References

Aghion, P., D. Hémous, and E. Kharroubi (2014): “Cyclical fiscal policy, credit constraints, and industry growth,” Journal of Monetary Economics 62, 41-58.

Chen, S., D. Igan, N. Pierri, and A.F. Presbitero (2020): “Tracking the Economic Impact of COVID-19 and Mitigation Policies in Europe and the United States,” CEPR Covid Economics 36.

Gagnon, J.E. and C.G. Collins (2019) : « Are Central Banks Out of Ammunition to Fight a Recession? Not Quite,” Peterson Institute for International Economics Policy Brief 19–18.

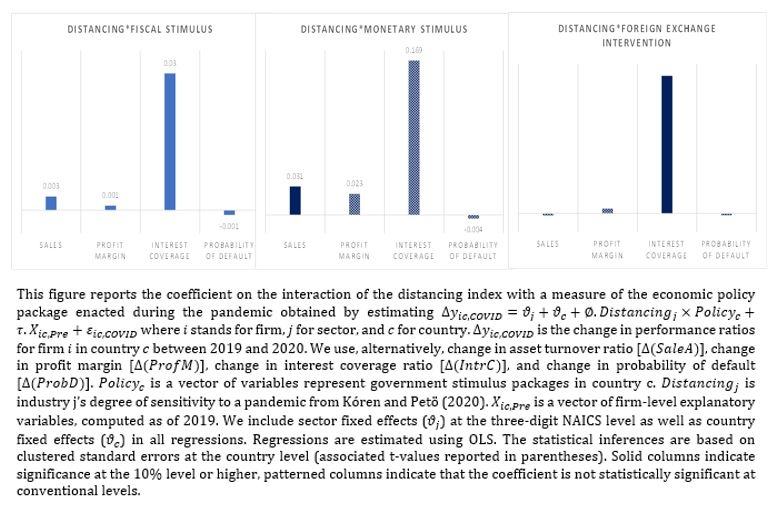

Igan, D., A. Mirzaei, and T. Moore (2022): “A shot in the arm: stimulus packages and firm performance during COVID-19,” BIS Working Paper No. 1014.

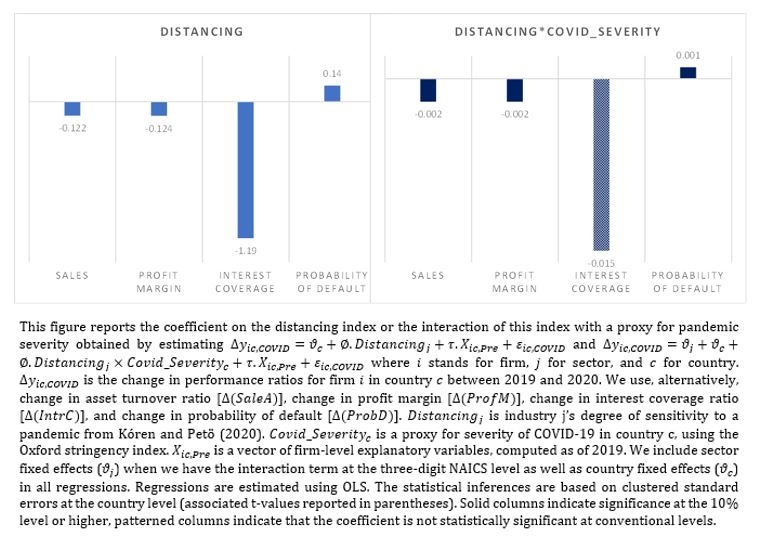

Kóren, M. and R. Petö (2020): “Business disruptions from social distancing,” PLoS ONE 15(9): e0239113.

Laeven, L. and F. Valencia (2013): “The real effects of financial sector interventions during crises,” Journal of Money, Credit and Banking 45 (1), 147–177.

Makin, A.J. and A. Layton (2021): “The global fiscal response to COVID-19: risks and repercussions,” Economic Analysis and Policy 69, 340-349.

Mankiw, G. (2020): “A Proposal for Social Insurance During the Pandemic,” blog.

Marron, D. (2020): “If We Give Everybody Cash To Boost The Coronavirus Economy, Let’s Tax It,” Tax Policy Center blog.

OECD (2020a): “Supporting people and companies to deal with the COVID-19 virus: Options for an immediate employment and social-policy response,” ELS Policy Brief on the Policy Response to the Covid-19 Crisis.

OECD (2020b): “Tax and fiscal policy in response to the coronavirus crisis: Strengthening confidence and resilience,” ELS Policy Brief on the Policy Response to the Covid-19 Crisis.