All of you here today know Ken Whitaker. Central banker and civil servant extraordinaire, he is held up as a champion of economic reform – the man credited with laying the groundwork for Ireland’s transformation into the Celtic Tiger.2 But you might not know that his reforming zeal was felt outside Ireland as well, even in Basel. Dr Whitaker was a frequent visitor to the Bank for International Settlements (BIS) during his term as Governor between 1969 and 1976, as you can see from the “class photos”.3

The BIS archives contain an interesting exchange of letters between Dr Whitaker and the then BIS Chairman. Dr Whitaker and the Governors of the Austrian, Danish and Norwegian central banks petitioned the BIS to expand its Board of Directors to include a wider range of shareholding countries. I’m afraid the BIS was not very receptive at the time: it saw any expansion as a slippery slope. It took several decades for membership of the BIS and of its Board to become, in stages, truly global.4 Dr Whitaker was, as ever, ahead of his time. And I was pleased to see that he still found value in the BIS’s role as a hub for central banks – bringing together policymakers from all over the world to exchange experiences and discuss common challenges.5

Last year, my colleague Mark Carney gave a lecture here on the future of work. In a similar vein, I will also look to the future – not of work, but of money; and, more broadly, the monetary system. Part of the BIS’s mandate is to serve central banks in their pursuit of monetary stability and to foster international cooperation in this area. Hence it is no surprise that we, like our shareholding central banks, have a keen interest in this subject. Money and payment systems together make up the monetary system,6 and should be seen as two parts of the same whole.

Throughout history, technological innovations have continually reshaped the monetary system, either by changing the nature of money or the workings of the payment system. These times are no different. The hype around bitcoin and its cousins has died down somewhat. But innovation continues. What seems new this time is the sheer volume of innovations and the fact that both components of the monetary system are targeted at the same time. Historically, changes to payment systems have been infrequent. Changes to the nature of money have been even rarer. But now, attempts to create new forms of money or to engineer new ways to pay appear almost weekly.

This afternoon, I will share some thoughts on how technological innovation may affect the monetary system. I am particularly interested in the implications for central bank money and what so-called central bank digital currencies (CBDCs) would mean – not just for the system, but for all of us as citizens.

The important part of the acronym CBDC is not the “D” for “digital”. Nowadays, nearly everyone has access to digital payments. Whenever you or I pay using a bank debit card or use a banking app on our mobile phone, the payment is made digitally and often instantly.

Instead, the important part of CBDC is the “CB” for “central bank”. A CBDC would allow ordinary people and businesses to make payments electronically using money issued by the central bank. Or they could deposit money directly in the central bank, and use debit cards issued by the central bank itself. So, what are the consequences of such a system? How would it differ from what we have now?

James Joyce once said: “a man of genius makes no mistakes; his errors are volitional and are the portals of discovery.” This is an inspirational guide for artists and writers; the cost of getting it wrong is just brief personal disappointment. But the upside is huge, and a masterpiece could follow. This gung-ho attitude is common in the fintech industry. “Just do it!” is the mantra. To them, worrying about the consequences of mistakes is for wimps.

But central bankers do not think of themselves as geniuses, and prefer to tread cautiously into new territory. There is a good reason for this. The monetary system is the backbone of the financial system. Before we open up the patient for major surgery, we need to understand the full consequences of what we’re doing. As my colleague Yves Mersch said recently, we understand the repercussions for the people we serve. And we recognise that adopting untried technology that ultimately proves unreliable could seriously endanger public trust in the currency and in the central bank.7

Therefore, grappling with the potential of CBDCs is one of the challenges common to today’s policymakers, and certainly for tomorrow’s as well. Having a digital currency issued by the central bank may not seem like a radical change to many of those used to shopping and paying bills online. But it turns out that such a move is more consequential than appears at first sight. I will take you through some of my thinking on the subject.

Let’s look back at how the monetary system evolved, taking money first. Throughout history, a wide range of items served as money, including stones, shells and cigarettes. In Ireland, coins – first imported by the Vikings – have been used for more than 1,000 years.8 In its 76 years, the Central Bank of Ireland has presided over three different currencies: the pre-decimal Irish pound with its 240 pennies to the pound, the decimal Irish pound, and the euro.9

At its simplest, in economic terms, money is what money does.10 And what money does – in whatever form it takes – is to serve as a unit of account, a means of payment, and a store of value. A common measure of economic value, or a unit of account, makes our lives easier. Imagine how difficult it would be to compare the price of a pint of stout and a glass of whiskey without money. Go into a pub near here and the barkeeper might tell you a Guinness costs 6 euros and a Jameson Gold costs 12 euros. One is clearly dearer than the other. But what if the barter system were still in place? A Guinness might cost 25 apples and a whiskey 30 oranges. The relative value becomes unclear. Today, the common measure is usually “the currency”. If there are multiple units of accounts, one tends to prevail over time. As you may recall, shops in Ireland initially listed prices in both euros and Irish pounds. Still, two decades later, not many outside this building remember the official conversion rate of IEP 0.787564 to the euro.

The second attribute of money is to serve as a means of payment. I could pay for my pint with cash, with a credit or debit card and, increasingly, even with my mobile phone. But, as I mentioned earlier, there is an important distinction between the types of money being transferred. Cash is public money, issued by the central bank. The others represent private money. That is, liabilities of either a commercial bank, the phone company, or a big tech firm.

Last but not least, money must be a reliable store of value. This is a lesson I learned the hard way as a child. When I was eight years old, inflation was high in Mexico. I remember my father giving me a wad of cash for the school bus. At the end of the day, when I tried to take the bus home, the fare had gone up. I ended up walking all the way home. Such experiences taught me the dangers of monetary instability and its inverse, the value of price stability.

The other half of the monetary system is payment systems, which also come in many shapes and sizes. Some are operated by the public sector. Others by the private sector. They might even compete. Unlike money, payment systems are not always interchangeable. Systems tend to process certain forms of payments. For example, retail systems typically handle large volumes of relatively low-value payments in such forms as cheques, credit transfers, direct debits and card payments. In contrast, wholesale systems handle large-value and high-priority payments like interbank transfers.

Two worldwide trends have been driving change in payment system design for quite some time. One is speed. The other is globalisation.

The quest for speedier payments is long-standing.11 A delay of a day or more in payment used to be acceptable; today, it seems like an eternity. On the retail side, consumers accustomed to instant communication via email and social media expect to be able to make instant payments. Accordingly, faster systems for retail payments (“fast payments”) have recently emerged. They generally allow the public to receive funds within seconds, anytime and anywhere. On the wholesale side, so-called real-time gross settlement (RTGS) systems have been speeding up payments for much longer – since the 1980s, in fact. They are now the standard around the world.12

Globalisation is increasing the demand for cross-border payments.13 Most of these flows still rely on an intricate web of bilateral relationships between commercial banks, known as correspondent banking.14 But multicurrency systems are emerging. They provide settlement of more than one currency within one jurisdiction or across multiple jurisdictions. One example is the Eurosystem’s new TARGET Instant Payment Settlement service, or TIPS.15 The system allows retail payment service providers to offer funds transfers in real time around the clock. It can also handle multiple currencies.16

Both money and payment systems are essential to the functioning of a modern economy. Both rely on trust. You accept money as payment because you trust that you can pass it on to someone else later. That trust may be shaken – by currency devaluations, hyperinflation, wide-scale payment system disruptions or bank defaults.17 Maintaining trust in the monetary system is a first-order public interest. In most countries, the central bank is the institution charged with this task.

A thought experiment: what would a future monetary system with CBDCs look like? Let me make an important point at the outset. The CBDC debate is not primarily about convenience and digitalisation. Cashless systems are being developed very rapidly. Many of you are or will be using one or more of those systems through your mobile phones. Indeed, this is the cutting edge of innovation. Many fintech companies are testing cashless systems. In China, for example, fast food can already be bought via “smile to pay” technology using facial recognition software.

So, to be clear, the CBDC debate is not about the technology or its look-and-feel to the customers making payments. Then, what is it about?

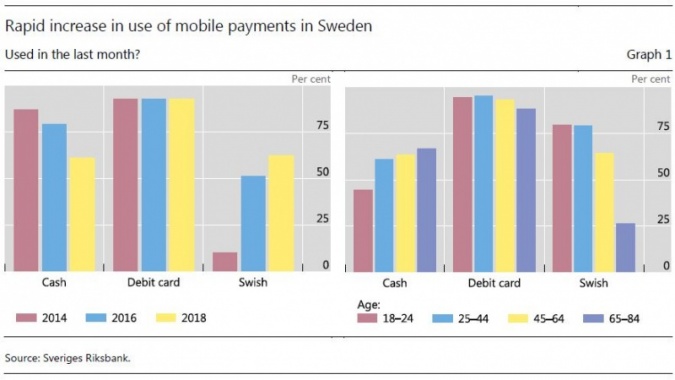

It’s partly about the potential decline in the use of cash, and what central banks should do about it. In a number of countries, the demand for cash has fallen substantially as consumers and retailers have embraced electronic means. Two examples are Sweden and Denmark, where stores and restaurants are increasingly reluctant to accept paper money. Instant mobile payment solutions are gaining ground rapidly. The latest data from Sweden show that mobile payments are being used as often as cash to make payments. Young people use their mobiles to pay almost twice as frequently as they do with cash (Graph 1).

But for most countries, cash is still in high demand.18 The amount of cash in circulation has actually increased over the last decade in tandem with electronic payments. In the short term, there is no urgency to come up with a substitute for cash. Things may change in the future, however, and central banks want to be prepared.

A cash substitute is in any case only one potential form of CBDC. A report last year by two of the central bank committees based at the BIS identified two main CBDC varieties.19 A wholesale CBDC would be restricted to a limited group of users and used for interbank payments and other settlement transactions. A retail CBDC would be widely accessible to everyone. This could be based either on digital tokens or on accounts. That would mean that you and I could open bank accounts directly with the Central Bank of Ireland.

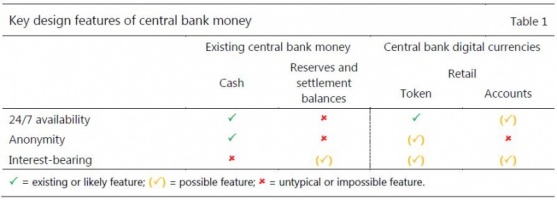

We can see how cash compares with a retail CBDC in the last two columns in Table 1. Like cash, a CBDC could and would be available 24/7, 365 days a year. At first glance, not much changes for someone, say, stopping off at the supermarket on the way home from work. He or she would no longer have the option of paying cash. All purchases would be electronic. But from here, differences start to emerge. A CBDC is not necessarily anonymous, like cash. And unlike cash, it could pay or charge interest.

In terms of technology, it would be easier to replicate the attributes of cash – if so desired – in a token-based version of CBDC than in an account-based one. But the digital token technology is still broadly untested, whereas the technology for an account-based CBDC has been available for decades. So far, central banks have generally chosen not to provide such accounts. Why not? The answer lies in one of the other major issues underlying the CBDC debate: the impact on the financial system.

The current system has two tiers. The customer-facing banking system is one tier, and the central bank is the other. The two tiers work together. You’re running a shop and, say, Joe buys something from you. When Joe pays you, his bank debits his account and credits your account. When your bank is different from Joe’s, the two banks settle the payment through the central bank. The central bank debits Joe’s bank’s account and credits your bank’s account, making sure the payment is “final”.

At the moment, these settlement accounts, shown in the second column of the table, are the only form of CBDC. Only commercial banks have access to them. The debate is whether to widen access to CBDC beyond the current circle of commercial banks.

Banks play an important role as provider of financial services to citizens and businesses. Imagine that the Central Bank of Ireland and the ECB were to offer deposit accounts to everyone and then issue debit cards and mobile phone apps for you to make payments with. In such a scenario, the central bank would be taking on the customer-facing business lines. Presumably, the central bank would need to recruit new staff to handle this line of business and to handle customer enquiries. Now, I can tell you that central bank staff are very good, and they would be capable of taking on customer-facing tasks. But that is not the main issue.

Safety could be an important reason to deposit money in the central bank. In times of uncertainty, more customers would prefer to have deposit accounts at central banks, and fewer at commercial banks. A shift of funds from commercial banks to the central bank could be gradual at first. But the trickle could turn into a flood.

If bank deposits shift to the central bank, lending would need to shift as well. So, in addition to the deposit business, the central bank would be taking on the lending business. The central bank would need to meet business owners, interview them about why they need a loan, and decide on how much each should receive.

We can ask ourselves whether this is the kind of financial system that we would like to have as the ultimate set-up. I grant that this thought experiment may have gone too far. For instance, the central bank could make do without a lending operation if it sends customer deposits to the commercial banks by opening central bank accounts at commercial banks. In effect, the central bank would be lending to the commercial banks so that they could lend on to the customers.

However, the bigger issue has to do with the division of labour between commercial banks and the central bank. The central bank is a public institution charged with ensuring that inflation is under control, the economy runs smoothly and the financial system is sound. Commercial banks are private businesses that thrive by attracting and serving customers. They need a different mindset, constantly innovating. They tend to have more staff than central banks because serving customers is resource-intensive. To be sure, supervision and regulation need to be in place so that commercial banks do not jeopardise the financial system through reckless behaviour.

There are historical instances of one-tier systems where the central bank did everything. In the socialist economies before the fall of the Berlin Wall, the central bank was also the commercial bank. But I do not think we can hold up that system as something that will serve customers better.

Less dramatically, publicly owned banks in many developing economies are hardly paragons of efficient allocation of funds or of good service. Although established with the best intentions, in practice they often verge on being highly bureaucratic institutions susceptible to political influence, in particular to directed lending to politically favoured sectors of the economy.

In any case, token-based CBDCs may be less prone to this type of structural shift from the commercial banking sector, as the outstanding amount of the CBDC can be fixed. However, there would then be the question of whether these tokens would start to command a premium over bank deposits. Would such a premium fluctuate over time with shifts in uncertainty and financial conditions? Offering higher interest rates on commercial bank deposits may be enough to hold funds there during quiet times. But it’s uncertain whether it would work during periods of tumult and the inevitable “flight to safety”.

We know from historical experience – especially in emerging market economies, but also advanced economies – that, during times of financial stress, money moves away from banks that are perceived as risky towards banks that are perceived as safer. So, money flows from privately owned banks to publicly owned ones, from domestically owned banks to foreign owned ones, and generally from weakly capitalised banks to strongly capitalised ones. In such scenarios, imagine that depositors also have the choice of putting their money in a digital currency of the central bank or in the central bank deposit account directly. It is not far-fetched to imagine that a premium would open up, where one euro of deposits in the commercial bank buys less than one euro’s worth of central bank digital currency.

Last but definitely not least, the introduction of CBDCs would change the environment in which central banks conduct monetary policy. This is, of course, the main tool that central banks have to influence the economy. The basic mechanics would stay the same: the central bank would still use its balance sheet to control short-term interest rates. But CBDCs would change the demand for base money and its composition in unpredictable ways. They might also modify the sensitivity of the demand for money to changes in interest rates.

Furthermore, if a CBDC is in demand, it would lead to a larger central bank balance sheet. This may require the central bank to hold additional assets such as government securities, loans to commercial banks or international reserves. In turn, the acquisition of these could interfere with key markets functioning or dry up liquidity. At least in a transitional period, all these changes have the potential to completely up-end the way that monetary policy affects the economy. Such changes are not ones that central banks take lightly.

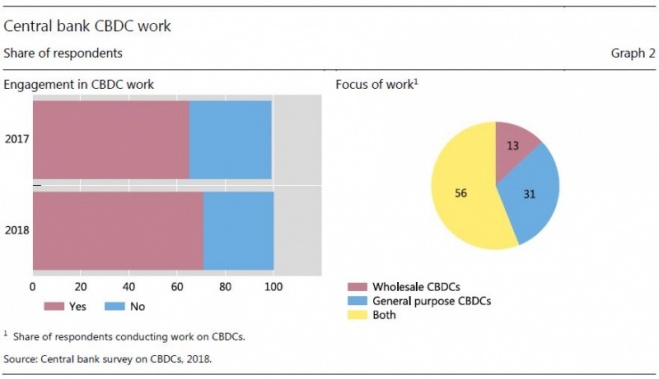

The Committee on Payments and Markets Infrastructures (CPMI) at the BIS last year surveyed central banks to take stock of current work and thinking on CBDCs.20 More than 60 central banks participated, representing countries covering 80% of the world population. Graph 2 summarises the results. Seventy per cent of central banks are working on CBDCs of some kind. Most are looking at both retail and wholesale varieties.

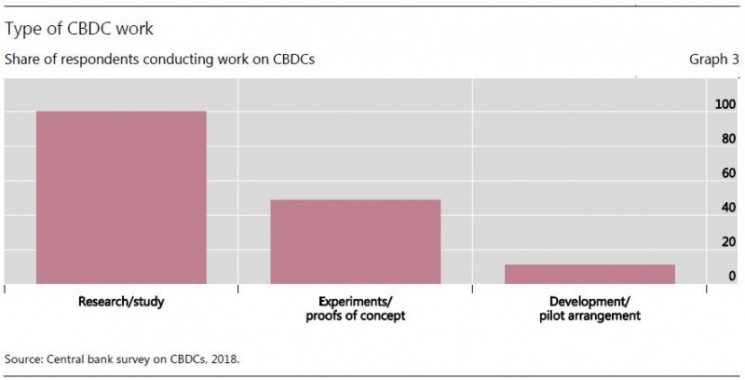

But only about half of these have moved on to the next stage of actively testing the idea (as Graph 3 shows). These central banks are examining the benefits, risks and challenges of potential issuance from a conceptual perspective. Only a couple have moved on to experimenting with the different possible technologies, in “proofs of concept” or even pilot projects.

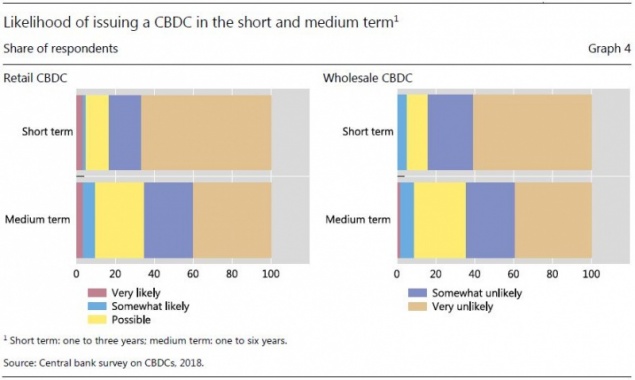

If we go one step further and ask central banks whether they plan to issue a CBDC, the picture is quite telling. As you see in Graph 4, very few central banks think it is likely that they will issue a CBDC in the short to medium term, be it retail or wholesale. Having looked into the matter, central banks have decided not to jump in.

Obviously, this is consistent with what I argued earlier, namely that: (a) the introduction of CBDCs would have a major impact on the financial system; (b) there is not yet a noticeable and widespread fall in the demand for cash; and (c) central banks do not feel compelled to face a major change in the way they conduct monetary policy. Also, research and experimentation have so far failed to put forward a convincing case. In sum, central banks are not seeing today the value of venturing into uncharted territory.

I have outlined some of the issues around CBDCs that central banks are evaluating as we move deeper into the digital age. The debate is not primarily about convenience and digitisation; rather, it’s about fundamental changes to both parts of the system that central banks oversee: money and payments. So far, experiments have not shown that new technologies would work any better than existing ones. There is no clear demand for CBDCs on the part of society. There are huge operational consequences for central banks in implementing monetary policy and implications for the stability of the financial system.

Dr Whitaker once said that the role assigned to the central bank was “to be cautious, to be the warning light”.21 Central banks are indeed proceeding cautiously and considering all relevant issues. We will flash the warning light if needed. Central banks do not put a brake on innovations just for the sake of it. But neither should they speed ahead disregarding all traffic conditions. We have to make sure that innovations set the right course for the economy, for businesses, for citizens, for society as a whole. This is what we are doing now.

2019 Whitaker Lecture by Agustín Carstens, General Manager, Bank for International Settlements at the Central Bank of Ireland, Dublin, 22 March 2019.

See M Carney, “The future of work”, Whitaker Lecture, 14 September 2018.

The Central Bank of Ireland became a member of the BIS in 1950.

BIS membership started to expand in 1996 and Board representation in 2006 with the addition of China, Mexico and the ECB; see www.bis.org/about/board.htm.

See A Chambers, Portrait of a patriot, Transworld Publishers, London, 2014. Dr Whitaker said that participating in BIS meetings helped in “elevating Ireland’s status. You might sit down beside someone like Georges Pompidou or Reginald Maudling. It also provided an opportunity for the country’s representatives to demonstrate that we comprehended technically what was going on.”

See C Borio, “On money, debt, trust and central banking”, speech at the Cato Institute, Washington DC, 15 November 2018.

See Y Mersch, “The role of cash – customer retention and tie to the citizen”, speech to The Banker, 1 September 2017.

See J Kelly, “The Irish pound: from origins to EMU”, Central Bank of Ireland, Quarterly Bulletin, Spring, 2003.

See J Hicks, Critical essays in monetary theory, Oxford University Press, 1979.

See M Bech, Y Shimizu and P Wong, “The quest for speed in payments”, BIS Quarterly Review, March 2017.

See Committee on Payments and Market Infrastructures, “Fast payments – enhancing the speed and availability of retail payments”, CPMI Papers, no 154, November 2016.

See Committee on Payments and Market Infrastructures, “Cross-border retail payments”, CPMI Papers, no 173, February 2018.

See Committee on Payments and Market Infrastructures, “Correspondent banking”, CPMI Papers, no 147, July 2016.

Sweden’s central bank, Sveriges Riksbank, has launched a preliminary study to investigate the conditions for the integration of TIPS with the Swedish payment system.

See M Bech and R Garratt, “Illiquidity in the interbank payment system following wide‐scale disruptions”, Journal of Money, Credit and Banking, vol 44, no 5, 2012.

See M Bech, U Faruqui, F Ougaard and C Picillo, “Payments are a-changin’ but cash still rules”, BIS Quarterly Review, March 2018.

Committee on Payments and Market Infrastructures and Markets Committee (2018): “Central bank digital currencies”, CPMI Papers, no 174, March 2018; and M Bech and R Garratt, “Central bank cryptocurrencies”, BIS Quarterly Review, September 2017.

See C Barontini and H Holden, “Proceeding with caution – a survey on central bank digital currency”, BIS Papers, no 101, January 2019.

See A Chambers (2014), op cit.