This policy brief evaluates the effectiveness of central bank asset purchases in the euro area given their prominent role in ECB’s response to the pandemic as well as some evidence from the US suggesting potentially diminishing returns of this policy measure over time. Using a non-linear econometric framework, we find that the potency of ECB’s asset purchases to lift inflation has indeed considerably declined over time with several factors contributing to a more muted response of prices to central bank asset purchases. Our results show that their ability to influence inflation expectations has significantly weakened, leading to the dissipation of the reanchoring channel. On top of that, we detect the emergence of several disinflationary (side)effects, primarily stemming from the supply-side of the economy. In particular, QE-induced compression of borrowing costs has given rise to counterproductive effects via the cost and capacity utilization channels. Overall, our findings point to a diminishing returns of ECB’s asset purchases.

Central bank asset purchases, also known as quantitative easing (QE), have become a major monetary policy tool in plethora of advanced economies which is used to provide additional monetary policy accommodation against the backdrop of persistently low inflation and natural interest rates. Both phenomena contribute to longer and more frequent zero lower bound (ZLB) periods when standard monetary policy instruments are insufficient to bring inflation back to the target (Williams (2016), Kiley (2018)).2 In our study, we focus on the macroeconomic effects of the European Central Bank’s (ECB) large-scale asset purchases, which first introduced the Asset Purchase Programme (APP) in 2015 and further expanded its arsenal with the Pandemic Emergency Purchase Programme (PEPP) in March 2020 to counter pandemic-induced financial fragmentation risks and, ultimately, ensure price stability.

The existing empirical evidence, primarily emanating from the initial round of the APP, suggests that ECB’s asset purchases had successfully substituted the policy rate setting as it has largely been constrained by the effective lower bound. Literature suggests that the APP had significantly lowered borrowing costs for sovereigns as well as firms and households and generated favourable macroeconomic outcomes, significantly contributing to the ECB’s efforts in maintaining price stability (see e.g. Rostagno et al. (2019)). However, current literature on the ECB’ asset purchases lacks evidence on their non-linear or time-varying effects despite potentially diminishing returns over time (see Borio and Zabai (2016) for discussion on the US experience). This aspect, coupled with the prominent role of the PEPP in ECB’s response to the pandemic as well as the recent strategy review, prompted us to comprehensively (re-)evaluate the effectiveness of ECB’s asset purchase over time (see the Bank of Latvia working paper (Zlobins (2021)).

In order to pin down the macroeconomic impact of the ECB’s QE over time, we use a time-varying parameter structural vector autoregression with stochastic volatility (TVP-SVAR-SV) along the lines of Primiceri (2005) and perform identification via sign and zero restrictions of Arias et al. (2018).3

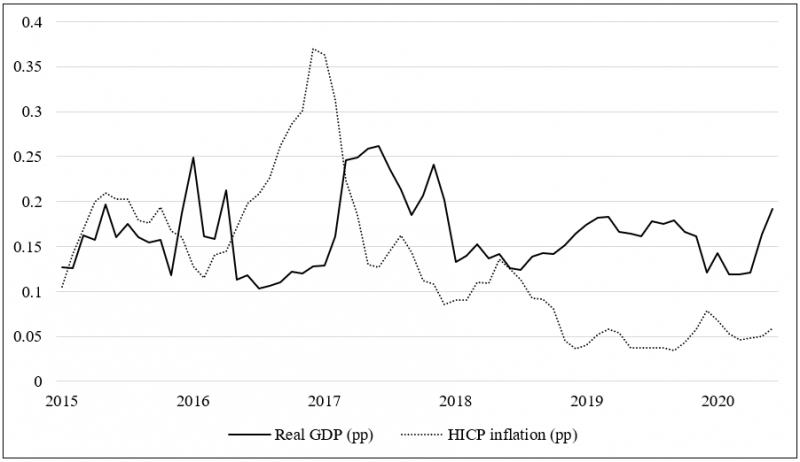

The results shown in Figure 1 suggest that the reaction of output to asset purchase shock has remained broadly stable over period from January 2015 to June 2020 but, strikingly, the response of inflation has considerably declined since 2018 onwards. It can be argued that this is a by-product of the Phillips curve flattening in the euro area, which is well documented in the literature, see e.g. Bobeica and Sokol (2019) and Eser et al. (2020). Both papers argue that the disconnect between slack reduction and inflationary pressures became particularly apparent from late 2017 onwards, which coincides with our results. Thus, our findings could imply that the effectiveness of asset purchases to lift inflation has not decreased over time, especially since their ability to reduce slack has remained intact, but they simply reflect an economic environment with a weak pass-through of costs to prices, which in turn is largely driven by factors outside the control of central bank.

Figure 1: Peak response of output and inflation to asset purchase shock (from January 2015 to June 2020)

Note: Figure shows peak impact from impulse response functions to asset purchase shock which has been normalized to a 1 pp increase in the Eurosystem asset holdings relative to 2015 nominal GDP (roughly 100 billion EUR) in each period, allowing the estimated elasticities to be comparable over time.

However, our analysis reveals that the observed decline in the response of inflation to large-scale asset purchases cannot be completely attributed to the recent Phillips curve flattening as we find that specific transmission channels of central bank asset purchases are no longer active in the euro area. On top of that, some disinflationary (side)effects have emerged from channels which have hitherto received little attention in the empirical literature on the ECB’s asset purchases. In particular, the results show that their ability to influence inflation expectations has significantly weakened from 2019 onwards, leading to the dissipation of the reanchoring channel (Andrade et al. (2016)), which was particularly relevant in the transmission of purchases made under the “first round” of the APP. Two other major transmission channels of asset purchases – portfolio rebalancing and signalling – have remained broadly intact over the sample, leading to a significant compression in funding costs. This, however has given rise to counterproductive effects via the cost channel mechanism (Barth III and Ramey (2002), Christiano et al. (2005), Ravenna and Walsh (2006)) as firms have used lower interest rates to cut their costs. Complementary to the cost channel, Boehl et al. (2020), studying the US experience, have identified additional supply-side mechanism through which large-scale asset purchases can have disinflationary effects. Namely, they argue that asset purchases predominantly boost investment with limited impact on private consumption, thus leading to the increase in the productive capacity of the economy and lowering prices pressures. We label this mechanism as the capacity utilization channel and empirically verify that this channel has recently emerged also in the euro area. We argue that the strong response of investment has been driven by QE-induced compression of borrowing costs, creating an incentive for firms to shift away from labour towards capital to reduce the wage bill, hence dampening private consumption and, consequently, generating counterproductive effects on inflation.

To sum up, this paper contributes to the empirical literature on macroeconomic effects of ECB’s large-scale asset purchases by exploring their non-linear effects over time. The evidence presented in this policy brief has important policy implications as they caution against systematic use of large-scale asset purchases to stabilize inflation and inflation expectations in the euro area as their effectiveness have significantly deteriorated over time.

Altavilla, C., Burlon, L., Giannetti, M., Holton, S. (2019). Is There a Zero Lower Bound? The Effects of Negative Policy Rates on Banks and Firms. ECB Working Paper, No. 2289, June 2019 (revised June 2020). 54 p.

Andrade, P., Breckenfelder, J., De Fiore, F., Karadi, P., Tristani, O. (2016). The ECB’s Asset Purchase Programme: an Early Assessment. ECB Working Paper, No. 1956, September 2016. 63 p.

Antolin-Diaz, J., Rubio-Ramirez, J. F. (2018). Narrative Sign Restrictions for SVARs. American Economic Review, vol. 108, No. 10, October 2018, pp. 2802–2829.

Arias, J. E., Rubio-Ramirez, J. F., Waggoner, D. F. (2018). Inference Based on Structural Vector Autoregressions Identified with Sign and Zero Restrictions: Theory and Applications. Econometrica, Vol. 86, issue 2, March 2018, pp. 685– 720.

Barth III, M. J., Ramey, V. A. (2002). The Cost Channel of Monetary Transmission. NBER Macroeconomics Annual 2001, vol. 16, January 2002, pp. 199-256.

Bobeica, E., Sokol, A. (2019). Drivers of Underlying Inflation in the Euro Area Over Time: a Phillips Curve Perspective. ECB Economic Bulletin, Issue 4/2019.

Boehl, G., Goy, G., Strobel, F. (2020). A Structural Investigation Of Quantitative Easing. De Nederlandsche Bank Working Paper, No. 691, August 2020. 49 p.

Borio, C., Zabai, A. (2016). Unconventional Monetary Policies: a Re-appraisal. BIS Working Papers, No. 570, July 2016. 49 p.

Christiano, L. J., Eichenbaum, M., Evans, C. L., (2005). Nominal Rigidities and the Dynamic Effects of a Shock to Monetary Policy. Journal of Political Economy, vol. 113, issue 1, February 2005, pp. 1-45.

Debortoli, D., Galí , J., Gambetti, L. (2020). On the Empirical (Ir)Relevance of the Zero Lower Bound Constraint. NBER Macroeconomics Annual, vol. 34, issue 1, pp. 141-170.

Eser, F., Karadi, P., Lane, P. R., Moretti, L., Osbat, C. (2020). The Phillips Curve at the ECB. ECB Working Paper, No. 2400, May 2020. 51 p.

Jarociński, M., Karadi, P. (2020). Deconstructing Monetary Policy Surprises – The Role of Information Shocks. American Economic Journal: Macroeconomics, vol. 12, issue 2, April 2020, pp. 1-43.

Kiley, M. T. (2018). Quantitative Easing and the “New Normal” in Monetary Policy. Finance and Economics Discussion Series of Board of Governors of the Federal Reserve System, No. 2018-004, January 2018. 40 p.

Primiceri, G. E. (2005). Time Varying Structural Vector Autoregressions and Monetary Policy. The Review of Economic Studies, vol. 72, issue 3, July 2005, pp. 821–852.

Ravenna, F., Walsh, C. E. (2006). Optimal Monetary Policy with the Cost Channel. Journal of Monetary Economics, vol. 53, issue 2, March 2006, pp. 199-216.

Rostagno, M., Altavilla, C., Carboni, G., Lemke, W., Motto, R., Saint Guilhem, A., Yiangou, J. (2019). A Tale of Two Decades: the ECB’s Monetary Policy at 20. ECB Working Paper, No. 2346, December 2019. 339 p.

Williams, J. C. (2016). Monetary Policy in a Low R-star World. FRBSF Economic Letter 23. 6 p.

Zlobins, A. (2020). ZLB and Beyond: Real and Financial Effects of Low and Negative Interest Rates in the Euro Area. Latvijas Banka Working Papers, No. 2020/06, December 2020. 40 p.

Zlobins, A. (2021). On the Time-varying Effects of the ECB’s Asset Purchases. Latvijas Banka Working Papers, No. 2021/02, October 2021. 47 p.

Contact: andrejs.zlobins@bank.lv. The views expressed in this policy brief are those of the author and do not necessarily reflect the views of Bank of Latvia.

Although a growing list of literature questions the empirical relevance of the ZLB (see Altavilla et al. (2019), Debortoli et al. (2020), Zlobins (2020)), suggesting that standard monetary policy tools are still effective beyond zero, Zlobins (2020) also shows that their ability to lift inflation is significantly weakened, thus requiring additional unconventional tools to ensure price stability.

In the working paper we show that our findings are robust also when using alternative identification strategies, namely via fusion of high frequency identification (HFI) with sign restrictions à la Jarociński and Karadi (2020) and a novel approach by merging HFI with narrative sign restrictions of Antolin-Diaz and Rubio-Ramirez (2018).