Disclaimer1

In the US the probability of the Fed exiting its zero rate policy in a few years has been rising. This owes much to the Fed’s policy reaction function, and the stickiness of prices which allowed the Fed to lower real rates by cutting nominal rates, thereby boosting the economy. In addition, we can point to two more prerequisites. First, in the US, well-functioning capital markets provide risk money. When interest rates declined, money poured from bond markets into capital markets. Second, when the Fed introduced its zero rate policy, inflation expectations in the US remained slightly below 2%.

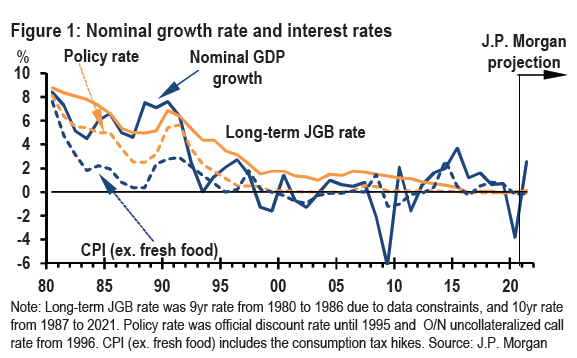

In Japan, the BoJ has had an almost-zero rate policy since 1995 (Figure 1). Powerful deflationary/disinflationary forces and policy rates at the effective lower bound have persisted for more than 20 years, much longer than is typically contemplated in economic analysis. When Kuroda’s BoJ innovatively introduced QQE in 2013, the BoJ tried to raise inflation expectations in an attempt to boost growth and exit persistent deflation, raising inflation to the target. It failed. The BoJ failed to raise inflation expectations and lower real rates persistently because it was constrained by rates at the effective lower bound (ELB) and underestimated the negative impact of the consumption tax rate hike, thus could not respond forcefully enough to inflation disappointments. As a result, markets lost confidence in the BoJ’s ability and commitment to reach the inflation target. As a consequence markets now believe that the BoJ will conduct LULY (low-for-ultra-long yield) policy, longer than other DM CBs. With Japan’s low growth expectations and weak corporate productivity performance in mind, whether this policy stance can contribute significantly to achieving the 2% target is the main focus of this note.

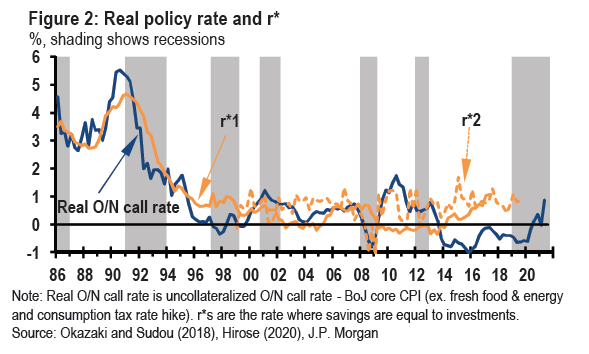

We start by assessing the effectiveness of the BoJ’s easing policy. We assess the degree of monetary easing by the difference of the real policy rate (r) and the natural rate of interest (r*) taking into account the difficulties in estimating r* (Figure 2). After the burst of the asset price and credit bubble in 1990, the BoJ continued to ease, and generally r was lower than r*. That said, there were two phases of financial tightening: In 1995 when the BoJ first shifted the policy rate to the O/N uncollateralized call rate and cut rates to almost zero (0.5%) but the yen appreciated rapidly, and in 2000 and 2001, when the BoJ lifted the true zero rate policy (2000) but faced the burst of the global IT bubble and shifted to QE (2001). On the other hand, during the domestic banking crisis in 1997 the BoJ maintained accommodative financial conditions. Core CPI inflation (excluding fresh food) dropped to zero at the end of 1990s, Japan slipped into deflation in the early 2000s (Figure 1), suggesting that the BoJ had not eased enough to counteract the deflationary shocks of the 1990s and prevent the slide into deflation. After that, facing the ELB, the BoJ lowered the long-term nominal interest rates through the CE (2010-) after the GFC when r clearly exceeded r*, followed by QQE (2013-), adding stimulative effects, which cannot be measured by a simple comparison of r* and r (see here ).

With QQE starting in 2013 the BoJ committed to doing whatever it takes to achieve the 2% target in two years. Though it succeeded in lowering r clearly below r*, given that it was constrained by the ELB, it still failed to respond aggressively to inflation disappointments. After that, the BoJ shifted from QQE to YCC to secure the sustainability of the easing, but did not ease further. This experience suggests that with both short- and long-term yields at zero it was very difficult to raise inflation expectations.

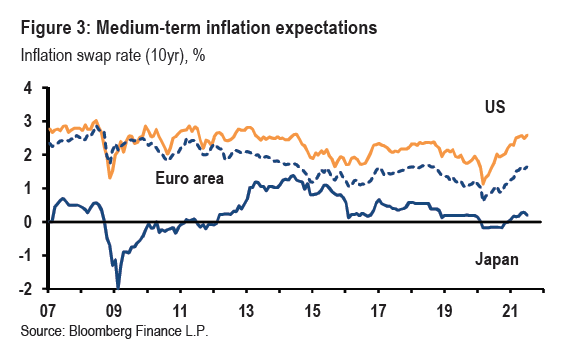

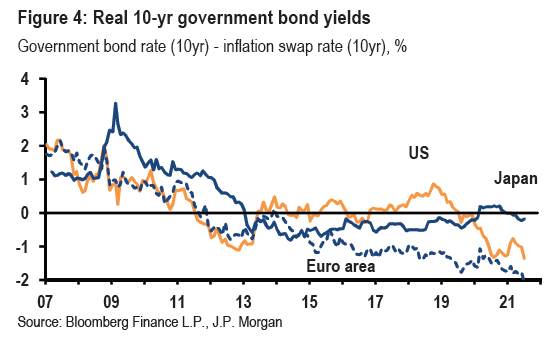

Partly because Japan’s inflation expectations was already at a low level when the BoJ adopted the almost zero rate policy and turned toward more pessimism thereafter, and because Japan’s inflation expectations are strongly backward looking, the policy’s impact on inflation expectations has been small except for 2013-15, when QQE sparked yen deprecation and the consumption tax hike raised prices (Figure 3). The real bond yield has been only slightly negative and not much below the low real return on capital, resulting in limited stimulus (Figure 4).

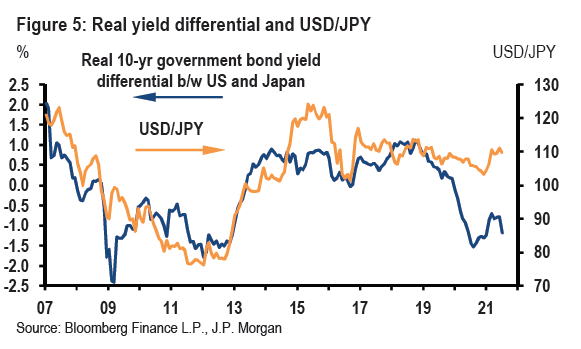

The influence of the monetary easing on the exchange rate is another channel to affect the economy. The real long-term yield differential between the US and Japan, usually affects the USD/JPY exchange rate strongly (Figure 5). This relationship and the steep drop in the US the real yield and Japan’s almost unchanged real yield since the start of the pandemic suggests significant appreciation pressure on the yen, which might force the BoJ to respond. However, fortunately, recently this relationship has not held, reflecting Japanese firms investing abroad and offshore investors selling of Japanese stocks on disappointment in Japanese firms (Sasaki, et al.). On the other hand, since Japanese households have a strong belief in the yen, there is no sign of broader capital flight or subsequent further yen depreciation.

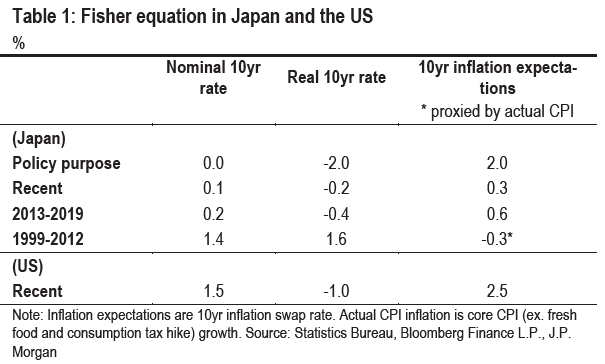

Let us compare the real rate and inflation expectations in Japan with those in the US (Table 1). The original purpose of the BoJ policy is that by maintaining the policy rate at zero, inflation expectations should rise to the 2% objective, while the real rate should decline to -2% to stimulate the economy and prices. However, since the BoJ adopted QQE and YCC, inflation expectations have turned positive but have not risen much, and the real long-term interest rate has not declined much. This is quite a contrast with the US, where the zero rate policy has succeeded in maintaining inflation expectations at over 2%, thereby decreasing the real rate to boost the economy. When this policy change is recognized as a decisive and limited-term action, people would not tend to store money and would invest more without lowering inflation expectations.

If the BoJ lowers the policy rate sharply, it could stimulate the economy, but we think the ELB constrains its ability to raise inflation. The existence of the reversal interest rate (the rate at which lowering the policy rate further becomes contractionary – around -0.5%) and of the likely threshold for depositors shifting from deposits to cash (-0.5% to -1.0% range), limits the size of possible further rate cuts.

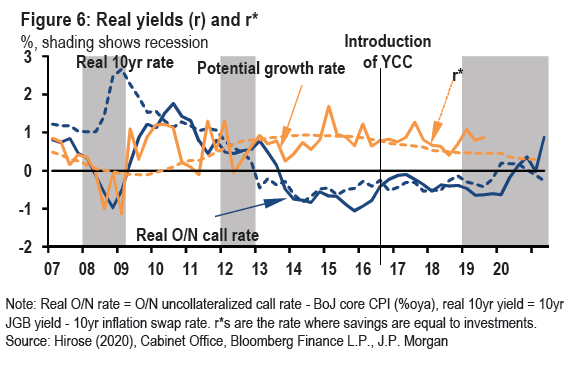

Then the next question is whether the continuation of the LULY policy would prompt a rapid economic recovery and raise inflation to 2%. First of all, the first-round impact of monetary easing in shifting demand from the future to the present likely has been exhausted over the past 20 years. Next, as Figure 6 indicates in more detail, while the BoJ has trouble lowering the real O/N rate and the real 10-year yield (r), Japan’s natural rate of interest (r*) where savings are equal to investments or its potential growth rate as the proxy of r* in the long run could decline further unless firms can be incentivized to reduce their savings and invest aggressively to raise productivity growth.

Fortunately, unlike the US, where r* is declining partly due to excess external savings in addition to the gradual decline in the potential growth rate, Japanese markets do not rely on foreign investors like US markets. As a result Japan has not experienced downward pressure on r* from external savings. However, if the potential growth rate declines further and negative shocks come, r* likely will also decline further. If this materializes, it would reduce the easing effect of monetary policy (r* – r), tightening financial conditions and lowering inflation expectations. Furthermore, simple continuation of the LULY policy with no prospect of achieving the 2% inflation target could further hurt the BoJ’s credibility, which would work against a possible rise in inflation expectations.

Of course, the strong global economic recovery and pent-up domestic demand backed by fiscal support can boost economic growth in the near future, but this should be transitory and inflation likely will remain subdued, different from in 2013-2015 when large fiscal spending and significant yen depreciation supported the Japanese economy and the yen depreciation and the consumption tax rate hike pushed up inflation expectations. The mobilization of excess corporate savings for investment would have a stronger impact on the economy, in our view. Below we look at potential options from this perspective.