This policy brief argues that the current EU’s fiscal policy framework calls for a paradigm shift in how the fiscal policy framework is designed, as opposed to the incremental reform approach of recent decades. This should include improved governance of fiscal rules, which should be simpler, more functional and credible than the current ones, but it should also go a step further and incorporate supranational risk-sharing components enabling the smooth operation of the monetary and fiscal policy mix, from a wider euro area perspective. We highlight several challenges with a bearing on any reform process in the current setting: (i) medium-term debt anchors should be adapted to the medium and long-term interest rate and potential growth expectations; (ii) economies may remain subject to very severe shocks, meaning that fiscal space must be recovered in the medium term; and (iii) realistic mechanisms for absorbing existing fiscal imbalances must be implemented.

There is a broad consensus on the need to reform the fiscal governance framework in the European Union (EU).2 While the available evidence shows the benefits of having a reference framework of national fiscal rules in the euro area, such as that provided by the Stability and Growth Pact (SGP),3 the consensus on the need for reform is based on the shared perception that the current system has been unable to achieve its two main objectives: (i) to turn countercyclicality into a benchmark for fiscal policies, which would have enabled space to be created during upswings for use in downturns, in particular in severe crises such as the global financial crisis and the recent health crisis;4 and (ii) to provide a fiscal policy stance that is consistent with the macroeconomic needs of the euro area as a whole.

In February 2020 the European Commission (EC) launched a public consultation to set in motion a reform of the fiscal framework, that is expected to be re-launched soon after the resolution of the health crisis. The debate on the need for reform is nothing new; it has gone hand in hand with discussions on the operation and application of the SGP and progress towards greater euro area integration in recent decades.5 In light of the health crisis, the SGP’s general escape clause was activated and no date has been set for the return to normalcy. The clause allows Member States to undertake budgetary measures to deal adequately with extraordinary shocks, within the corrective and preventive procedures of the SGP. According to the EC, the decision to deactivate the general escape clause should be taken based on an overall assessment of the state of the economy based on quantitative criteria, with the level of economic activity in the EU compared to pre-crisis levels as the key quantitative criterion. Thus, on the basis of the EC’s Spring 2021 Economic Forecast, the general escape clause will continue to be applied in 2022 and is expected to be deactivated as of 2023.

The debate on the reform of the fiscal governance framework in the EU is raging, with several different contributions being made. These can be grouped into three blocks. First, the proposals for simplifying the fiscal rules and strengthening their governance arrangements6. Second, the need to incorporate new supranational fiscal policy components that contribute to the euro area’s macroeconomic stabilisation is underscored7. Lastly, proposals suggest the reforms in the fiscal arm need to be part of, and contribute to, a more ambitious process to implement the reforms required to complete an optimally functioning monetary union8.

Irrespective of their political feasibility, these proposals do not easily fit the current macroeconomic environment. The setting for this necessary reform bears little resemblance to that of the 1990s, when the cornerstones of the current model for euro area fiscal policy coordination were laid. Over recent decades, far-reaching structural trends, such as digitalisation, globalisation, climate change and population ageing, have emerged or taken hold. These trends are largely triggering lower natural rates of interest and influencing potential output growth rates, at least in advanced economies. Also, after the Great Moderation, the European and world economy has, over the last 15 years, suffered particularly severe global shocks.

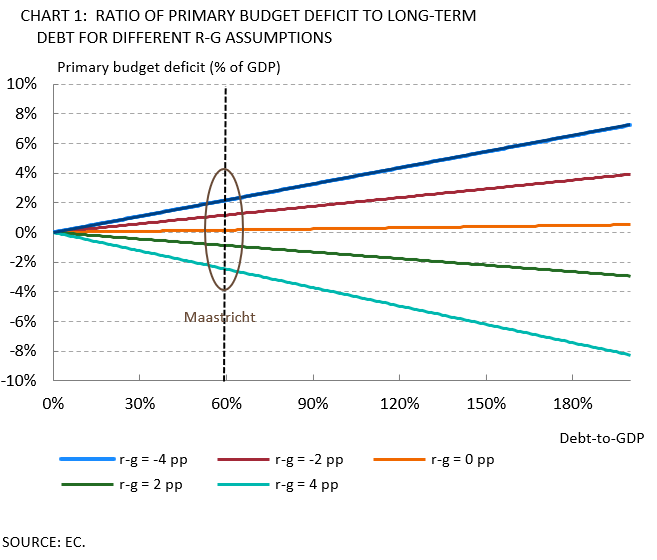

On the one hand, the quantitative limits of Maastricht Treaty were defined taking into account, approximately, the average economic situation at the end of the 1990s. Assuming potential growth of 2% and an inflation target of 2%, a budget deficit limit of 3% of GDP would stabilise the ratio of government debt to GDP at 60%. These reference values were set uniformly for all EU Member States. Around the time the SGP came into force, the r-g differential was positive, at close to 2 pp on average in the period 1995-1999. As a result, the medium-term stabilisation of existing government debt levels at around 60% (with inflation of 2%, i.e. the ECB’s target) was consistent with running an overall budget balance of around -3% of GDP. In the current context, however, and given the budget deficit reference value of 3% of GDP, the trend towards negative r-g differentials would be consistent with government debt levels stabilising at a higher percentage of economic output (see Chart 1).

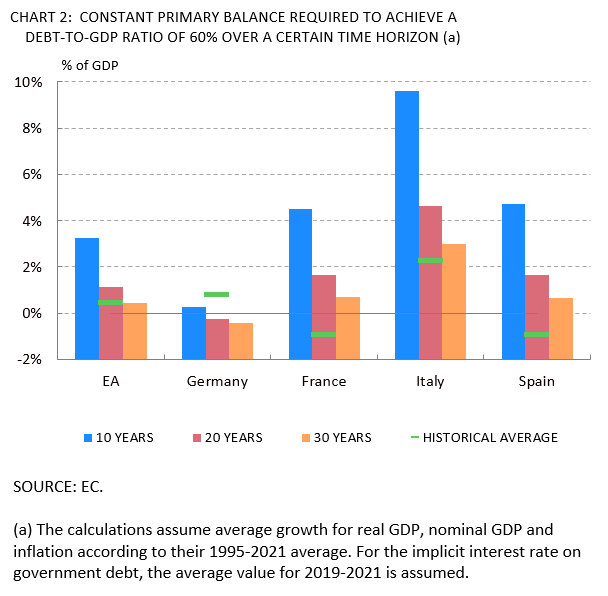

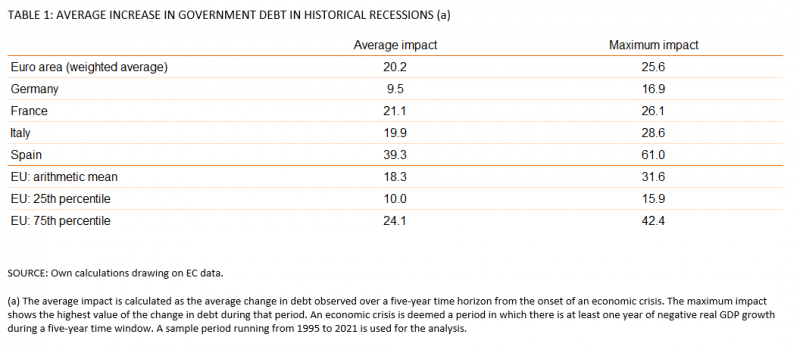

On the other hand, the current high levels of government debt evidence the difficulties of transitioning to the medium-term debt anchors. At present, converging towards a debt-to-GDP ratio of 60% would call for a concerted and constant fiscal effort over a prolonged time frame, thereby also limiting fiscal policy’s stabilisation capacity for the duration of the adjustment process. Thus, using the historical average values of real growth, inflation and interest rates, the euro area would need to maintain a fiscal surplus of 1.1% of GDP over 20 years in order to reduce the debt ratio to 60% (see Chart 2). This is substantially higher than the average primary deficit of 0.4% of GDP observed for the euro area as a whole since 1995. This is especially relevant given the need to recoup fiscal policy space in the medium term. Following an economic crisis, public finances tend to deteriorate as fiscal policy is used to stabilise the economy. The trajectory towards fiscal consolidation should take into account the likelihood of a further economic crisis and the fiscal room for manoeuvre needed to combat it. This headroom could be quantified in a highly stylised form, using the average change in the government debt ratio in the five years following an economic crisis. From a historical perspective, this change in the government debt ratio has been close to 20 pp for the euro area as a whole, although there is a high degree of cross-country heterogeneity, largely reflecting differing output volatility and other specific factors (see Table 1). In view of the difficulty faced by countries in achieving the fiscal buffer needed to attain appropriate economic stabilisation in the event of a recession, it is worth discussing the part that supranational headroom could play in the transition towards healthier fiscal positions. Moreover, an institution like the ESM could play a significant role in mitigating potential sovereign risks, acting as a backstop in the event of shocks affecting some countries.

Additionally, an appropriate framework for the interaction of fiscal and monetary policy needs to be desgined. The latest economic crises have shown the multiple ways in which fiscal and monetary policy can interact. First, monetary policy can provide fiscal policy with room for manoeuvre.9 Second, when interest rates are at their lower bound, countercyclical fiscal policy complements monetary policy.10,11 At the same time, fiscal policy can also help make monetary policy more effective, in an environment of persistently low inflation, by pushing the natural rate of interest upwards12. In any event, the requirements for effective fiscal stabilitisation for the monetary union as a whole are more demanding than the framework for policy coordination between Member States in the current setting for a number of reasons. First, because current rules do not envisage mechanisms for correcting national measures that are judged to be incompatible with the overall desired fiscal stance. And second, because having an appropriate union-wide fiscal stance does not guarantee that individual fiscal policies are adequate for the national fiscal sustainability and cyclical stabilisation targets, as has been observed in recent years. A possible way forward out of this coordination problem could be to establish a central mechanism entrusted with setting the euro area’s overall fiscal policy stance, with national authorities carrying out their actions autonomously and in strict compliance with SGP rules.

The new global macroeconomic environment and the experience of the last 25 years warrant a paradigm shift in the design of the governance framework, as opposed to the incremental approach of recent decades. This should include improved governance of fiscal rules, which should be simpler and more functional and credible than the current ones, but it should also go a step further and incorporate supranational risk-sharing components enabling the smooth operation of the monetary and fiscal policy mix, from a wider euro area perspective. Also, the medium-term anchors should be adapted to the specific interest rate and potential growth environment at each point in time, recognise that economies may continue to be subject to very severe shocks and, at the same time, develop realistic mechanisms for absorbing existing fiscal imbalances. Nonetheless, the foregoing should take into account the need to recover fiscal space in the medium term, which entails application of a prudent, transparent and credible fiscal policy framework.

Altavilla, C., M. Boucinha and Peydro, J. (2018). “Monetary policy and bank profitability in a low interest rate environment”. Economic Policy, Volume 33, Issue 96, pp. 531– 586.

Alloza, M., Andrés, J., Burriel, P., Kataryniuk, I., Pérez, J. J. and J. L. Vega (2021). “The reform of the European Union’s fiscal governance framework in a new macroeconomic environment”, Occasional Paper No 2121, Banco de España.

Andrés, J., P. Burriel and W. Shi (2020). “Debt sustainability and fiscal space in a heterogeneous Monetary Union: normal times vs the zero lower bound”, Working Paper No 2001, Banco de España.

Andrle, M., J. Bluedorn, L. Eyraud, T. Kinda, P. K. Brooks, G. Schwartz and A. Weber (2015). “Reforming Fiscal Governance in the European Union”, IMF Staff Discussion Note 15/09.

Arce, Ó., S. Hurtado and C. Thomas (2016). “Policy Spillovers and Synergies in a Monetary Union”, International Journal of Central Banking, 12(3), pp. 219-277.

Banco de España (2017). Chapter 4, “Fiscal policy in the euro area”, of Annual Report 2016.

Beetsma, R., N. Thygesen, A. Cugnasca, E. Orseau, P. Eliofotou and S. Santacroce (2018). “Reforming the EU fiscal framework: A proposal by the European Fiscal Board”, VoxEU.org, 26 October.

Bénassy-Quéré, A. et al. (2018). “Reconciling risk sharing with market discipline: A constructive approach to euro area reform”, CEPR Policy Insight No 91.

Brunila, A., M. Buti and D. Franco (eds.) (2001). The stability and growth pact: the architecture of fiscal policy in EMU, Springer.

Burriel, P., F. Martí and J. J. Pérez (2017). “The impact of unconventional monetary policy on euro area public finances”, Economic Bulletin, Banco de España.

Burriel, P., P. Chronis, M. Freier, S. Hauptmeier, L. Reiss and D. Stegarescu (2020). “A fiscal capacity for the euro area: lessons from existing fiscal-federal systems”, Occasional Paper No 2009, Banco de España.

Christiano, L., M. Eichenbaum and S. Rebelo (2011). “When Is the Government Spending Multiplier Large?”, Journal of Political Economy, 119(1), pp. 78–121.

European Commission (2020a). “Communication on Economic Governance Review – Report on the application of Regulations (EU) No 1173/2011, 1174/2011, 1175/2011, 1176/2011, 1177/2011, 472/2013 and 473/2013 and on the suitability of Council Directive 2011/85/EU”, Brussels.

European Fiscal Board (2020). Annual Report.

Eyraud, L., M. X. Debrun, A. Hodge, V. D. Lledo and M. C. A. Pattillo (2018). “Second-generation fiscal rules: Balancing simplicity, flexibility, and enforceability”, International Monetary Fund.

Fournier, J. (2016). “The positive effect of public investment on potential growth”, Working Paper No 1347, OECD Economics Department.

Galí, J. and R. Perotti (2003). “Fiscal Policy and Monetary Integration in Europe”, Economic Policy, October, pp. 533-572.

Gaspar, V. (2020). “Future of Fiscal Rules in the Euro Area”, Keynote speech at workshop on “Fiscal Rules in Europe: Design and Enforcement” organised by DG ECFIN. Brussels. Available at: https://www.imf.org/en/ News/Articles/2020/01/28/sp012820-vitor-gaspar-fiscal-rules-in-europe

González-Páramo, J. M. (2005). “The reform of the Stability and Growth Pact: an assessment”, speech at the conference on “New Perspectives on Fiscal Sustainability”, Frankfurt, 13 October.

Gordo, E. and I. Kataryniuk (2019). “Towards a more resilient euro area”, Economics and Business Letters, 8, pp. 106-114.

Hernández de Cos, P. (2020). “The European response to the COVID‑19 crisis”. Opening address – Fundación Internacional Olof Palme Conference, 13 November.

Hernández de Cos, P. and J. J. Pérez (2015). “¿De la reforma del pacto de estabilidad a la unión fiscal?”, Euro Yearbook 2015, pp. 209-222.

Kopits, G. (2001). “Fiscal Rules: Useful Policy Framework or Unnecessary Ornament?”, IMF Working Paper No 01/145.

Larch, M., E. Orseau, and W. van der Wielen (2021). “Do EU fiscal rules support or hinder counter-cyclical fiscal policy?”, Journal of International Money and Finance, 112, 102328.

Leeper, E. M., T. B. Walker and S. C. S. Yang (2010). “Government Investment and Fiscal Stimulus”, Journal of Monetary Economics, 57, pp. 1000-1012.

Martin, P., J. Pisani-Ferry and X. Ragot (2021). “Reforming the European Fiscal Framework”, Les notes du conseil d’analyse économique no 63.

Martínez Mongay, C., E. Feás, M. Otero Iglesias and F. Steinberg (2021). “Elementos de discusión para una reforma de la gobernanza de la Unión Económica y Monetaria”, Documento de Trabajo 4/2021, Real Instituto Elcano.

Rodríguez, L. and C. Cuerpo (2019). “Some elements for a revamped fiscal framework for Spain”, Working Papers, No 2018/03, Autoridad Independiente de Responsabilidad Fiscal.

Thygesen, N., R. Beetsma, M. Bordignon, X. Debrun, M. Szczurek, M. Larch, M. Busse, M. Gabrijelcic, L. Jankovics and S. Santacroce (2021). “High debt, low rates, and tail events: rules-based fiscal frameworks under stress”, VoxEU.org. Available at: https://voxeu.org/article/rules-based-fiscal-frameworks-under-stress

This policy brief is based on a recently published Occasional Document by Bank of Spain. See Alloza et al. (2021).

See, among others, Andrle et al. (2015), Hernández de Cos and Pérez (2015), Beestma et al. (2018), Banco de España (2017), Benassy-Quéré et al. (2018), Eyraud et al. (2018), Rodríguez and Cuerpo (2019), Gaspar (2020), Thygesen et al. (2020), European Commission (2020a), European Fiscal Board (2020), Martin et al. (2021), Martínez Mongay et al. (2021) and the sequence of comments on the VoxEU website on the EU Economic Policy and Architecture after Covid debate moderated by J. Pisani-Ferry and J. Zettelmeyer.

See Kopits (2001) for a methodological discussion on the benefits and desirable features of fiscal rule frameworks from a general perspective.

J. Galí and R. Perotti (2003) show how SGP signatories’ discretionary fiscal policy became more countercyclical after the pact’s first years in force than in the preceding decades. However, Larch et al. (2021) show how fiscal policy has been procyclical in the EU (and in a broader set of advanced countries) in recent decades. According to this study, compliance with fiscal rules makes fiscal policy more countercyclical.

See Brunila et al. (2001) for a review of the earliest debate. González-Páramo (2005) provides a comprehensive overview of the initial conceptual discussions about the fiscal rules framework and its interaction with monetary policy.

See Martin et al. (2021).

See Banco de España (2017).

See Banco de España (2017), Gordo and Kataryniuk (2019) and Burriel et al. (2020).

See Burriel et al. (2017), Andres et al (2020) and Hernández de Cos (2020).

See Christiano et al. (2011) and Arce et al. (2016).

Moreover, fiscal policy should ensure central banks’ capacity to implement their non-standard policies and, in particular, their viability, by preserving the value of their massive purchases of government debt, i.e. by guaranteeing that government debt is a safe asset.

Leeper et al (2010) and Fournier (2016).