References

BIS (2014). The transmission of unconventional monetary policy to the emerging markets, bis papers, no. 78 (august, 2014). https://www.bis.org/publ/bppdf/bispap78.pdf.

Angelovska–Bezhoska, A., Mitreska, A., and Bojcheva–Terzijan, S. (2018). Unconventional monetary policy had large international effects. Journal of Central Banking Theory and Practice, 2:25–48.

Backé, P., Feldkircher, M., and Slacík, T. (2013). Economic spillovers from the Euro area to the cesee region via the financial channel: A gvar approach. Focus on European Economic Integration, Oesterreichische Nationalbank (Austrian Central Bank), issue 4, pages 50–64.

Bluwstein, K. and Canova, F. (2015). Beggar-thy-neighbor? the international effects of ECB unconventional monetary policy measures. CEPR Discussion Papers 10856, C.E.P.R. (October 2015).

Ciarlone, A. and Colabella, A. (2016). Spillovers of the ECB’s non-standard monetary policy into cesee economies. Revista ESPE – Ensayos sobre Política Económica, Banco de la Republica de Colombia (December 2016), 34(81):175–190.

Fadejeva, L., Feldkircher, M., and Reininger, T. (2014). International transmission of credit shocks: Evidence from global vector autoregression model. Bank of Latvia Working Paper No.5/2014.

Feldkircher, M., Gruber, T., and Huber, F. (2017). Spreading the word or reducing the term spread? assessing spillovers from Euro area monetary policy. Department of Economics Working Paper Series No. 248, WU Vienna University of Economics and Business, Vienna.

Falagiarda, M., McQuade, P., and Tirpak, M. (2015). Spillovers from the ECB’s non-standard monetary policies on non-Euro area eu countries: evidence from an event-study analysis. Working paper 1869, ECB 2015.

Hájek, J. and Horváth, R. (2016). The spillover effect of Euro area on Central and Southeastern European Economies: A global VAR approach. Open Economies Review, Springer, 27(2):359–385.

Horváth, R. and Voslárová, K. (2017). International spillovers of ECB’s unconventional monetary policy: the effect on Central Europe. Applied Economics., 49(24):2352–2364.

Moder, I. (2017). Spillovers from the ECB’s non-standard monetary policy measures on Southeastern Europe. Technical Report, European Central Bank.

Appendix

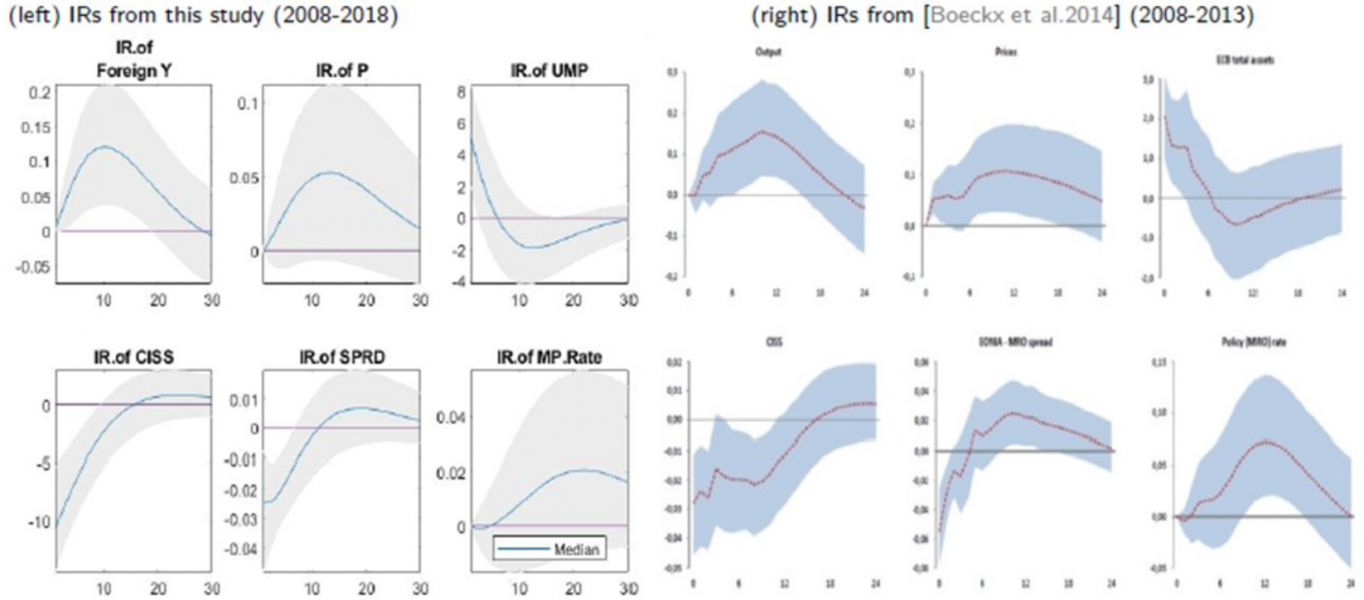

Figure A.1: Response of EA variables following ECB’s UMP shock

(left – IRs from this study; right – IRs from Boeckx et al. (2014), figure 4, p.25).