In the first half of 2022 we’ve witnessed a profound change in the global macro-financial regime. Inflation is the order of the day, but its seeds were sown long ago. Over and above the monetary dynamics, analysts, commentators and investors should look to understand the psychological dimension that underpins an inflationary spiral, and contributes to the self-fulfilling phenomenon. Policymakers are likewise having to adjust their reaction functions to the new framework. The era of the ‘Great Coincidence’ in the policy mix and ultra-cheap money is coming to an end at a time of looming stagflation. New dynamics are emerging between the monetary and fiscal authorities, as they simultaneously attempt to grapple with inflation and meet critical new sets of public expenditure, in the wake of the Covid pandemic, the conflict in Ukraine and the green transition. All of these elements contribute to the greater narrative of an ongoing regime shift, with profound consequences for investors.

In the first half of the year, inflation data exceeded the expectations of many analysts and commentators. Annual consumer price inflation readings reached their highest levels in decades, both in developed (DM) and emerging markets (EM), with some variation across regions. Within this context, collective attention has shifted to understanding the mechanisms that underpin inflation. In particular, inflation has two main dimensions: it is as much a monetary phenomenon, as it is a psychological one. In this paper I will address each of these components, and explore how they are interconnected.

Looking at the monetary side first, the velocity of money – the rate at which money supply is transacted in an economy over a given time – has been declining since the 1990s. This downtrend was exacerbated by the Covid-19 pandemic and reflects lower activity levels together with monetary and budgetary support. At the same time, increased asset prices show that velocity in the financial sphere has trended higher. Hence, consolidating the real and financial spheres into a unique notion of velocity, an inflationary process has effectively taken place. In fact, excess liquidity in the real sphere typically occurs at the bottom of the activity cycle, and monetary accommodation helps transfer this surplus into the financial sphere. Therefore, a holistic notion of velocity should consider both real and financial transactions per unit of money.

In general, higher velocity in one sphere comes at the expense of a slowdown in the other, although periods of simultaneous expansion or contraction can also occur. The strong linkage between the two realms is also the reason why a financial crisis often leads to an economic recession. Household savings feed financial markets, while divestments and investment payments in financial assets (i.e. dividends, coupons) transfer money back into the real economy, where it can either be spent or channelled into markets again. For some time, deceleration in money velocity masked inflation in the real sphere. In reality, an inflationary process was taking place in the financial world and is now moving back into the real one, as a consequence of the ongoing regime shift. On top of this, inflation may become a self-fulfilling phenomenon due to its psychological dimension.

An expansion in the monetary base alone is insufficient to trigger an inflationary spiral: a shift in the psychological referential must simultaneously occur. The referential is framed by the link between long- and short-term memory, and forgetfulness. Inflation is a discovery process of memory awakening and adaptive expectations; people discount the future in much the same wat that they remember and forget. A sudden shift in data (successively higher readings each month) builds up the collective’s short-term memory that brings the long-term reference back to the forefront. This is what happened over the past year or so. Perceived inflation is a memorised variable with powerful hereditary traits. By publicising the presence of inflation through rate hikes, the existence of the threat is recognised and thereby accelerated. In this sense, inflation is a self-propelling phenomenon. Moreover, psychology and inflation are intrinsically related through psychological time, whereby time appears to fly during periods of inflation, in both the real and financial spheres. For example, one hour in normal circumstances may seem like one day under hyperinflation.

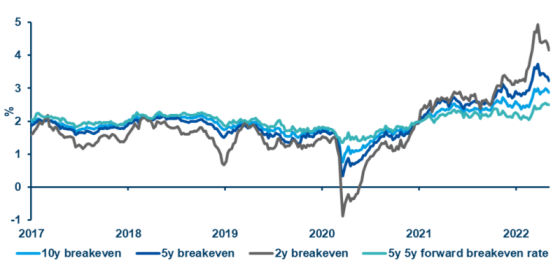

Figure 1. US market inflation expectations are awakening

Source: Amundi Institute on Bloomberg data, as of 11 May 2022.

As inflation persists and experience of the past decade (memories of disinflation/deflation) gradually fades, market attention will revert to the long term reference (the ‘70s or stagflation). Short term inflation readings currently overshoot the long term average by the widest margin since the ‘80s. In the past, this has been accompanied by higher inflation expectations. Another intrinsic element of the regime shift is that the process is self-sustaining – there is inflation when people believe there is inflation. In fact, collective memory plays a fundamental role. History does not repeat itself but, rather, the psychology of people remains relatively constant. Few people today have a vivid recollection of the great inflation in the ‘70s, and they have not been faced with any sustained period of rising prices. The past decade of secular stagnation proliferated a widespread belief that post-Covid inflation would be short-lived, whereas this is not the case. Big (historical) core narratives are framed by a coefficient of forgetfulness: the further in the past the event, the greater the coefficient. Through sudden non-linear jumps, a short term event can ignite dormant memory patterns which trigger inflation in the real sphere. This is likely where we are today.

Narratives also play an important role in spreading inflation. Mathematically, narratives behave like a virus, turning inflation into a mass phenomenon with feedback loops and self-fulfilling prophecies. Evidence of this can be seen through inflation in areas not hit by bottlenecks, but caused by the simple contagion of talks, narratives and stories on TV. The spread of narratives in media has created anxiety and fear. Social worries have risen rapidly, as the poorest are often hit the hardest, and pre-existing social divisions have been exposed. Moreover, the power of media today is arguably greater than ever, and this too is an important dimension. Interestingly, there is a discrepancy between academic and non-academic expert opinion, and the public’s perception about inflation. Whereas the experts agree that a Fed rate hike is deflationary, it is believed an inflationary move by the public1, which discounts it on personal expenditures (higher cost for mortgages, loans, etc.) and consequently projects higher wages in a negative feedback loop for prices. This is a critical consideration in terms of Central Bank (CB) action and self-fulfilling expectations.

In the current inflationary environment there is a high pressure on policymakers to provide protection and compensation on the budgetary side (e.g. blocked prices, subsidies, fiscal transfers). Inflation often leads to more fiscal accommodation rather than less, which in turn contributes to the dynamics of inflation itself through both real and psychological channels. Lately, CBs have been criticised for having fallen behind the curve on inflation. Now, they are caught in the crossfire between killing inflation at the risk of triggering a recession, or letting it run to stimulate nominal growth with a hefty price to be paid later on.

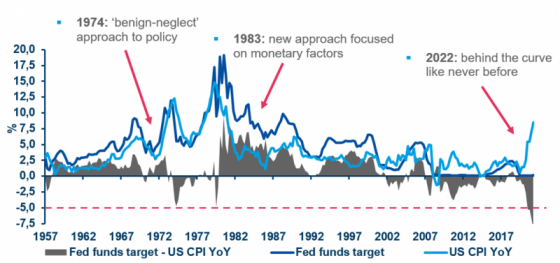

By any reasonable measure, the Fed has fallen behind the curve on inflation. A Taylor-type monetary policy rule points to an approximate 300 bps gap. Likewise, a forward guidance approach corroborates that the Fed is behind (although relatively less than the Taylor rule suggests), since markets have already moved ahead of the bank’s effective action. Two historical precedents – where core PCE was as high as today – come to mind. In 1974 the Fed downplayed the monetary factors that contribute to price increases and kept the policy rate low, causing higher inflation, economic volatility and multiple recessions. In 1983, it had learned its lesson and raised rates despite falling inflation, stabilising the economy until the 1990-1 recession.

Figure 2. The Fed and the historical precedents of 1974 and 1983

Source: Amundi Institute on Bloomberg data, as of 27 April 2022.

Although the jury is still out, I think today we are closer to a ‘74-style scenario; the initial ‘behind the curve’ gap is similar. The longer the Fed delays taking severe action, the higher the terminal policy rate will have to be. Nevertheless, it is unlikely that a full policy normalisation will occur because of the recessionary risk that it entails. The consequences of a conservative policy stance will be higher, persistent, and self-perpetuating inflation. The ex-post rate will remain relatively low for some time, but nominal rates will trend upwards, with no way to stabilise volatility in the real economy. The epilogue will nevertheless be a recession which, while it can be delayed, cannot be avoided altogether.

As we move towards a new economic and financial regime, governments will assume control of money while maintaining double-digit monetary growth for several years, thus facilitating the transition from free market, independent CB rule-based policies towards a command-oriented economy. Additionally, huge fiscal accommodation is required to finance the post-Covid recovery as well as the energy transition in the fight against climate change; the need for independence on the energetic front was further accentuated by the conflict in Ukraine. Fiscal expansion must necessarily come from a continuation of the financial repression environment, with CBs staying behind the curve to allow further debt expansion at sustainable costs. This could build the conditions for the simultaneous financing and expansion of the real and financial spheres, leading to temporary increases in the prices of assets, goods and services.

Overall, we are reaching the end of the great monetary consensus. The independent CB model (‘one tool, one objective’) is no longer applicable in an increasingly fragmented world; hyperbolically, there are as many policy reaction functions as there are countries facing inflation. While the public debate has been focused on the monetary side, we should look at the overall policy mix in order to understand the novel role of monetary policy. The current popular consensus is that certain critical needs must be fulfilled on the budgetary front. However, the widespread belief that fiscal spending is effectively unlimited (i.e. the fiscal ‘free lunch’) is going to be severely tested in the new macro-financial regime. Moving forward I see three possible scenarios for the policy mix:

While public opinion is mostly focused on the first option, I believe the second or third are more likely. Fiscal spending must target critical new sets of public goods (the energy transition, social and strategic autonomy) and central banks will have to accommodate these priorities. This is particularly true in Europe, where the monetary authorities have to fill the void left by the lack of credible budgetary rules. The worst-case scenario is full-blown stagflation. If nothing is done on the fiscal side, then mechanically there will be a tightening in the policy mix, reversing the trend of the past few years.

In the current and uncertain environment, a global repricing of risk is underway. It started with bonds, particularly on the short end of the yield curve, but has since paused; this should remain paused or even retreat as the central bank delivers less than required, feared or priced into the market. The final leg of this repricing will occur with additional pressure at the long end, via a steepening of the curve, signalling an inflection point for risky assets and a preference for bonds. Large insurers and pension funds will play an important stabilising role in this respect. Another consequence of the inflationary regime is a change in correlation dynamics; higher inflation is turning the correlation of equity and bonds positive, challenging basic portfolio construction tenets.

In general, the performance of equities and bonds will deteriorate or even reverse, provoking widespread underperformance. The repricing point in equities should see a tilt towards value and quality (away from tech and more ‘glamorous’ but less solid business models), while the lagging repricing of credit should catch up and could finally close the gap. Further repricing in equities and credit would provide a more comfortable signal that it is time to increase risk: that is, in order to consider adding more risk, we would want to see the 10-year portion of the curve plateau. Overall, investors should aim to preserve the purchasing power of their portfolios, building upon the ‘real concept’, and searching for additional sources of diversification in real and alternative assets. The aim of the game is to think hard about what risk premia and valuations could look like at equilibrium in the new regime: the ones we’ve seen in the last 35 years or so are no longer available in the current state.

Andre, P. Pizzinelli, C. Roth, C, Wohlfart, J. (2022) Subjective models of the Macroeconomy: Evidence from Experts and Representative Samples, Review of Economic Studies, 0, 1-34.