Recent stress in the U.S. banking sector raises the question of whether something similar or worse could happen in the Euro area. Key channels of stress include the vulnerability of banks to deposit runs, unrealised mark-to-market losses on portfolios of debt securities, exposure to CRE, and more general credit risks developing. Unlike the US, the Euro area does not have a complete banking union, including a unified deposit insurance system. And deposit insurance is capped at €100000, less than half the level in the US ($250000). While the ECB is now the dominant banking supervisory authority in the Euro area through the Single Supervisory mechanism (SSM), a common backstop provided by the European Stability Mechanism (ESM) to the main crisis resolution tool – the Single Resolution Fund (SRF)– is still awaiting ratification as the Italian government has yet to agree to the ESM reform package.

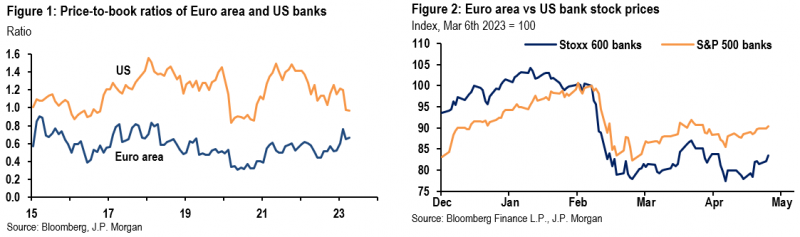

At first blush, these institutional features make the Euro area appear potentially more vulnerable to banking stress than the US, especially when combined with the general lower profitability of euro area banks. Indeed, although profitability has gone up in recent quarters given the exit from negative interest rates and increasing net interest margins (NIM), the price/book ratio of euro area banks has been consistently below those of the US (Figure 1). Moreover, stock prices for the EU-wide banking sector (which does not include Switzerland) have fallen ever more sharply than a similar index for US banks since early March (Figure 2).

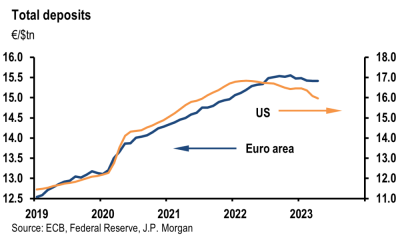

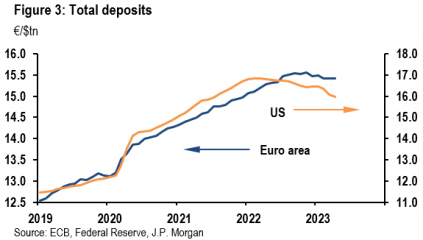

Despite all this, with the exception of Credit Suisse, the European banking system has been largely insulated from contagion from funding stress in the US regional banking sector. Most notably, there are no signs of deposit fragility so far, whereas deposits in the US banking system have been on a steady slide since early 2022, which obviously intensified in March (Figure 3).

Overall, the Euro area banking system has weathered the recent shocks well so far. Euro area banks may be less profitable than their US counterparts, but they score better on several measures of solvency, liquidity and funding stability. Some key concerns about the US regional banks also do not seem to be as pervasive or elevated in the Euro area. Euro area Less Systemic Institutions (LSIs) are extremely small and seem to be largely engaged in traditional lending, with arguably less concentration in potentially risky sectors such as commercial real estate (CRE). Crucially, the regulatory loopholes that led to insufficient oversight of large banks such as Silicon Valley Bank (SVB) and First Republic Bank (FRB) do not appear present in the Euro area, where liquidity and mark-to-market rules apply to all banks without exceptions.´

There are good reasons to expect euro area bank resilience to continue. Some reflect the more traditional structure of the Euro area banking business, including a small perimeter of generally small local banks that appear too marginal to raise systemic considerations. Others are related to policy actions, given that the Euro area makes up for its incomplete banking union with stringent regulation and intrusive system-wide supervision. Under our baseline, the Euro area is set to experience moderate growth (around 1% on average for 2023-2024) and private sector balance sheets should remain healthy. These conditions suggest that while there may be pockets of banking stress, a manifestation of systemic risk is unlikely.

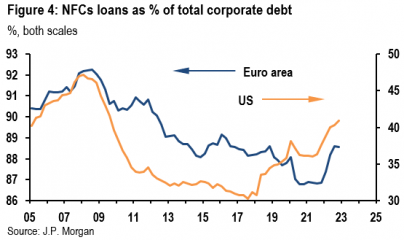

Still, banks do play a more central role in credit provision in the euro area than in the US (Figure 4). While capital market financing has increased in the euro area over the last 15 years, bank loans still make up nearly 90% of total corporate debt. In the US, by comparison, the share of banks loans is only around 40 percent. Hence a slowdown in bank lending would be more consequential for the macroeconomic outlook in the euro area, which is a concern given the recent loan growth data and tightening of bank lending standards. Moreover, a significant downturn, coupled with a high for long rate environment in the face of very sticky inflation, would definitely generate genuine pressure on banks’ balance sheets via a material impairment in asset quality. Combined with potentially tighter regulatory requirements, this could raise the risk of a credit crunch.

To be sure, there is no room for complacency given bank runs and liquidity flight can happen abruptly. Intrusive supervision is here to stay and liquidity regulation may need to be tightened further given deposits can fly more easily in an era of digital banking and social media. The latter will undoubtedly be a focal point of the ECB’s annual review of banking risks. Finally, making further progress on banking union and ratifying the ESM treaty reform would increase resilience of the euro area banking system and reduce associated risks. That could be especially important if financial conditions remain tight for a sustained period of time and credit risks materially build.

The EU banking system has been through a major regulatory upheaval since the GFC and the sovereign crisis of 2010-12. In addition, Southern Europe saw a sweeping restructuring in the sector, which dramatically improved the solvency and the resilience of the formerly weaker part of the banking system. There were two main drivers: (i) market forces and (ii) the ECB push to sever the sovereign-bank doom loop.

The Euro area, as the whole EU, implements the Basel standards consistently across several thousand banks of all sizes. Meanwhile, the US has implemented a dual approach since 2018, with Basel rules applying in full only to a subset of 13 large systemically important banks and lighter requirements for the others. The European Banking Association (EBA) also conducts and publishes regular (every 2 years) stress tests to measure the loss absorbing capacity of the large banks under downside scenarios. Stress test scenarios for 2023 focus on a sharp rise in short-term and long-term interest rates. European banks are required to perform regular supervisory tests under Pillar 2 requirements to measure the impact of interest rate changes on their interest income and value of equity.

Furthermore, since the onset of the GFC, the ECB has taken on a proactive refinancing role for the banking system, with a plethora of facilities for banks to tap. As a result of all these factors, most measures of banking soundness have improved dramatically over the last decade (see below).

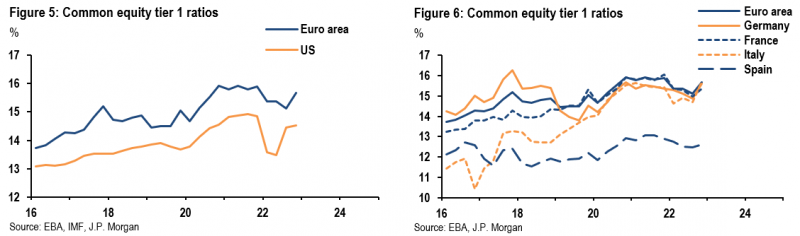

Solvency measures for banks across both sides of the Atlantic have increased sharply since the GFC. CET1 ratios in the Euro area hover around 15-16%, about 1%-pt above the US (Figures 5 and 6), although CET1 requirements for G-SIBS are actually slightly larger in the US than for their European counterparts. The current elevated levels of CET1 in the Euro area contrast with ratios below 10% in 2009, and the current composition is actually of higher quality and loss absorbing capacity compared to 15 years ago. Looking into the largest economies of the region, only Spain remains somewhat below the regional average.

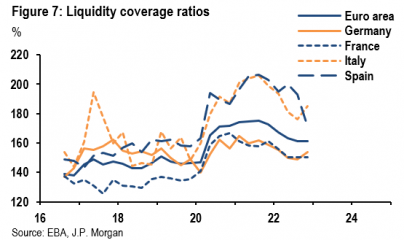

The ability to withstand liquidity shocks is better measured by the short-term liquidity coverage ratio (LCR). The LCR imposes a minimum requirement on the amount of unencumbered high-quality liquid assets (HQLA) available to withstand a 30-day liquidity stress scenario.

The aggregate LCR in the Euro area in 1Q23 stood above 160% (Figure 7), well above the level in the US (115%). The LCR is considerably higher in Italy and Spain (around 180% on average) than in Germany and France around 150%). The US figures are, however, distorted by the management of excess liquidity in the system through the repo policy, which constrained the growth of the numerator.

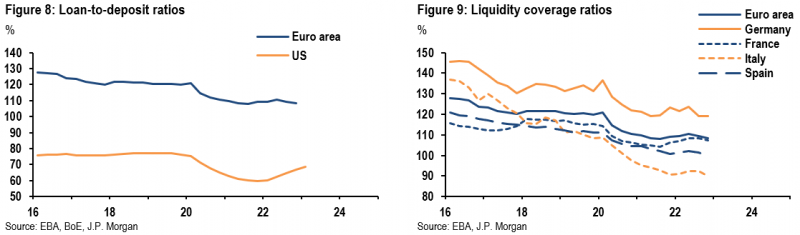

The loan-to-deposit ratio (LTD) has also fallen sharply in the Euro area to slightly above 100%, down from levels close to 140% in 2014. There is significant heterogeneity across countries, with Germany higher, close to 120%, and Italy lower, close to 90%, with France and Spain in between. The LTD is much lower in the US (around 60%) but that arguably reflects the structurally limited exposure of US banks to the mortgage business outside of origination given the presence of the GSEs. The LTD in the US has risen significantly in the last few quarters as a result of a contraction in deposits (Figures 8 and 9).

In the past, LTD levels well above 100% reflected a large dependence on volatile wholesale funding. The sudden dry-up of that source of funding amidst the freezing of the interbank market during the GFC was one of the key factors that produced the credit crunch during the GFC. An LTD near 100% would normally imply that there is little excess liquidity in the banking system, but Euro area banks also have above €4.1 trillion of excess reserves stored at the ECB, compared to total private non-financial sector deposits around €15.5 trillion. Hence, in an era of expanded central bank balance sheets, the LTD ratio provides less of a signal of funding risk. The latter is instead better gauged by liquidity ratios, which are very elevated in the region.

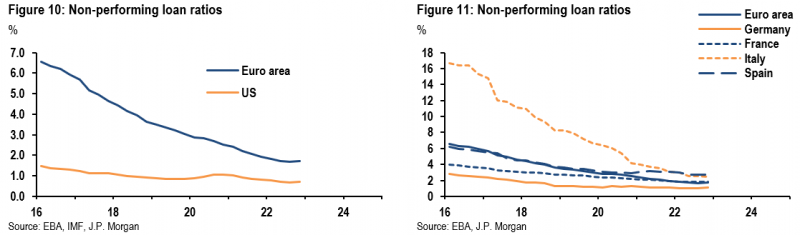

A crucial measure of the improved soundness of the Euro area banking system is the sustained decline in NPLs, which have recently declined to cyclical lows of below 2% (Figures 10 and 11), down from above 10% during 2012-14. The downward trend has been dramatic in Italy, where the NPL ratio has now fallen near to 2%, compared to a peak of around 18% in the aftermath of the 2011-12 recession. The Italian decline also reflects the development of deeper NPL secondary markets, including for NPL securitizations.

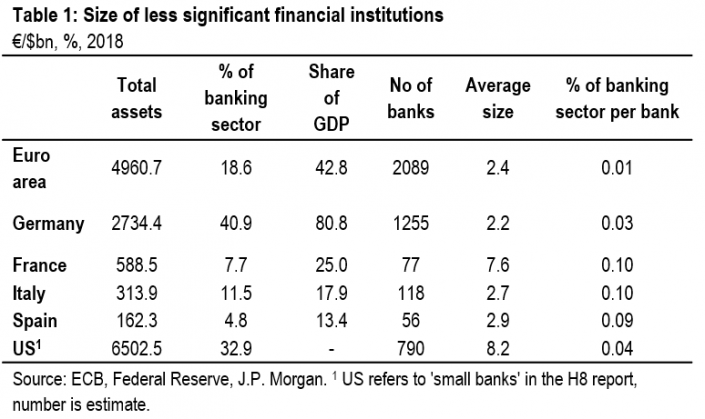

The ECB directly supervises 110 significant banks incorporated in the Euro area countries participating in the SSM. Typically a bank is classified as significant if the total value of its assets exceeds €30 billion or it is one of the three largest banks in a given country. These banks hold an overwhelming majority (82%) of banking assets in these countries. The banks outside the ECB/SSM perimeter are called Less Systemic Institutions (LSIs) and are subject to primary supervision from the national competent authorities.

The size of the LSI sector varies considerably across countries, but it is generally quite small. The aggregate figure is skewed higher by Germany, which has seen less of a merger wave in the last 15 years and looks like an outlier with a 41% share (Table 1). There are some lower requirements for these banks that might, on the surface, suggest some similarity with the situation of the regional banks in the US. However, a more in-depth look suggests that the LSI sector plays a marginal role in the Euro area, with only modest, if any, implications for

financial stability.

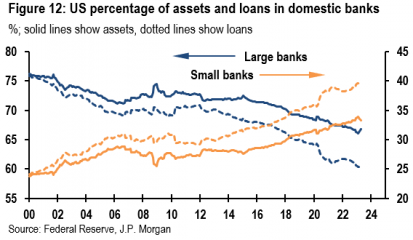

As a start, the less regulated small banking sector at the epicenter of the current banking stress in the US accounts for a much larger share (33%) of the banking system compared to the Euro area (Figure 12). Actually, this figure underestimates the role of regional banks because it does not include the larger regional banks like SVB and FRB.

In 2019, the US bank regulators, following an Act of Congress, ruled that most banks with assets between $50 and $250 billion would no longer be subject to the LCR or other enhanced prudential standards that apply only to the most systemically important banks (GSIBs). Hence, the effective regulatory oversight of some large US regional banks was significantly lowered, as it has become apparent in recent months. Indeed, both Silicon Valley Bank (SVB) and First Republic Bank (FRB), now defunct, held more than $200 billion in total assets, which put them in the top 20 list of the largest US banks. This grey area in the regulatory and supervisory perimeter seems specific to the US, with no similar carve out in the Euro area. And the Federal Reserve seems intent on fixing it, as they underscored when announcing the results from their review of the supervision and regulation of SVB.

Euro area LSIs are numerous, are local business-oriented (rather than regional) and are extremely small. The average size of the LSIs is EUR 2.4 billion (Table 1), which is about ¼ that of the US small banks (even excluding SVB and FRB). The business model is traditional, based on deposit taking and collateralized lending to the real economy.

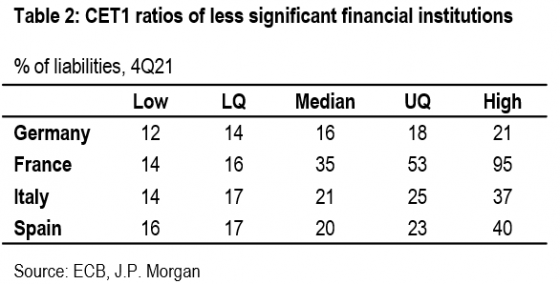

Data on solvency also show that LSIs generally have higher capital ratios than their large counterparts (Table 2). This is hardly a coincidence in our view. After a major wave of consolidation in the sector, small local banks likely needed to show strong solvency parameters to attract business. In the Euro area, LSIs have been exempted since inception from higher MREL (minimum requirements for own funds and eligible liabilities) because the size and profitability of the business are not consistent with the costs of market-based finance. This inability to access costly market finance may have induced the national supervisors to be more conservative on capital requirements for these banks as a group. Finally, all Euro area banks, including LSIs, are subject to the LCR regulation and mark-to-market of interest rate risk on debt securities in the available for sale (AFS) book.

Overall, a closer look at the key features of Euro area LSIs suggest that this sector has little potential for systemic spill-overs.

The apparent lack of systemic relevance of LSIs does not mean that they can be considered immune from a deposit run. Instead, our colleagues in Credit research have argued that whole Euro area banking sector is considerably less vulnerable to bank runs compared to the US for a series of reasons.

First, all retail depositors are better protected on the basis of the seniority waterfall in place in the Euro area compared to the US. In the Euro area, both types of retail deposits – insured (up to €100k) and uninsured (above €100k) – are senior liabilities. In the US, the ambiguity about the status of retail deposits above the insured threshold ($250k) appeared to be a key factor heightening the risk and extent of the bank run on SVB and other regional banks. Eventually, a systemic exception had to be invoked to ensure that all deposits were to be considered safe, but that came only after the fact. By contrast, corporate deposits rank together with non-deposit liabilities both in the Euro area and the US, even though in some Euro area countries such as Italy and Portugal, deposits of SMEs are also senior ( i.e., rank above senior secured debt).

Second, the EU introduced MREL to further enhance loss-absorbing capacity. In the EU, 115 banks need to meet MREL targets. In the US, only a handful of G-SIBs must comply with the international equivalent of MREL, Total Loss Absorbing Capacity (TLAC) targets, as well as additional surcharges for systemic relevance. As a result, on a system-wide basis, both solvency and liquidity requirements are actually higher in the Euro area compared to the US. Furthermore, according to a recent Banque de France paper, the average MREL binding requirements for EU G-SIBs are about 3.5%-pt higher than the average TLAC requirements for US banks, with the risk that the finalisation of Basel III may widen the gap further in the coming years.

This emphasis on MREL is mirrored in a broader EU recourse to Cocos – contingent convertible bonds that rank just above equity in the hierarchy – in order to build an extra buffer of loss absorbing capital that reduces the risk of losses being large enough to hit depositors. Importantly, authorities in the Euro area have been adamant in rejecting the possibility that the inversion by the Swiss authorities of the standard seniority between AT1 bonds and equity in the Credit Suisse case could ever apply in the region.

This said, the Euro area also has its blind spot, in the sense that a successful resolution strategy based on bail-in according to the BRRD rulebook requires adequate levels of MREL (up to 8%) to prevent losses being imposed on depositors and other retail creditors. However, several medium-sized banks do not respect those requirements, sometimes for the simple reason that they are not listed. This is one of the main reasons behind the European Commission’s proposal for a revised Crisis Management and Deposit insurance framework.

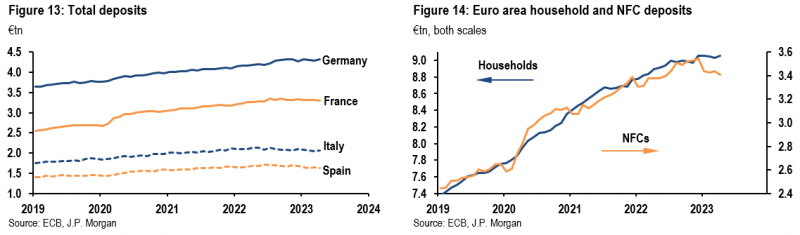

So far, the entire deposit base – both household and corporates – has been stickier in the Euro area than in the US. Deposit outflows in the Euro area have been modest up to now, and much lower than for the US (Figures 3 and 13). The relative stability of deposits in the Euro area also reflects different macro drivers. First, quantitative tightening is lagging versus the US and will likely proceed at a more measured pace in according to current ECB communication. Second, the build-up of excess savings (in nominal terms) in the region during the COVID period has led to a substantial increase in bank deposits. Faced with a persistent shock to the price level, households have only made modest recourse so far to the stock of excess savings. We expect that Euro area consumers will be reluctant to reduce their savings rate materially below historical norms also going forward and this should support the stability of deposits. By contrast, in the US, the savings rate has fallen sharply in recent quarters. Competition from other deposit-like instruments in the US (e.g., MMFs) has likely favoured migration of liquidity away from the banking sector at a time of rising interest rates, exacerbating the extent of the phenomenon.

While Euro area banks have been quite sluggish in adjusting deposit rates to the current level of policy rates, it is likely that this pressure may intensify as savers seek higher returns on their deposits. So far, the combination of higher rates and stronger nominal GDP growth has sharply boosted net interest income (NII), but an increasing deposit beta (correlation between deposit and policy rates) and modest loan growth point to some decline going forward. Furthermore, while household deposits have remained fairly stable through April, there are already declines in corporate deposits, although the latter account for less than 30% of total deposits (Figure 14). This is likely the result of a higher recourse to self-financing in the face of higher bank rates and tighter financing conditions, and is set to intensify over the coming months.

Our colleagues in Equity research have looked at the sensitivity of a set of large Euro area banks to interest rate risk on their portfolio of debt securities (including sovereign bonds). The IMF’s Spring 2023 Global Financial Stability Report (GFSR) also has some related analysis.

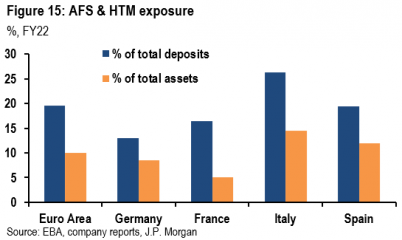

The bottom line is that vulnerabilities in the euro area appear less than in the US. The role of debt securities in the portfolio of large Euro area banks is significant (Figure 15), especially in Southern Europe, where banks have traditionally been buyers of government debt (even though on a secular downtrend due to a regulatory push towards diversification). But both our equity team analysis and that of the IMF show that this role is less significant than in the US.

For example, the GFSR illustrates that debt securities account for nearly 13% of the total assets for Euro area banks, less than half than for US banks (27%). Second, only in the US are mark-to-market valuation changes for AFS securities treated as unrealized gains and losses for all but the largest banks. Third, IMF estimates suggest that the impact on capital ratios of unrealized losses in held-to-maturity portfolios for the median bank in Europe would be less than 50bp, more than 5 times smaller than the equivalent impact in the US. Fourth, according to our Credit research colleagues, not only do Euro area banks have higher LCRs than their US counterparts, they also hold about ⅔ of HQLA in central banks reserves and cash. With an average LCR at 160%, this means that they could withstand a severe liquidity scenario without having to sell their sovereign bonds.

Another key feature in the Euro area is the collateral framework of the ECB, which allows Euro area banks to pledge portfolios of securities held at amortised cost to obtain secured funding without crystalizing any potential valuation loss. This is a key point, considering that eventually it was the funding pressure stemming from a deposit run that magnified the problem of unrealised losses on the portfolio of debt securities holding (including US treasuries) at the US regional banks. In fact, if deposits don’t come under pressure, there is no need to recognize mark-to-market losses even if the equity value is falling. And, if the central bank has standing funding facilities and an efficient collateral framework, the risk of a doom loop becomes smaller.

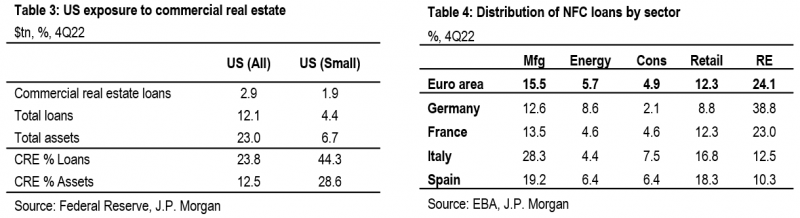

Concerns about exposure to commercial real estate (CRE) in the Euro area also seem less pervasive than in the US. US banks’ exposure to CRE is generally high, and is nearly twice as large for small banks (Table 3).

In the Euro area, aggregate data for the total banking system show that real estate is the single largest sector in terms of loans to corporates, although the figure is likely significantly biased upward given that the RE aggregate includes loans to other companies that are collateralised by real estate. Country level data show that Germany is significantly more exposed to CRE (Table 4). Loans to the Real estate & Construction sectors account for 40% of the NFC loan book in Germany, well above France (27.6%), Italy (20%) and Spain (16.7%).

More importantly, small US banks have a disproportionate exposure to CRE compared to US large banks, and this funding gap is unlikely to be adequately filled as small banks reduce the provision of loans. Comparable data for the Euro area LSIs is not available. As a ballparking exercise, we start by noting that loans to NFCs account for 22% of LSI assets. If the LSIs loan book had a same sectoral breakdown as for the total banking system (29% of the loan book allocated to both Real estate & Construction), the average exposure to CRE would be 6.5% of total assets, thus roughly ½ of the US banks and 1/4 of the US small banks. Even if the concentration were twice as much as the total banking sector (58% – a value that looks implausibly high), then LSI exposure to the sector would only account for 13% of their total assets, still well below the 28.6% of the US small banks.

Our colleagues in Equity research have looked at the exposure to CRE for a set of large listed banks, even though data availability is an issue due to incomplete reporting. Potential losses appear fairly manageable. For a set of large EU listed banks (i.e. including Scandinavian banks which are much more exposed), the average exposure to CRE is worth 7.3% of the total loan book and about 50% of the exposure is already provisioned for.

Our colleagues in Credit Research have also argued that there are fundamental reasons to be less concerned about CRE exposures in the Euro area. First, the Euro area CRE market is more regulated than in the US, a factor which historically has led to an undersupply of units and high occupancy rates. Second, there is much more widespread indexation to inflation in the Euro area, which is set to bolster CRE yields. Third, the Euro area overall seems less vulnerable to valuation shocks because work from home seems to have had a lower impact than in the US. In particular, US CRE is affected by significant tech layoffs, which has been a key driver of demand for CRE in last few years. This is much less of an issue in the Euro area given the much smaller size of the sector.

Finally, as discussed, there is no comparable role for LSIs in the CRE sector in the Euro area, possibly with the exception of Germany. As a result, the sector is unlikely to see a sudden stop in credit; in fact, banks in Europe continue to fund CRE companies and therefore should avoid any crystallisation of valuation losses. By contrast, US large banks may not be able to make up for the reduced credit from regional lenders. If the former transpired, US CRE companies would have to unwind real estate portfolios, which would likely exacerbate the pricing pressures.

Of course, one should not underplay more general concerns about CRE exposures. It is a sector that is highly sensitive to the economic cycle. And valuations and transactions have already taken a significant hit, with potentially more to come. As the ECB notes in its May 2023 financial stability report, further adjustment in CRE markets could expose vulnerabilities in some open-ended property funds. Overall, however, banking sector-related risks seem less acute than in the US.

Disclaimer: This SUERF policy note includes research content published by J.P. Morgan on 7 June 2023. J.P. Morgan has granted SUERF a limited right to re-publish this research on an information only basis. J.P. Morgan has no liability in any regard for the publication of this SUERF policy note or SUERF’s decision to reproduce any J.P. Morgan research content contained herein. It is not an offer to buy or sell any security/instruments or to participate in a trading strategy or trading activity; nor does it constitute any form of personal financial advice or investment recommendation by J.P. Morgan. This information should not be relied upon for any reason whatsoever by any natural or legal person.

For important current standard disclosures that pertain to J.P. Morgan’s research please refer to J.P. Morgan’s disclosure website: https://www.jpmm.com/research/disclosures.