The views and opinions expressed in this article are those of the authors and do not necessarily reflect the view of the Deutsche Bundesbank or the Eurosystem.

After decades of low inflation in the developed world, inflation is increasing significantly over the past months in many countries. Academics and central bankers alike emphasize the critical role of inflation expectations for actual inflation. Already in the time of the effective lower bound, managing inflation expectations was seen as one of the few ways to influence inflation. Nowadays, in times of high inflation rates, central banks globally aim to “anchor” and manage inflation expectations. However, it is still a perennial question how households form their inflation expectations and which factors influence them.

We investigate the relationship between inflation perceptions and inflation expectations. We use micro-data from the Bundesbank Online Panel Households (BOP-HH) on individuals in Germany. This survey contains rich data on inflation perceptions and various measures for short- and long-term inflation expectations. The panel dimension allows studying how the within-person variation in inflation perceptions feeds into expectations.

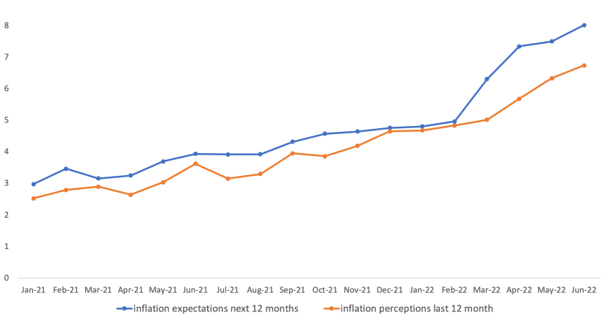

Figure 1 displays the time series of households’ inflation perceptions and short-term expectations. It is striking how closely perceptions and expectations move together; the time series look very similar.

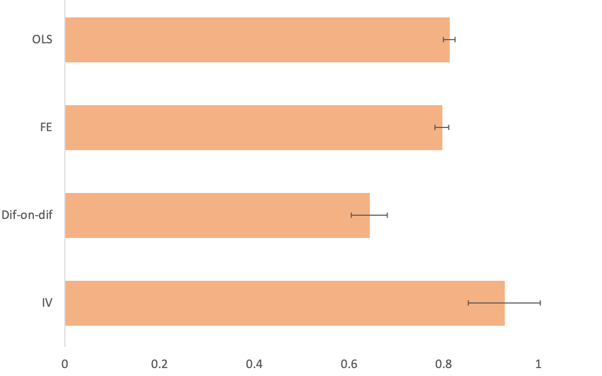

We investigate the link more formally using regressions methods on micro data and find a significant positive relationship between households’ expected short-term inflation over the next 12 months and households’ perceived inflation over the past 12 months (Figure 2). A one percentage point increase in households’ perceptions is associated with a 0.81-pp increase in expected short-term inflation. This effect is quantitatively large.

Figure 1: Mean inflation expectations and inflation perceptions of individuals over time

Sources: Bundesbank Online Panel Households (BOP-HH). Expectations and perceptions: Weighted means, observations truncated to interval [-5;+30].

We also exploit the panel dimension of our data and estimate a fixed-effects model. The panel dimension allows studying how the within-person variation in inflation perceptions feeds into expectations, and thus provides stronger evidence for a causal relationship. In addition, we conduct a change–on–change panel regression. The panel regressions (Figure 2) confirm that inflation perceptions have a positive, sizable, and statistically significant impact on short-term inflation expectations. Finally, to study the causal relationship between inflation perceptions and inflation expectations, we conduct instrumental variable regressions. We use the lagged value of inflation perceptions and the lagged overall CPI index to instrument current inflation perceptions. The results from an IV estimation confirm the findings of OLS and panel regressions (Figure 2).

Inflation perceptions also play a crucial role for long-term inflation expectations, for the next five years on average as well as for the next ten years on average. A positive, sizable, and highly significant impact remains even after we control for short-term expectations. Long-term expectations are thus directly and indirectly, via the effect on short-term expectations, affected by households’ inflation perceptions.

During the time period April to June 2019 and April 2020 to July 2021, the German economy experienced a stable and low inflation rate equal to 1.1% on average. For the time period from July 2021 to June 2022, the average inflation rate was much higher and equaled 5.6%. We split the sample into a low-inflation (before July 2021) and high-inflation environment (after July 2021), and the relationship between perceptions and expectations is sizable and highly significant in both periods. However, individuals seem to place more weight on their perceptions when forming inflation expectations in the low- compared to the high-inflation environment.

Figure 2: Regression Results: Estimated coefficients of inflation expectations on inflation perceptions

Notes: The top bar presents the OLS estimates. The second bar shows estimates of the panel fixed effect regression. The third bar presents the estimates from the panel change-on-change regression. The bottom bar shows the IV estimate. The black lines denote 95% confidence intervals. The data for OLS and panel regressions span waves 1-30 (April-June 2019, April 2020 – June 2022) of the survey. The data for IV regression span waves 1-27 (until March 2022).

We investigate two factors that moderate the pass-through from inflation perceptions to inflation expectations, information acquisition and uncertainty about future inflation. We study information acquisition by adding two questions to one survey wave. The first question asks whether consumers have received any information about inflation in Germany recently. The second question asks individuals about the primary information source used to form inflation perceptions (own shopping experience versus things they have heard or read).

We find that both aspects of information acquisition have a direct effect on inflation perceptions. Reported inflation perceptions are significantly higher for uninformed individuals (i.e., those who did not hear or read anything about inflation over the last four weeks) and for those who rely primarily on their own shopping experience when forming inflation perceptions. However, information acquisition does not affect short-term inflation expectations directly. The impact on short-term inflation expectations works through perceptions.

Individual uncertainty about future inflation affects the pass-through from perceptions to expectations. We observe a U-shape pattern for the relationship between inflation perceptions and inflation expectations depending on the uncertainty level. Consumers with low and high uncertainty rely more on inflation perceptions when forming inflation expectations, but this relationship weakens for the intermediate uncertainty range.

Our analysis shows that perceived inflation plays a crucial role in forming inflation expectations. Information acquisition and uncertainty are essential determinants of the strength of this relationship. Our findings are relevant for policy. They suggest that in seeking to influence and anchor inflation expectations, central bankers could spend further effort on managing inflation perceptions.