The views, opinions, findings, and conclusions or recommendations expressed in this paper are strictly those of the author(s). They do not necessarily reflect the views of the Swiss National Bank (SNB). The SNB takes no responsibility for any errors or omissions in, or for the correctness of, the information contained in this paper.

Public debt managers (DMs) are tasked to ensure that governments meet their payment obligations at the lowest possible cost. A transparent and predictable framework is seen as instrumental in achieving this goal. One way to increase transparency is the announcement of a target volume before an auction. However, these targets are typically non-binding, and DMs might swerve from the announced target. For example, when they realize that the government’s financing needs have changed, they must choose between auctioning a different amount of bonds than announced or organizing an additional auction. Both options are costly.

However, there is another explanation for why the issued volume may be different from the announced target. DMs might realize a financial windfall when “beat-the-market” opportunities beckon. In our setup, potential “beat-the-market” opportunities arise from asymmetric information when the well-informed PDs sell the bonds in the secondary market. This leeway can lead to a positive correlation between an “issuance bias,” defined as the difference between the actual and the announced auction volume, and an “auction premium”, defined as the difference between the auction price and the fundamental value of the bond.

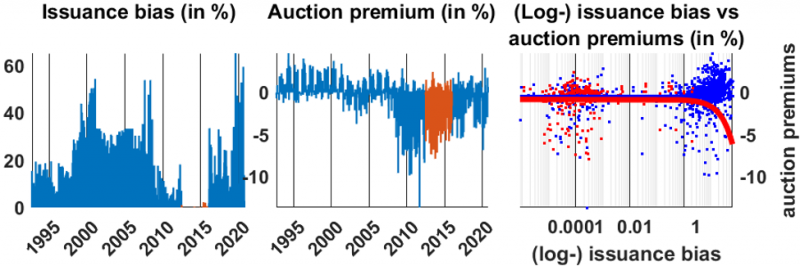

Our theoretical paper is informed by observations on U.S. data shown in Figure 1. The left-hand panel displays the issuance bias for 1,620 nominal Treasury securities with fixed coupon payments with a maturity of more than 365 days issued from September 30, 1992, to October 15, 2020. Red bars denote the period between July 2012 and December 2015, where the U.S. Treasury seems to have been strongly committed to its announcements, as evidenced by a lack of any issuance bias. However, the bulk of observations in blue suggests little commitment. The central panel shows the auction premiums. To measure the auction premiums empirically, we define the fundamental bond value as the (discounted) secondary market price of a similar Treasury bond one week after the auction. Finally, the right-hand panel shows a scatter plot for both data series in log-linear scale. When the Treasury was not committed, the correlation coefficient between the issuance bias and the auction premium was 0.22 and significant by all conventional levels (p-value = 0.00). In contrast, in the period when the Treasury seems to have been strongly committed to its announcements, the correlation coefficient was -0.01 and insignificant (p-value = 0.83).

Transparency and predictability are widely acknowledged by DMs as crucial for meeting their objectives (OECD, 2022). To this end DMs disclose their financing programs through issuance calendars. Only little theoretical or empirical research is available on the effects target announcements have on primary and secondary markets. We contribute to filling this gap. Specifically, assuming an incentive to overissue under “beat-the-market” opportunities to cash in the auction premium, we analyze whether and how DMs’ commitment to a predictable issuance policy supports a well-functioning secondary market, which, in turn, helps minimize debt servicing cost.

We ask three questions. First, what function does an announcement fulfill? We address this question at the end of the literature review. Second, what is the role of announcements for market participants? We discuss their role when we describe Figure 2. Third, what goals and conditions are required for DMs to meet their targets? This question is taken up in the final section.

Figure 1

Figure 1 The left-hand panel plots the issuance bias of 1,620 notes and bonds from September 30, 1992 to

October 15, 2020. Red marks observations between July 2012 and December 2015 while the remainders are

in blue. The central panel shows the auction premiums. The right-hand panel shows the scatter plot in log-linear scale. The lines are linear fits but appear bent because of the log-transformation.

The starting point is Friedman (1959) who characterized the practices of the U.S. Treasury’s debt management of the time as irregular, unpredictable and a source of uncertainty for the secondary market. He proposed that the amount to be sold be specified in advance and vary little from one issuance to the next.

One strand of literature explores the interplay between primary and secondary markets for sovereign bonds. There is evidence of under- and overpricing at auctions and of “auction cycles” (references are in Dentler and Rossi, 2022). In Bikhchandani and Huang (1989), resale opportunities can lead strategic bidders to bid more aggressively at auctions to signal a high valuation of the bonds to less informed secondary market participants. In our model it is costly for secondary market participants to learn the true value of a bond.

The bulk of theoretical and empirical work has been devoted to the fiscal insurance approach (or macroeconomic view) on public debt management. This line of research highlights the negative welfare impact of distortionary taxes required to fund unforeseen financial needs (Missale 2012). We accommodate a tax-smoothing/fiscal insurance rationale by means of punishing deviations from a stochastic financing need in the DM’s objective function. Our set-up is also related to the micro portfolio optimization (or finance perspective) that focuses on debt servicing costs, which in our case are captured by the auction premiums that in the end benefit taxpayers.

Another line of research focuses on time-inconsistency in debt management (Calvo and Guidotti, 1990; Missale and Blanchard, 1994). Unlike this literature, our source for advantageous market opportunities stems from a state-inconsistency where one of two states implies a haircut to the final bond repayment.

Our paper also ties in with the literature on government bond auctions (see Ranaldo and Rossi, 2016 for an overview). However, the distinction between the uniform and the discriminatory price auction format, which is at the center of this literature, plays no role in our model. Nor do we pay direct attention to the when-issued or the repo market in which Treasury securities may also be traded.

Forest (2012) asks whether announcements function as transmitters of information between DMs and the public. He found no anomaly in the volatility of secondary market yields around announcement dates. Accordingly, announcements may not reveal news systematically because the information content of an announcement is already priced in the bond. One reason could be that nowadays the timing and size of bond issuances follow a more predictable pattern than in the past. However, if market participants are not surprised by DMs’ announcements, what is their purpose? As discussed by Beetsma et al. (2018), announcements can function as a coordination device. By ensuring participation in the primary market, auction failures that affect the government’s credibility and raise borrowing costs can be avoided. Finally, the comparison between announced and realized volumes imposes discipline on DMs and limits their discretion. The focus of our paper is on this disciplining function.

The bond’s life cycle divides the single shot game into five rounds. (1) A DM announces a target volume for the upcoming bond auction, and some traders exert effort to become experts like PDs; some traders remain non-experts. (2) Nature reveals (i) government’s financing needs to the DM and (ii) the bonds’ true (long-term or fundamental) value to PDs and to expert traders. (3) The DM auctions the bonds to PDs. (4) PDs and traders form pairs and exchange bonds in the secondary market for a (generic) security. PDs may have an information advantage about the bonds’ true value, which gives rise to two types of equilibria. First, trading shuts down whenever the valuation wedge between PDs and traders is too small (“separating equilibria”). Second, sufficiently high purchasing offers made by traders allow PDs to extract information rents whenever the true bond value is low (“pooling equilibria”). Since we found empirical evidence supporting pooling equilibria, we do not discuss separating equilibria any further. (5) All payment obligations to which all agents are committed are settled.

There are two counteracting effects in pooling equilibria. First, given that PDs behave competitively in the auction, the information rents realized by the PDs benefit the DMs in the form of an auction premium that incentivizes them to overissue whenever the true bond value is low. Second, the information rents motivate traders to become experts by acquiring knowledge about the true value of the issued bonds in the first round of the game that mitigates the auction premium and the issuance bias.

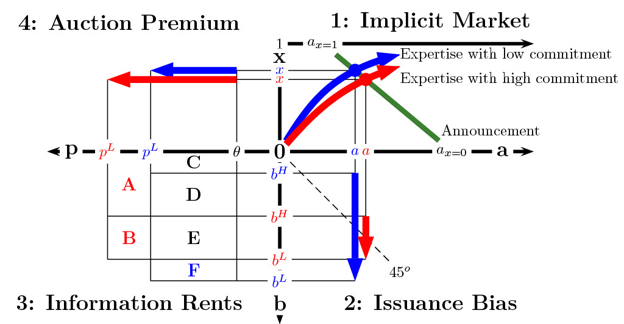

We distinguish between low and high commitment as a policy choice, and low and high true bond values for individual bond issuances. The question is: what happens when deviations from the announcement become more costly, that is, when the DM’s commitment to an announced target volume increases? Figure 2 summarizes the intuition and highlights the effects on auction outcomes and information rents. The top right-hand panel, titled “Implicit Market”, shows the announcement-expertise space. It represents the first round of the game. The DM’s announcement curve (green line) slopes downward. If all traders are expert (x = 1), the DM is not incentivized to overissue, and the announcement is equal to government’s expected financing needs. If a fraction of traders are non-experts, the DM will overissue bonds whenever the true bond value is low. The DM’s commitment does not alter the announcement curve because the DM is assumed to be risk neutral with respect to auction results. Traders’ expected trading volume coincides with the announcement because the DM has no private information at the time of the announcement and is not subject to time-inconsistent behavior so that the announcement plays the role of an incentive to become an expert. Hence, the expertise curves originate at 0 and increase in the announced bond volume. However, expertise is higher under low commitment (blue) than under high commitment (red). We explain this result in a thought experiment below. The intersection of the two curves determines the equilibrium levels of an announcement and of expertise. In other words, the announcement plays the role of a quantity in a conventional (good or financial) market, whereas expertise resembles the price dimension in an implicit market. Finally, a higher commitment reduces expertise and increases the announced volume.

Figure 2

Figure 2 The four dimensions originate at the center of the figure and represent in clockwise direction starting from the top expertise in the secondary market, x, DMs’ announcement, a, bond issuance at the auction, b, and the auction price, p. The top right-hand panel shows the implicit market for announcements (quantity) and expertise (price), the bottom right-hand the issuance bias. The bottom left-hand quadrant captures the information rents PDs can extract from uninformed traders in the secondary market, and the top left-hand quadrant shows the auction premium. Blue marks outcomes under low commitment and red the outcomes under high commitment.

The lower right-hand panel, titled “Issuance Bias”, exhibits the bond issuance-announcement space. The announcement reflects the expected bond issuance in the absence of strategic information and time-inconsistency considerations, leading announcements to play the role of an expectation anchor and meeting the expected bond issuance on the 45-degree line. However, a larger commitment reduces the issuance bias, which in the figure is measured by the difference between issuances of bonds with a high true value (bH) and a low true value (bL).

The bottom left-hand panel, titled “Information Rents”, shows the auction price-bond issuance space. The information rents extracted by PDs from non-expert traders under low commitment for bonds with low true values is given by C+D+E+F. This area is defined by the auction price pL (blue), the true bond valuation θ displayed on the p-axis, and the total issuance volume bL (blue). The area defines the financial windfall and the welfare increase due to beat-the-market opportunities (information rents) arising to DMs and, in the end, to tax payers.

Finally, the top left-hand panel, titled “Auction Premium”, shows the expertise-auction price space. Expert traders pay θ on the secondary market. The (positive) difference to the auction price pL arises from the information rents extracted from non-expert traders. As a result, a reduction in expertise (from blue to red) increases the auction premium.

The main effect from increasing a DM’s commitment to an announced target volume is a reduction in the issuance bias whenever “beat-the-market” opportunities are present. To explain this result, we conduct the following thought experiment based on Figure 2. After the announcement and the level of expertise are set, the DM’s commitment unexpectedly increases shortly before the auction. The auction price does not change under the assumption that the demand for bonds is perfectly price elastic. However, the issuance volumes, marked by bH and bL, would move towards the announced volume. Note that when commitment increases, the announced volume also increases. As a result, the DM issues more debt on average. Finally, an increased commitment also monotonically increases the auction premium.

Let’s further assume we started the game in a low (blue) commitment environment. An unexpected increase in commitment before the auction reduces the information rents in the area defined by F. In turn, the effort of traders to become experts is reduced. This explains why the expertise curve under low commitment (blue) is above the expertise curve under high commitment (red). The reduction in expertise, on the other hand, increases the auction price. However, the joint financial effect of a reduction in the issuance bias and an increase in the auction premium from “beat-the-market” opportunities is inconclusive and depends on the parameter space. Note that under high commitment the information rents are given by the sum A+B+C+D+E. Consequently, increased commitment changes the information rent extraction and the financial windfall by A+B-F. In addition, a higher commitment reduces the DM’s flexibility to respond to unexpected financial needs. Hence, the previous welfare considerations must be extended to A+B-F-G, where G represents the cost from accommodating unexpected financial needs.

Does commitment benefit trading in the secondary market, as argued by Friedman (1959)? The answer depends on the presence of opportunities to “beat the market”. An increase in commitment does not alter much in the absence of such opportunities. Commitment reduces bond issuance variation attributable to unforeseen financing needs regardless of the presence or absence of “beat-the-market” opportunities. However, some empirical and welfare predictions change when “beat-the-market” opportunities are present. We discuss these points extensively in the paper and in addition show the effects on borrowing costs from commitment.

Our paper is one of the first to address effects on market participants from a commitment to a pre-auction target announcement by public debt managers. The main result is that a commitment to such announcements limits the information rents extracted from traders in the secondary market. While this reduces the loss of non-expert traders, it also reduces their expertise and limits DMs’ flexibility to accommodate shocks to financial needs. Many questions remain open. For example, do these announcements broaden the investor base? How much does a dynamic version of this model affect the increase in debt issuance resulting from higher commitment? How do our results compare with the benefits commonly attributed to communication in monetary policy-making? One critical issue is the effect on credibility. The question whether more predictability raises a debt manager’s credibility cannot be answered because in our model commitment, and in turn credibility, is an exogenous parameter. This points to an avenue for further research. However, as shown by monetary policy analyses of reputational effects in a repeated-game time-inconsistency environment, the outcome is tricky. This fact motivated us to focus on state inconsistency and not time inconsistency.

Beetsma, Roel, Massimo Giuliodori, Jesper Hanson, and Frank de Jong. 2018. “Bid-to-cover and yield changes around public debt auctions in the euro area.” Journal of Banking & Finance, 87: 118–134.

Bikhchandani, Sushil, and Chi-fu Huang. 1989. “Auctions with resale markets: An exploratory model of treasury bill markets.” The Review of Financial Studies, 2(3): 311– 339.

Calvo, Guillermo A. and Pablo E. Guidotti. 1990. “Public debt management: theory and history.” , ed. R.

Dornbusch and M. Draghi, Chapter Indexation and maturity of government bonds. Cambridge University Press.

Dentler, Alexander and Enzo Rossi. 2022. Public debt management announcements under “beat-the-market” opportunities. SNB Working Papers 6/2022.

Driessen, Grant A. 2015. “How treasury issues debt.” CRS Report, 18.

Forest, James J. 2012. “The effect of Treasury auction results on interest rates: 1990-1999.” PhD diss. University of Massachusetts, Amherst.

Friedman, Milton. 1959. “A program for monetary stability.” Fordham University Press.

Missale, Alessandro and Olivier Blanchard. 1994. “The debt burden and debt structure.” American Economic Review, 84: 309–319.

Missale, Alessandro. 2012. “Sovereign debt management and fiscal vulnerabilities.” BIS Paper, 65.

OECD Sovereign Borrowing Outlook 2022.

Ranaldo, Angelo and Enzo Rossi. 2016. Uniform-price auctions for Swiss government bonds: Origin and evolution. SNB Economic Studies 2016-10.