The link between US labor cost and price inflation has notably weakened over the past three decades. An understanding of the drivers behind this development is key, in particular from a central bank perspective, given the price stability mandate. Our empirical analysis shows that improved anchoring of inflation expectations has played a particularly relevant role, but that also increased trade integration and rising firm market power may have contributed to the decline in the pass-through from labor cost to price inflation. As the declining pass-through is linked to structural trends unlikely to revert in the near future, our findings suggest that, in the current environment, accommodative policies are not likely to add to inflationary fears via the labor cost channel, provided inflation remains low. In such an environment, our results indicate that a robust job market can be sustained without causing an outbreak of inflation. In our analysis, inflation is considered “low” as long as it remains below average, after adjustment for the long-term inflation expectations. Our analysis also shows that once inflation becomes high, according to our measure, the pass-through from a labor cost shock to inflation becomes stronger and faster.

To gauge inflationary pressures, policy makers have traditionally paid close attention to labor cost developments. Under the cost-push view of inflation, it is intuitive to expect that labor costs are an important element in a firms’ pricing decision since they constitute a substantial part of business expenses. Empirically, this view is grounded in the 1970s observed wage-price spirals.

Recent developments have however increasingly put this cost-push view of inflation into question. The period following the Global Financial Crisis has been characterized by muted inflationary developments, despite the strong labor market performance. In particular in the United States this has led to open calls as to whether labor costs are still a useful gauge for inflationary developments, by academics and policy makers alike.2

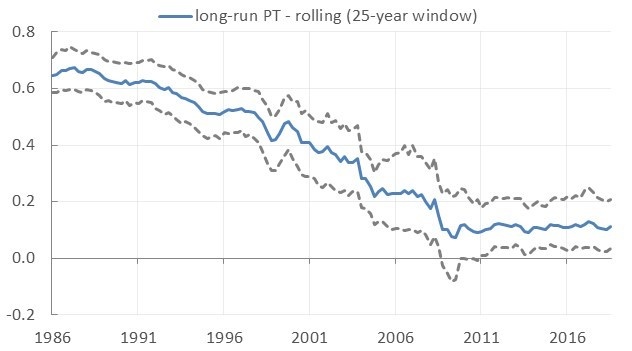

In our recent work (Bobeica et al. (2021)) we confirm empirically, using a parsimonious SVAR model, that the link between labor cost and price inflation has weakened notably.3 These findings are illustrated in Figure 1. It shows the rolling estimate of the economy-wide pass-through multiplier over the period 1960Q4-2018Q3. The multiplier is akin to those in the fiscal literature and computed as the ratio of the cumulative response of price and labor cost inflation over 40 quarters to a one standard deviation shock in labor cost inflation.

Figure 1: Estimated pass-through from labor cost to price inflation

Source: Bobeica et al. (2021), The dashed line shows the 16 and 84 percentiles.

Concretely, the Figure shows that a while in the earlier parts of the sample the pass-through was strongly positive, it has been steadily declining over time to only 0.1 towards the end of the sample.

While there is a growing body of evidence that the link between labor cost and price inflation has weakened over time, in-depth analyses of its drivers remain scant. Getting deeper insights into this question is nevertheless particularly relevant for the central bank, as it may help to understand to what extend the monetary policy can remain accommodative without the fear of inflation via the labor cost channel.

To do so, we formally investigate to what extent the declining pass-through should be seen in conjunction with other important trends that have shaped the US economy of late: (i) improved anchoring of inflation expectations; (ii) the changing constellation of shocks hitting the economy; (iii) increased trade integration and (iv) rising firm market power.

We find that all four investigated hypotheses have contributed to the declining pass-through from labor cost to price inflation in the United States, with the improved anchoring of inflation expectations having played a particularly relevant role.

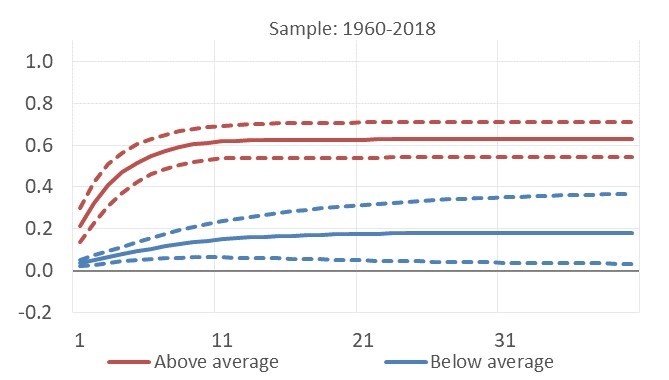

Empirically, the important role of improved anchoring of inflation expectations is illustrated in Figure 2. The Figure shows the results from our baseline VAR augmented with a Markov-switching specification with two regimes in which the switching parameters depend on whether the level and volatility of inflation (adjusted for long term inflation expectations) are above or below their historical average. The results show that when inflation – adjusted for long run inflation expectations – is above the sample average, the response of inflation to a labor cost shock is not only stronger but also more rapid. Instead, when adjusted inflation is below the sample average, the response is weak and sluggish.

Figure 2: Pass-through from labor cost to price inflation under low versus high level and volatility of price inflation

Sources: Bobeica et al. (2021)

While the inflation regime goes quite some way in explaining the declining pass-through from labor cost to price inflation, it is not the sole driver. In this regard, our analysis confirms that also the other considered factors have played a meaningful role. With pass-through being lower for supply than demand shocks4, the increased prominence of supply shocks during the 1990s may have contributed to the declining pass-through at least over that part of the sample. However, also the increase in both trade openness and firm market power offer promising avenues for understanding the decline in pass-through.

As regards trade openness, our analysis using a novel dataset covering 93 sectors between 1973Q1-2018Q3 shows that above-median trade openness at the sectoral level is associated with a lower pass-through value. However, the difference is small: the median pass-through for sectors with a relatively high degree of trade openness is close to 0.1, whereas the median pass-through of sectors with lower trade openness is around 0.3.

Finally, also changes in the pricing power of firms have played a role. The developments in firm market power at the aggregate level have already been linked to a number of secular macro trends in the United States, such as the decrease in labor and capital shares, the decline in labor participation and the slowdown in aggregate output (see DeLoecker and Eeckhout 2017 and Eggertsson 2018).

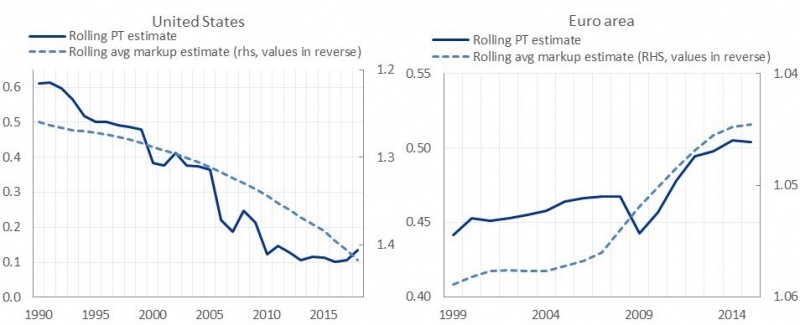

That there may indeed be a link between the degree of firm market power at the aggregate level and the link between labor cost and price inflation is illustrated in Figure 3. The chart compares for both the euro area and the US – on a rolling basis – the developments in estimated labor cost pass-through with the evolution of firm market power as proxied by an estimated measure of markup up from DeLoecker and Eeckhout (2017). This chart at prima facie would indeed confirm a very strong link between the decline in the pass-through from labor cost to price inflation and the evolution of the aggregate markup (in reverse scale).

Figure 3: The link between market power and labor cost pass-through

Sources: Bobeica et al. (2021). Note the solid series show the rolling pass-through estimate (at 40 quarter horizon) of a labour cost shock to price inflation based on a VAR estimation described above. For the United States the results are shown for a 30-year rolling window, for the euro area for a 20-year rolling window. The markup estimates are shown in reverse scale and based on De Loecker and Eeckhout (2017) and McAdam et al. (2019).

Looking at a more disaggregated level, these results are further confirmed: Using the same industry level dataset as describe above, we find that in sectors with above-median market concentration the pass through is lower, but again the difference is small: the median pass-through for sectors with above-median market concentration is around 0.1, whereas in sectors with below-median market concentration it is 0.3.

Overall, these results show that the rising trade openness and firm market power at the aggregate level both offer promising avenues for understanding the decline in pass-through and warrant further analysis. This is especially the case since these two factors, according to some narratives, may be interrelated as rising markups have been concentrated among large international companies (see for instance Autor et al 2017). These companies benefit from global networks of factors of production and are able to offset the impact of wage shocks.

The landscape in which monetary policy operates is thus shaped not only by macroeconomic dynamics at a business cycle frequency, but further complicated by slowly moving trends – such as globalization or changes in firms’ market power – which affect key relations as the one between labor costs and consumer prices.

Autor, D., Dorn, D., Katz, L., Patterson, C., and Van Reenen, J. (2017). Concentrating on the Fall of the Labor Share. American Economic Review, 107(5):180–185.

Bobeica, E., Ciccarelli, M., and Vansteenkiste, I. (2020). The Link between Labor Cost Inflation and Price Inflation in the Euro Area. In Castex, G., Gal, J., and Saravia, D., editors, Changing Inflation Dynamics, Evolving Monetary Policy, volume 27 of Central Banking, Analysis, and Economic Policies Book Series, chapter 4, pages 071–148. Central Bank of Chile.

Bobeica, E., Ciccarelli, M., and Vansteenkiste, I. (2021). The changing Link between Labor Cost and Price Inflation in the United States. Working Paper Series 2583, European Central Bank.

DeLoecker, J. and Eeckhout, J. (2017). The Rise of Market Power and the Macroeconomic Implications. Working Paper 23687, National Bureau of Economic Research.

Knotek, E. S. and Zaman, S. (2014). On the Relationships between Wages, Prices, and Economic Activity. Economic Commentary, Aug.

McAdam, P., Petroulakis, F., Vansteenkiste, I., Cavalleri, M. C., Eliet, A., and Soares, A. (2019). Concentration, market power and dynamism in the euro area. Working Paper Series 2253, European Central Bank.

Peneva, E. V. and Rudd, J. B. (2017). The Passthrough of Labor Costs to Price Inflation. Journal of Money, Credit and Banking, 49(8):1777–1802.

Powell, J. H. (2020). New economic challenges and the fed’s monetary policy review, Speech at ‘Navigating the decade ahead: Implications for monetary policy,’ a symposium sponsored by the Federal Reserve Bank of Kansas City, Jackson Hole, Wyoming. 27 august 2018, Federal Reserve System.

The views expressed are of the authors and do not necessarily reflect those of the European Central Bank.

See among other Knotek and Zaman (2014), Peneva and Rudd (2017) and Powell (2020).

We estimate an SVAR identified with a Cholesky factorization and containing quarterly data between 1960Q1-2018Q3 for three variables, namely the annual growth rates of (i) real GDP, (ii) a measures of US labor cost and (iii) the core PCE price index. To measure labor costs, we use the hourly labor compensation in the non-farm business sector and subtract from it the trend growth rate of average labor productivity. We prefer to subtract an estimate of the trend as the actual series are extremely noisy at quarterly frequency. The trend is in this regard computed as in Peneva and Rudd (2017). The two nominal variables, labor cost and price inflation, are expressed as deviations from long term inflation expectations.

A number of recent studies have argued that the link between labor cost and price inflation is shock dependent. We analyse this empirically in a six-variable SVAR with sign restrictions relying on the approach proposed in Bobeica et al. (2020) for the euro area. Concretely the VAR includes the following variables (of which the first four are expressed in growth rates): real value added, core PCE price index, nominal compensation per hour, labor productivity, the unemployment rate and a proxy for the shadow rate. This set up allows us to estimate five types of shocks: aggregate demand, aggregate supply (technology), labor supply, wage markup and monetary policy shocks in the US. The estimations confirm the results of Bobeica et al (2020) for the euro area, namely that the pass-through from labor cost to price inflation is stronger under demand, monetary policy and labor market shocks whereas aggregate supply shocks only generate a weak link between labor cost and price inflation.