier et al., 2022), we take a micro perspective and exploit the heterogeneity in banks’ pre-pandemic extra capital above the CBR to investigate whether banks closer to the CBR reduced corporate lending, compared to other banks, to avoid dipping into their buffers. We perform difference-in-differences analysis on a sample of 376 euro area banks which allows explicit testing on whether the lending behaviour of a selected group of banks, those closer to the CBR, differed significantly from that of banks with larger headroom above the CBR. Specifically, we define as “close to the CBR” those banks that have a pre-pandemic distance to CBR equal or below the first quartile of the distance to CBR distribution (approximately 2.6 percentage points) and we use as control group those banks with a larger distance to CBR (Figure 2). We use euro area credit register to get credit volume data at bank-firm level and thus to control for credit demand by comparing the credit received by the same firm from banks close and far from their CBR. We also control for a vast range of other policies put in place to support credit during the COVID-19 pandemic, in particular monetary and fiscal measures.

Figure 1. Evolution of bank common equity tier1 capital ratios and their components

Figure 2. Distribution of the distance to combined buffer requirement (CBR)

Our main finding is that proximity to the CBR puts downward pressure on corporate lending. Specifically, we find that, ceteris paribus, proximity to the CBR reduces lending by about 3.5% to non-financial corporations during the pandemic. We also find that banks with smaller capital headroom on top of regulatory capital buffers were more likely to grant loans pledged by government guarantees to economize on risk weights and loss provisioning and, consequently, to avoid approaching the CBR. We show that undrawn credit line balances prior to the pandemic exacerbated the downward pressure on new lending. Large credit line drawdowns that occurred during the pandemic pushed banks closer to the CBR to further cut lending supply to corporates to maintain the distance to capital buffer requirements. Additionally, we document that lower lending from banks closer to the CBR resulted in credit constraints for firms exposed to these banks as lost loans were not fully replaced. Specifically, firms that prior to the pandemic received a large part of their borrowing from banks in proximity to the CBR experienced about 2.5% lower borrowing during the pandemic in comparison to firms that borrowed mostly from other banks. This led those firms to cut down their headcounts by close to 1% in comparison to other firms. Finally, we show that government guarantees ameliorated the negative effect caused by closeness to the CBR. Firms receiving loans covered by government schemes countered off the lending impairments caused by banks closer to the CBR. Our results are in line with recent studies investigating possible impediments to buffer use.

We find robust evidence that banks proximity to the CBR results in lower lending supply during the Covid-19 pandemic. As such, while the CBR was successful in raising banks’ capital in good times, thereby improving solvency, it is less successful in its objective to support the credit supply in crisis time. The negative effect of proximity to the CBR on lending suggests that banks may be unwilling to accept restrictions on their distribution of capital as this have stigma effects. Overall, this suggests that further adjustments to the Basel III framework could help to make it more countercyclical. On the positive side, credit guarantee schemes proved useful to support credit supply of banks close to their CBR.

Abad, J., Garcia Pascual, A. (2022). Usability of bank capital buffers: The role of market expectations. IMF Working Paper, No WP/22/21, International Monetary Fund.

BCBS (2019). The Basel Framework, Bank for International Settlements.

Couaillier, C., Lo Duca, M., Reghezza, A., Rodriguez d’Acri, C. (2022). Caution: Do not cross! Capital buffers and lending in COVID-19 times. ECB Working Paper No 2022/20644, European Central Bank.

In the European framework, the CBR consists of the capital conservation buffer, the counter cyclica buffer, the systemic risk buffer and the buffer for systemically important banks.

For an explanation of the factors, see the article entitled “Macroprudential capital buffers – objectives and usability”, Macroprudential Bulletin, No 11, ECB, October 2020.