This note provides a brief overview of the economic outlook faced by European SMEs and the financing markets most relevant to the European Investment Fund (EIF), the European Investment Bank (EIB) Group’s specialist provider of risk financing for entrepreneurship and innovation across Europe. It is based on the EIF’s European Small Business Finance Outlook (ESBFO),1 an annual publication that aims to inform policy makers, professionals and academics on recent trends on SME external financing markets in order to foster an informed public debate on SME financing to the benefit of European SMEs.

Recently, the outlook of the economic environment faced by European SMEs has worsened considerably, as a multitude of downwards risks are weighing heavily on global economic growth forecast. Global supply chain issues caused by the COVID-19 pandemic have proven more persistent than initially anticipated and have led to rising inflationary pressures around the world, mostly through increases in the price of international shipping and basic commodities. The Russian invasion of Ukraine has sent further shockwaves through global markets, severely affecting energy prices and adding to inflation, effectively bringing the post-pandemic recovery to a halt. Meanwhile, consumer confidence has sunk to a record-low level. In an effort to control price levels, the ECB has responded by drastically increasing interest rates. Combined, these factors indicate that a significant slowdown in economic growth is imminent. Consequently, the European Commission predicts the EU economy is likely to suffer through a technical recession during the first quarter of 2023.

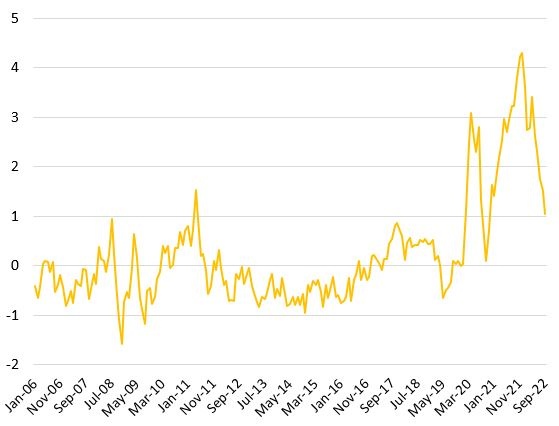

Global supply chain disruption index

Source: Federal Reserve Bank of New York

SMEs suffer disproportionally in the current economic environment. Compared to their larger counterparts, SMEs rely on less developed supply chain networks. Less substitution possibilities imply that shocks to global distribution channels typically have a more severe impact on their day-to-day business activities. In addition, due to limited availability of capital resources, SMEs are less likely to have invested in renewables or energy-efficiency projects, making their cost-structure more susceptible to shocks in energy prices. Finally, the rise in interest rates following the ECB’s consecutive rate hikes is likely to have a profound impact on SMEs’ financing conditions, by adding to the expense of bank lending and worsening the outlook of private equity funds’ fundraising and exit environment.

In the immediate aftermath of the pandemic, access to public financial support was an important positive driver of external financing availability, as the vast majority of European SMEs had access to government support schemes. These schemes mostly helped firms to finance working capital needs and meet their short- and medium-term obligations. Recently, however, pandemic support programs are gradually being terminated, potentially exposing vulnerable, yet viable SMEs to liquidity shortages, thereby heightening their risk of insolvency.

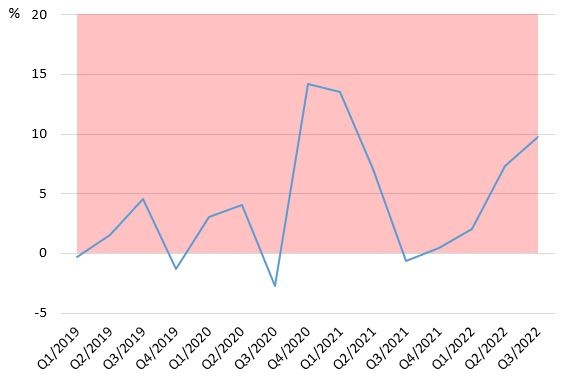

Bank credit standards applied to SME lending by Euro area banks*

*Net-percentages, calculated as the difference between the share of banks that tightened, minus the share of banks that loosened credit-standards. A positive value implies an aggregate tightening of credit standards.

Source: ESBFO, ECB BLS survey

Banks, traditionally the most important source of external financing for European SMEs, have again started to tighten SME credit standards, citing the [deterioration of the] general economic environment as the most important contributing factor (ECB, 2022),2 possibly anticipating a rise in loan defaults as a consequence of the current energy crisis.

While SME external financing conditions throughout 2021 remained relatively favourable by historic standards, the ECB SAFE survey revealed a deterioration during the first months of 2022. According to the data provided by the latest survey wave,3 administered at the onset of the Russian invasion of Ukraine, about 24% of European SMEs reportedly experienced severe access to finance issues, an increase of 2 percentage points compared to one semester earlier.4 SMEs cited the decline in public financial support for access to finance instruments as one of the drivers behind the deterioration of their external financing access

Percentage of SMEs reporting severe issues in accessing external financing*

*Ranking it 7 or more on a scale up to ten, when asked how pressing of a problem access to finance was in the six preceding months.

Source: ESBFO, ECB SAFE survey

SME financing conditions differ vastly between European countries. The share of SMEs experiencing severe financing issues ranges from just 15% in Finland, to over 40% in Greece. Compared to the same semester one year earlier, SMEs’ perception of their external financing environment improved in all countries but France.

The near-term risks to the economic outlook are on the downside. While gas prices have declined considerably in recent months, a colder than expected winter could reverse this trend and prevent inflation to return to the ECB’s target level. Individual country efforts, using subsidy-based instruments to compensate for rising energy prices, might invalidate the ECB’s actions, increasing the probability of additional rate hikes. In addition, rising geopolitical tensions could strengthen the trend towards deglobalisation and further threaten the functioning of global supply chains, whereby redesigning Europe’s industrial structures is likely to be associated with sizeable adjustment costs. Furthermore, China’s restrictive Covid policy and a slow-down in US economic growth are likely to negatively affect demand for European exports. Combined with plummeting consumer confidence, this will further weigh on near-term aggregate demand, and hence, economic growth.

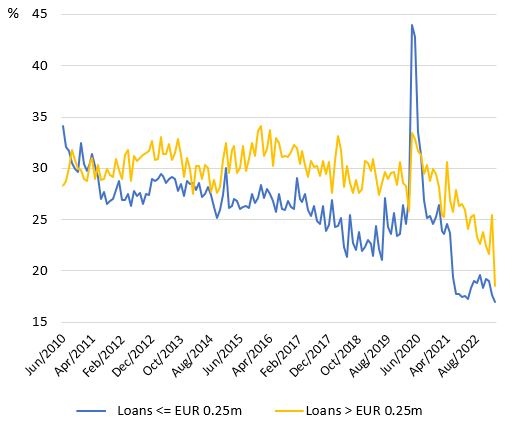

In the wake of the COVID-19 pandemic, government-backed Credit Guarantee Schemes contributed significantly to corporate liquidity support. In the immediate aftermath of the pandemic, activity on the bank lending market for loans backed by a guarantee or collateral spiked, in particular for loans smaller than EUR 0.25m. Recently, with support programs being gradually terminated, the share of guaranteed/collateralised loans plunged to just 17% in August 2022, falling well below its historic average. This trend initially appeared unique to the segment of small loans, but recently the share of guaranteed/collateralised loans also declined for larger loans.

Newly disbursed loans that carry a guarantee or collateral, by loan size

Source: ESBFO, ECB

While the data unfortunately do not allow distinguishing between guaranteed and collateralised lending, it is unlikely this declining trend is explained by a reduction in collateral requirements. Rather, given the rise in economic uncertainty, it is in fact more likely that banks have increased collateral requirements, implying a decline in the outreach of credit guarantee instruments is a more plausible explanation of the decrease in the combined category.

This conclusion is corroborated by evidence provided by AECM, whose data revealed a record seven-fold increase in the volume of newly granted government-backed credit guarantees during 2020, to EUR 280bn, followed by a significant decline to EUR 90.8bn for 2021.

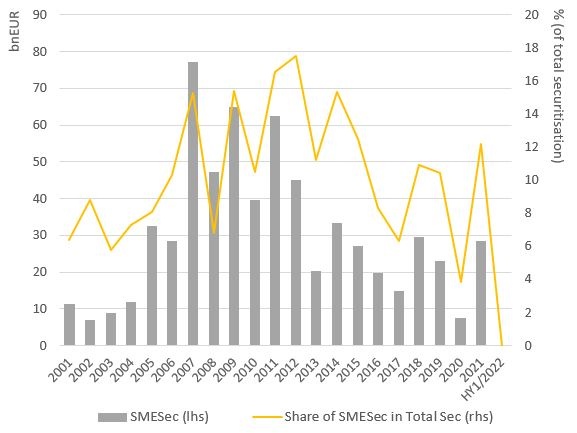

SME securitisation (SMEsec) provides an invaluable tool to enhance SMEs’ access to capital markets. In the aggregate, 2021 was a relatively good year for the European SMEsec market, as visible5 issuance increased significantly to EUR 28.4bn in 2021 (+279% year-on-year). However, this was driven by the largest single transaction in Europe ever (Best/Rabobank, EUR 16.6bn) and 2022 started slowly, with no visible issuance during the first semester.

The impact of the recent and ongoing economic crises on SMESec asset quality and deal performance remains to be seen, as well as the strength of structural protection and its ability to buffer adverse economic effects. The impact of the crises will vary by region, depending on many parameters like structure and flexibility of the economies (and the SMEs).

SMESec issuance in Europe (volume and % of total sec)

Source: ESBFO, AFME

Driven by investors’ demand as well as environmental risk aspects, sustainability considerations are gaining importance in securitisation – and in structured finance in general. The sustainable securitisation market is still in its early days, but has the potential to play a significant role in Europe’s green transition.

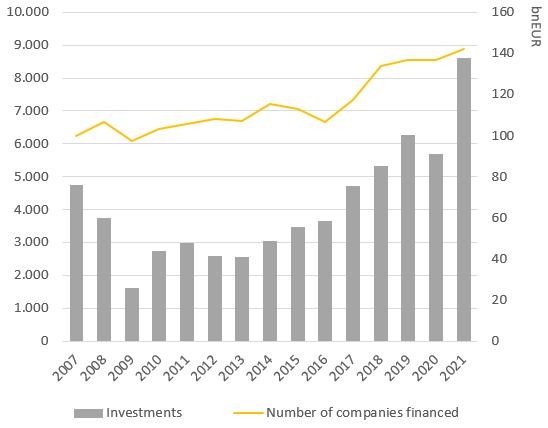

Private equity and venture capital (PE/VC) financing is the most important source of funding for innovative young and high-growth enterprises. The European PE/VC Ecosystem experienced a strong recovery in 2021, with PE/VC investment volumes in European companies increasing by 51%, the largest year-on-year increase recorded since 2010, settling at an all-time record of EUR 138bn (VC: +71%; Buy-out: +28%; PE Growth: +124%). Fundraising also reached new highs in 2021. Following a temporary setback during the midst of the first waves of the COVID-19 pandemic, total PE/VC fundraising recovered in 2021 and amounted to EUR 118bn. Preliminary evidence suggests that investment volumes in Europe remained relatively robust during the first semester of 2022.

PE/VC investment amounts in European portfolio companies*

*All investment figures are equity value, excluding leverage.

Source: ESBFO, Invest Europe

While 2021 has been a historic year for European PE/VC, the market faces significant headwinds for the near future. The uncertain geopolitical situation and rising rates are likely to present unprecedented challenges to fundraising and exits, which in turn will result in downward pressure on investee valuations. The 2022 EIF VC Survey6 indeed revealed that fund managers are getting increasingly concerned about the fundraising and the exit environment, in particular driven by macroeconomic and geopolitical developments.

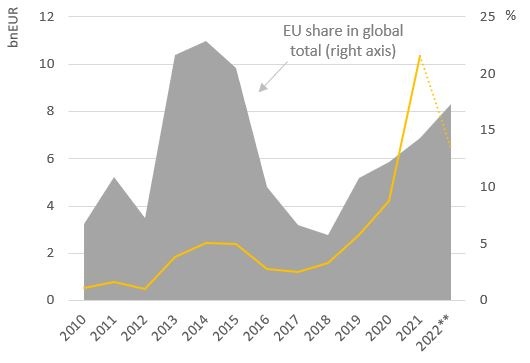

While the current economic situation is certainly a cause for concern, the energy crisis, as well as the recent European policy focus on sustainability and environment (through the European Green Deal), also present new opportunities for European PE/VC. Rising energy prices and an accommodating European regulatory framework have worked as a catalyst for EU Greentech investments. Consequently, funding volumes for EU Greentech companies have risen strongly in recent years. Over 2020, investments rose by 53%, significantly outpacing the aggregate market. Growth accelerated throughout 2021, as funding more than doubled, growing by as much as 145%. The data available at the time of writing indicate that Greentech market expansion is likely to slow down over 2022, although funding volumes are nevertheless expected to match those of 2021.

Funding volumes for EU Greentechs*

* VC + PE growth financing sourced from the Pitchbook database.

** Incomplete annual total at the time of data extraction (11/08/2022)

Source: ESBFO, Pitchbook

The geopolitical situation, lasting impact of the COVID-19 pandemic and current macro-economic environment are weighing on European SME finance conditions. The effects of the consecutive crisis events that are currently hitting Europe and the structural market failures that typically plague SME financing markets require continued, targeted and efficient support for European SMEs. Moreover, the long-term consequences of the significantly changing framework conditions for SMEs lead to the need of a long-term time horizon for the planning and preparation of support measures and strategic priorities in order to mitigate downside risks and to build on opportunities for the European SMEs.

In this challenging environment, the EIF is committed to fulfil its role as a counter-cyclical finance provider, through intermediated support to Europe’s small and medium-sized enterprises, starting from the pre-seed, seed-, and start-up-phase (technology transfer, business angel financing, microfinance and early-stage VC) up to the growth and development stage (formal VC funds, mezzanine funds, debt funds, and portfolio guarantees/credit enhancement). In the areas of credit guarantees and securitisations, the EIF cooperates with a wide range of financial intermediaries, such as banks, micro-finance providers, leasing companies, guarantee funds, mutual guarantee institutions, promotional banks and debt funds, thereby ensuring a sufficient supply of debt not only in times of crisis but also in order to mitigate structural market weaknesses. Moreover, in the area of PE/VC financing, the EIF will continue to provide support to Europe’s most innovative enterprises and tech champions of tomorrow, while private appetite for risk finance is weighed down by an environment of rising interest rates.

In addition to the acute pandemic and geopolitical crisis situations, the climate emergency is growing more pressing with every passing year. In support of the European Green Deal, the EIB Group’s Climate Bank Roadmap outlines the EIF’s role as a catalyser for private climate and environment finance. SMEs will play an important role in Europe’s quest to carbon-neutrality. SMEs and enterprises in the EIF’s portfolio have been contributing to the EU’s drive for resource efficiency and green transition for many years. The continued development of finance products that support the green transformation will be among the key business development priorities of the EIF in the year ahead.

Kraemer-Eis, H., Botsari, A., Gvetadze, S., Lang, F. and Torfs, W. (2022). European Small Business Finance Outlook. EIF Working Paper 2022/84. EIF Research & Market Analysis. November 2022. https://www.eif.org/news_centre/publications/EIF_Working_Paper_2022_84.htm

ECB (2022). Bank lending survey. Survey Results 2022 Q2.

Referred to as HY2/2021 but administered during the first months of 2022.

Ranking it 7 or more on a scale up to ten, when asked how pressing of a problem access to finance was in the six preceding months.

The numbers presented in this section do not account for the synthetic securitisation market, which typically do not appear in the statistics.

Kraemer-Eis, H., Block, J., Botsari, A., Diegel, W., Lang, F., Legnani, D., Lorenzen, S., Mandys, F., Tzoumas, I. (2022), EIF VC Survey 2022: Market sentiment and impact of the current geopolitical & macroeconomic environment, EIF Working Paper 2022/82, https://www.eif.org/news_centre/publications/EIF_Working_Paper_2022_82.htm