Zooming out from Corona-related gyrations in equity markets we take a longer-term view on the interplay between equity risk premia and monetary policy in the euro area. We find that changes in equity prices during periods of accommodative monetary policy mainly reflected adjustments in risk-free rates and economic activity – rather than fluctuations in investors’ required risk compensation. Furthermore, the equity risk premium (ERP) appears to not have declined by much since the introduction of unconventional monetary policy and stands higher than prior to the Global Financial Crisis (GFC). Use of identified monetary policy shocks in fact points to insignificant effects of monetary policy on the ERP. However, a breakdown of these shocks reveals that monetary policy has a significant upwards impact on the ERP if the shock is perceived as a negative information surprise, while the opposite prevails in the case of a genuine accommodative monetary policy surprise. Accumulating these effects over time suggests that these two effects might have largely offset each other since the introduction of unconventional monetary policy.

Leaving aside COVID-19 related gyrations in equity markets, we note that equity prices in the euro area have risen since the announcement of the Asset Purchase Programme (APP) in early 2015, with stock price increases being stipulated to at least partially reflect changes in monetary policy. In principle, monetary policy can affect equity prices through three channels. The first is via risk-free interest rates, where equity prices increase, ceteris paribus, if – following a monetary policy easing – the risk-free interest rates used to discount future cash-flows to investors decline.2 The second channel is the impact of monetary policy on companies’ actual and expected earnings, and therefore on the level of future dividends and share buy-backs paid out to investors. A priori, the immediate effect of monetary policy on earnings expectations is unclear. While an easing of monetary policy should eventually have a positive impact on the macro-economy and therefore on earnings and dividends, the underlying reasoning provided by central banks for why such easing occurs – typically a worsening in the economic and inflation outlook – might lead market participants to revise their earnings expectations downwards. Finally, monetary policy might impact equity prices via the equity risk premium (ERP) – the expected excess return from investing in stocks over the risk-free rate – where the sign of the impact is a priori unclear and eventually is an empirical question.3

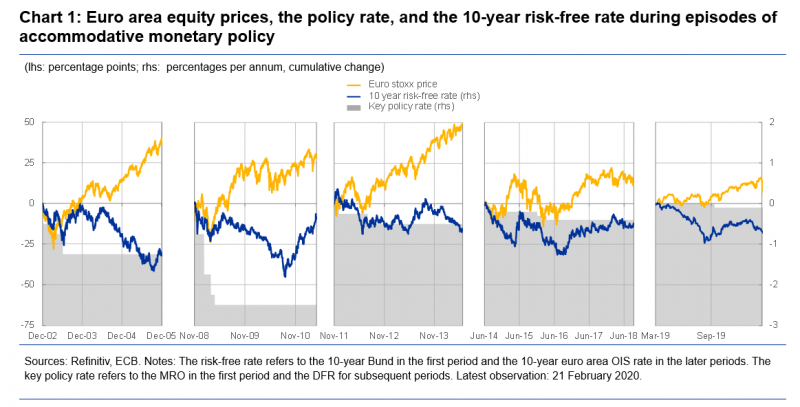

During past periods of monetary policy accommodation in the euro area risk-free rates tended to decline while equity prices increased (Chart 1). The chart shows five periods since the early 2000s, during which ECB policy rates were lowered. Although these episodes were characterised by different economic backgrounds and specific additional policy measures alongside the rate cuts, longer-term risk-free rates declined and equity prices rose during all of those periods.4

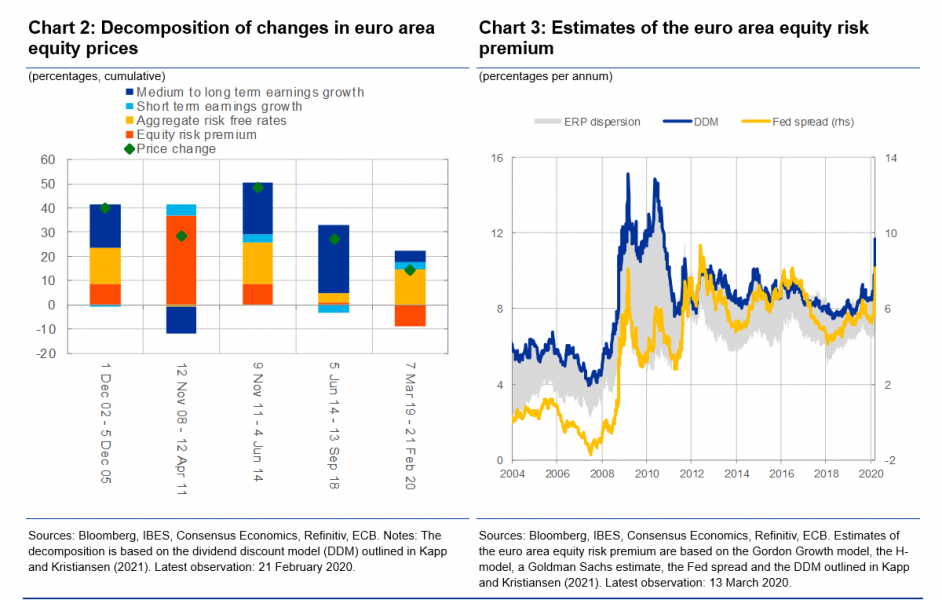

Except for the financial-crisis recovery, equity prices increased mainly on account of a decline in the risk-free rate as well as improvements in actual and expected earnings – rather than because of declines in the ERP (Chart 2). Using a dividend discount model5 to decompose the changes in equity prices reveals that declines in risk free rates and improvements in earnings and expectations thereof have typically accounted for the largest share of price increases for the episodes shown. The ERP, by contrast, played a relatively minor role. Hence, monetary policy easing during those periods is unlikely to have contributed to an ERP compression that has led to stretched levels of stock price valuations. An exceptional period is the marked recovery after the financial crisis peak, where the strong improvement in risk sentiment contributed to bringing back the ERP from its unprecedentedly high levels recorded during the crisis. While accommodative monetary policy certainly supported the improvement in risk-sentiment, it can also be attributed to targeted central bank and government interventions in the financial sector, such as large liquidity injections and the bail-out of a number of major global financial institutions.

Since 2014, the euro area ERP has been relatively stable at slightly above 8 percent, i.e. 2-4 percentage points above its pre-crisis level (Chart 3). That is, compared to pre-financial crisis averages ranging between 4% and 6%, investors currently demand a relatively high compensation for investing in equities instead of risk-free assets. Importantly, this result is not specific to the dividend discount model underlying the ERP estimate in Chart 3, blue line, but rather a common finding in the academic literature and across different estimation approaches (grey range).

The persistently elevated level of the equity risk premium is explained in the academic literature by market-specific factors and macroeconomic trends. Conceptually, the equity risk premium is the additional risk remuneration required by investors to hold equities instead of risk-free bonds over a certain investment period. The academic literature describes a number of potential reasons for why the ERP might have increased since the GFC. On the one hand, the literature points to higher risk aversion (as a persistent legacy of the financial crisis), and to concerns about increased downside economic risks.6 These factors might help explain both why risk premia have risen and why risk-free interest rates have fallen.7 In addition, a number of structural factors are argued to have increased the demand for safe assets over and beyond the demand for risky assets. These factors include changes in regulation, the savings glut, secular stagnation and the rise in global central bank reserves. Moreover, market segmentation and frictions that prevent or limit the stock market engagement of certain investor groups (e.g. pension funds), a limited participation in equity markets by the public (e.g. due to country-specific investment habits), as well as continued net issuance of equity throughout the post-QE period might have played a role. Finally, studies suggest that, while market participants rebalanced from shorter- to longer-term bonds in response to unconventional monetary policy easing, there is little evidence of rebalancing towards equities.8

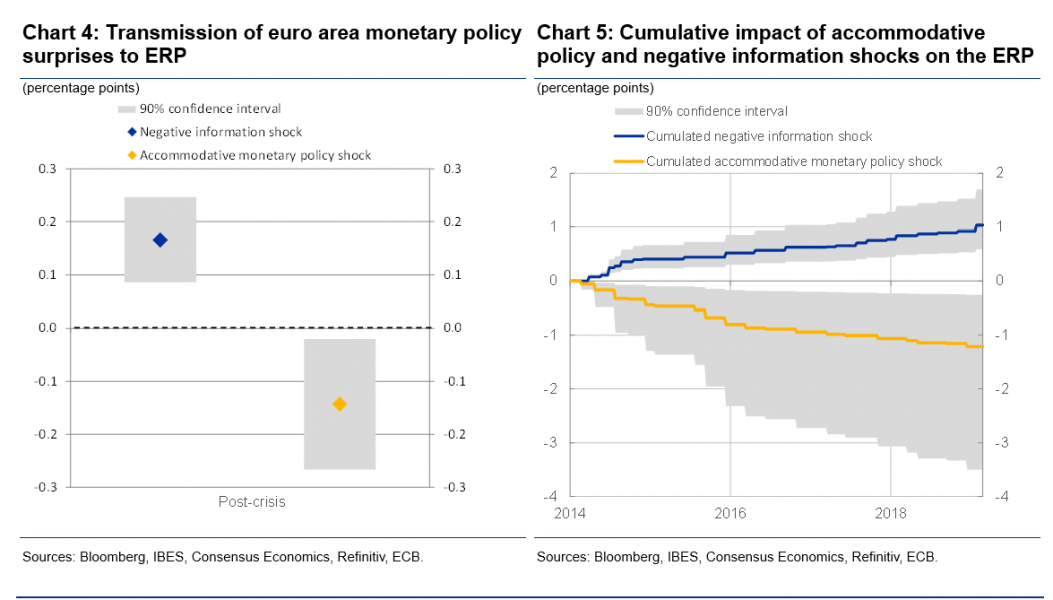

Monetary policy is also found to have an impact on the ERP, yet with opposite effects of “genuine” accommodative policy surprise shocks versus negative information shocks (Chart 4). To understand the reaction of the ERP to monetary policy surprises, it is important that genuine policy surprises (perceived deviations of interest rates from the policy rule) are separated from information effects (perceived new information signalled by the central bank on the current and future state of the economy). Following the academic literature, an accommodative policy surprise is identified via a contemporaneous decline in yields and an increase in inflation expectations. A positive information surprise is identified as a monetary policy event in the wake of which yields increase and shorter-term inflation linked swap rates increase at the same time.9 A priori, the reaction of the ERP to an accommodative monetary policy decision might be positive or negative, depending on the magnitude of the monetary policy surprise, and the perceived economic and inflation information being a positive or negative surprise to the market. Regression results suggest that the effect of accommodative monetary policy surprises on the ERP is negative, while the revelation of negative information concerning the state of the economy tends to increase the ERP.10 Accumulating the effects of genuine accommodative policy surprises and negative information effects suggests that the two effects might have largely offset each other since 2014 (Chart 5).

To ensure that results are not disproportionately dependent on the choice of the ERP approximation, we estimate the ERP using a number of alternative models. Although ERP estimates differ, regression results consistently suggest that identified pure accommodative monetary policy shocks entail a decline in the ERP, while negative information shocks are followed by an increase. Further, the impact of monetary policy shocks is roughly comparable across the German, French, Spanish and Italian stock markets.

Disclaimer: This policy brief should not be reported as representing the views of the European Central Bank (ECB). The views expressed are those of the authors and do not necessarily reflect those of the ECB.

For long rates to decrease after a policy rate cut or after forward guidance on keeping future rates low(er), it is necessary that term premia do not increase so much that they over-compensate the policy-induced decrease in average expected short-term rates. Empirically, as a general rule, this condition appears to be satisfied.

See Bernanke and Kuttner (2005), Jarocinski and Karadi (2018).

Concise dates and a more precise description of these periods can be found in the appendix of Kapp and Kristiansen (2021).

See ECB Economic Bulletin, Issue 4/2018 and Kapp and Kristiansen (2021) for a detailed description of the model.

See also Bernanke (2005), Lane and Schmukler (2006), Caballero et al (2008), Caballero, Farhi, and Gourinchas (2014), Gordon (2015), Lane (2019), Summers (2014), Summers and Rachel (2019), Norton and Philippon (2019), Blanchard and Giavazzi (2005), Daly (2016), and Kedan and Ventula Veghazy (2018).

See Broadbent (2014, 2019).

See Bua and Dunne (2017), who find that, in response to the PSPP, investment funds do rebalance into longer-term maturities, but not towards equities.

In order to examine the impact of monetary policy on the ERP more generally – for both accommodative and contractionary monetary policy actions – we first follow Gürkaynak, Sack and Swanson (2004), Jarocinski and Karadi (2020) and Altavilla, Brugnolini, Gürkaynak, Motto and Ragusa (2019) for the identification of monetary policy shocks. In this first step we calculate a monetary policy shock (MPS) series in line with Gürkaynak, Sack and Swanson (2004), where monetary policy shocks are estimated by calculating principal components from the change in yields around monetary policy announcements, i.e. the change in the first principal component. Subsequently, we follow Jarocinski and Karadi (2020) and Altavilla, Brugnolini, Gürkaynak, Motto and Ragusa (2019) and partition monetary policy shocks into central bank information shocks and ‘pure’ monetary policy shocks by applying a sign restricted BVAR to the shock series derived under step one, and adding daily changes in euro area Inflation Linked Swaps (ILS) rates to the model.

This is in line with the intuition outlined in Daly (2016) and Broadbent (2019), and consistent with the empirical results on equity prices in Altavilla et al. (2019). In this respect, Cieslak & Schrimpf (2019) argue and confirm that central bank announcements, mainly in the form of information shocks, can directly affect market participants’ risk sentiment.