While the ECB is not allowed to monetise debt formally in the wake of the Covid-19 crisis, there seems to be some scope to do so, without fear of galloping inflation. It might even be needed to hit the inflation target.

I never thought one day I would actually be discussing something a “serious economist” (an oxymoron?) would turn away from in horror.

Mention Weimar Germany and Zimbabwe in the same sentence and you know what I am talking about: monetary financing of government debt.

For people not familiar with the concept this is when a central bank prints new money and basically hands it over to the government to spend, without the obligation to pay it back one day. Plenty of proposals have been floating around over the past few years and not all of them are actually feasible or permitted by the European Treaties.

Nevertheless, it is still worth looking at some of the alternatives and discussing the pros and cons in the wake of the Covid-19 health crisis that has hit the eurozone. With debt levels already very high in most member states lack the fiscal capacity to tackle this new deflationary shock. So why not create the means through the printing press?

The easiest proposals focus on the part of sovereign bonds currently held by the European Central Bank (for simplicity we will use the terms ECB and Eurosystem as substitutes).

Why not just eliminate this debt by replacing these bonds with a zero-coupon perpetual? This would give member states some breathing space and the capacity to spend more. But not so fast. The central bank is actually owned by the government (though there are a few cases where the ownership is mixed). And within the Monetary Union, governments receive dividends from their national banks, who in turn receive their share of the ECB’s profits.

A central bank’s profit derives from the difference in interest income on the assets it holds and the interest it pays on its liabilities. Banknotes by nature don’t carry an interest rate. The profit the central bank makes on this is called seigniorage. In normal times, a positive interest rate is paid on commercial bank reserves, which are a large part of the central bank’s liabilities. But now the ECB actually charges a negative interest rate on a big chunk of bank reserves. Therefore, they also contribute to net interest income. If the ECB exchanges interest-bearing debt on the asset side of its balance sheet with a zero-coupon perpetual, then, of course, the central bank’s profits will decline, which will result in lower dividends for the governments in the future. For most central banks in the Eurosystem, the dividends and taxes paid to the state are now around 0.1% to 0.3% of GDP.

What most people don’t realise is that there is already some mild form of debt monetisation. As a matter of fact, in the current public sector purchase programme, bonds on the ECB’s balance sheet that come to maturity are replaced with new bonds. As in practice, the ECB will buy the new bonds that the governments are raising to reimburse the central bank, it is pretty much as if the central bank is holding the debt permanently on its balance sheet. What’s more, the interest they pay to the central bank is, at the end of the day, partially given back as a dividend. This is, of course, the case as long as the interest paid on central bank liabilities is zero or lower.

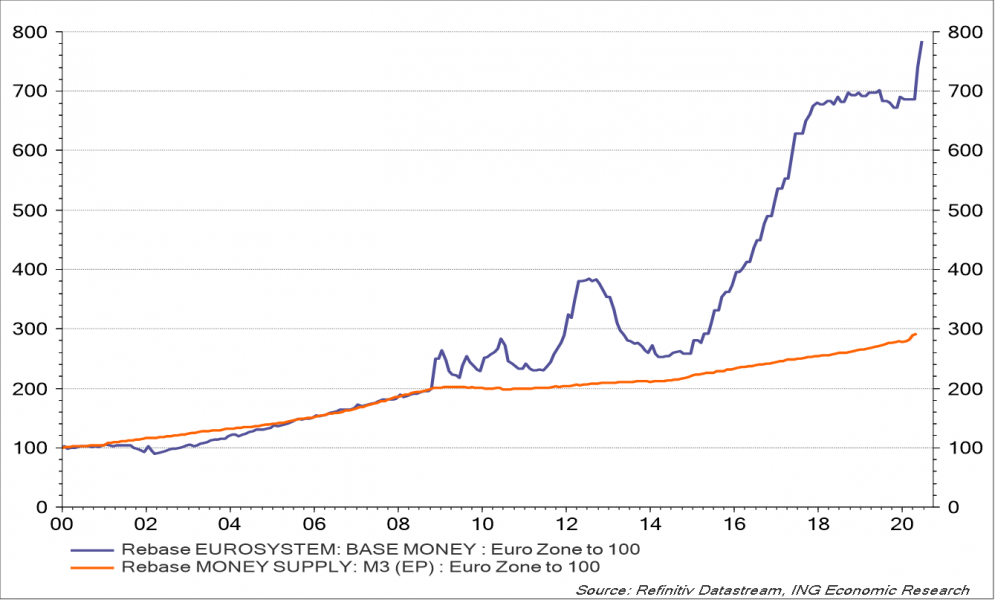

Graph 1: The money multiplier collapsed

So, in a nutshell, as long as the central bank rolls over its stock of sovereign bonds, there is nearly no difference with the situation where it replaces these bonds with a zero-coupon perpetual: this part of the debt is not reimbursed and comes at close to no interest cost. Admittedly, for the time being, there is no commitment to keep them indefinitely on its balance sheet.

Of course, the ECB could continue to expand its balance sheet by further buying sovereign bonds and refinancing these bond holdings forever. Actually, that is pretty much what happened during and after the Second World War. Major central banks substantially increased their balance sheets by purchasing government debt and while the balance sheets were mostly reduced afterwards in terms of GDP, they hardly ever did in nominal terms, as is explained here. In that way, it is believed that the Federal Reserve’s printing press financed about 15% of the war expenditures.

As the French President Emmanuel Macron compared the current Covid-19 crisis to a war-like situation, a case could be made for a permanent increase in the ECB’s balance sheet. The trouble is that monetary financing isn’t actually allowed under the EU treaties. Therefore, the ECB can use its balance sheet for monetary purposes, but can never commit to keeping government debt on its books indefinitely. The recent ruling of the German constitutional court is likely to draw even more scrutiny to the central bank’s policy in this regard. Of course, the ECB could do this by stealth. It doesn’t have to say overtly that it will continue to refinance government debt, but in practice, it could do so.

The only trouble here, a problem signalled by Adair Turner, is that the central bank might be too credible in its denial of monetary financing. In other words, the general public could believe that the debt in the hands of the ECB will have to be repaid someday, implying higher taxes in the future. That could lead to higher savings, and consequently less growth now (a phenomenon called Ricardian equivalence, if you want to impress your friends). So it is important that debt financing by the ECB is believed to be genuine in practice but non-existent in theory.

But wouldn’t this further increase in the size of the balance sheet lead to more inflation?

We already had a strong increase in the size of the balance sheet in previous years, not only in Europe but also in the US and Japan. The argument goes that more of this would push inflation through the roof. The reasoning behind this is to be found in the quantitative theory of money: the more money in circulation, the more inflation. What is lost in this reasoning, is that there is a difference between the money on the balance sheet of the central bank (base money, which equals notes in circulation and bank reserves) and broad money in the hands of the general public.

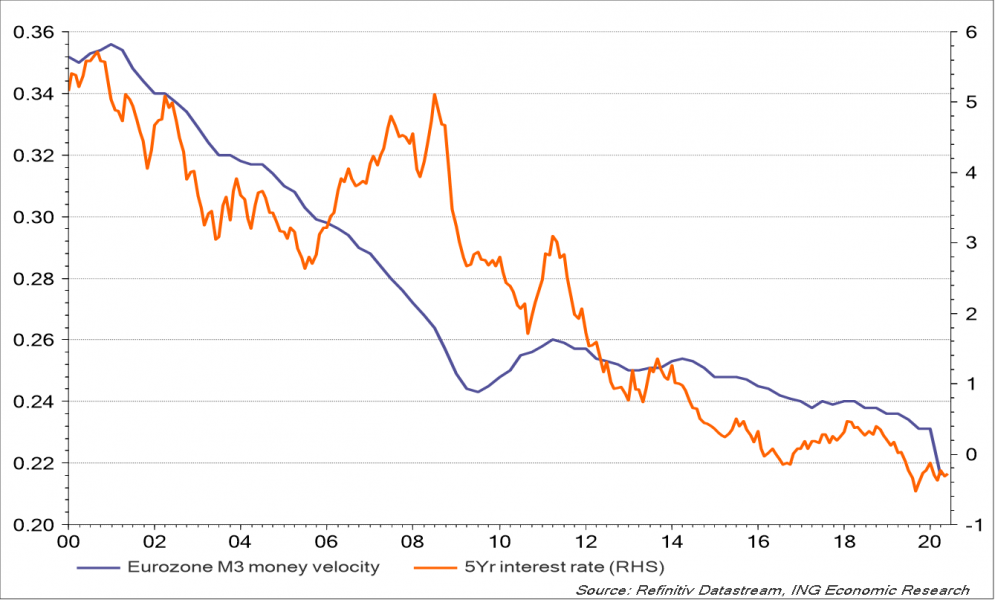

The money multiplier, which is the ratio of broad money to base money has actually collapsed. This is because quantitative easing directly creates broad money and bank reserves in similar amounts, but there is no extra money creation involved through bank credits in the process (see here for a detailed explanation). On top of that, the velocity of money, which measures the number of times the stock of money is used to do purchases during a certain time period, has also strongly declined. The latter is logical. As interest rates on alternative assets are very low, people hold a larger chunk of their wealth in the form of money, without actually using it to do transactions. To illustrate these points you only have to look at what happened in Japan over the last few decades. Since 1997, base money has increased by a whopping 970%, while consumer prices over the same period have basically remained unchanged. In other words, the increase in the ECB’s balance sheet through the purchase of additional government bonds doesn’t need to lead to significantly higher inflation, though of course the amount of government bond purchases without causing higher inflation, is not limitless either.

Graph 2: Declining velocity

You could even wonder if, at the end of the day, a little bit more inflation is not what the eurozone needs. Over the last 10 years, average inflation has been 1.3%, while average core inflation and the average GDP deflator came out at 1.1%. Nominal GDP growth, therefore, averaged a mere 2.5%. That is a worrying phenomenon since the real burden of large debt levels remains high, further depressing growth. With the current downturn creating a huge negative GDP output gap, some extra stimulus seems warranted, without immediately having to fear galloping inflation. And with short term interest rates already negative, the only tool the central bank has left to boost the economy further is balance sheet expansion. Since it is not obvious how to determine the exact amount of permanent balance sheet expansion, the central bank could announce a price level target in the future (see e.g. Bernanke), ideally one that allows for some correction of the inflation undershoot that we experienced over the last decade. The establishment and extension of the Pandemic Emergency Purchase Programme is already an important step in this regard, though at this moment the programme is still labelled as temporary.

The final question is whether the ECB, by monetising part of the fiscal expansion, would become hostage to the fiscal authorities. Fiscal authorities might want to prevent an interest rate increase because this would implicitly increase the cost on the debt held by the central bank (it would reduce the central bank’s interest income and thereby the dividends paid out to the governments), while at the same time, new debt would also have to be issued at a higher interest rate. And if the fiscal expansion to fight Covid-19 is now accommodated by the central bank, why couldn’t the same thing be done to finance the green agenda?

In that way, fiscal policy would become dominant, a thesis advanced by the proponents of Modern Monetary Theory: governments can spend newly created money as long as there is no full employment. Only when the situation of full employment is reached do governments have to hit the (tax) brakes to avoid inflation. However, past experiences of the central bank’s monetary policy being subordinated to fiscal policy did not end well.

A politician who needs to get re-elected is generally not the one who will “take away the punch bowl just as the party gets going”. That is basically the reason why most industrial countries have opted for an independent central bank that has to maintain the purchasing power of money in the longer run. But even when maintaining the dominance of monetary policy over fiscal policy, we believe that today, there is some scope to accommodate fiscal expansion by a further increase in the ECB’s balance sheet, without having to fear inflation going through the roof. At the end of the day, it might even be needed to bring inflation back to close to, but below 2%.

The article was also published in BFW digitaal / RBF numérique 2020/6.