References

Adalid, R., Falagiarda, M., and Musso, A. (2020). Assessing bank lending to corporates in the euro area since 2014. ECB Economic Bulletin, 1/2020.

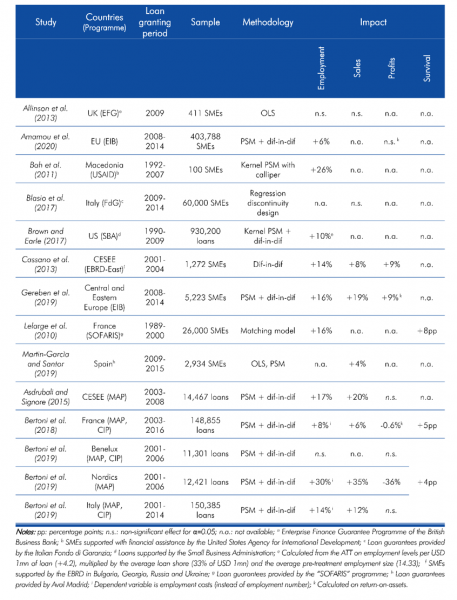

Allinson, G. F., Robson P., Stone, I. (2013). Economic evaluation of the Enterprise Finance Guarantee (EFG) Scheme. Department for Business, Innovation and Skills Project Report.

Amamou, R., Gereben, A., and Wolski, M. (2020). Making a difference: assessing the impact of EIB’s funding to SMEs. EIB Working Paper.

Ashenfelter, O. (1978). Estimating the effect of training programs on earnings. The Review of Economics and Statistics, 60, 1. pp. 47-57.

Asdrubali, P. and Signore, S. (2015). The economic impact of EU Guarantees on credit to SMEs. Evidence from CESEE countries. European Commission’s European Economy Discussion Paper 002 and EIF Working Paper 2015/29. July 2015. http://ec.europa.eu/economy_finance/publications/eedp/pdf/dp002_en.pdf and http://www.eif.org/news_centre/publications/eif_wp_29_economic-impactguarantees_july15_fv.pdf

Bah, E., Brada, J.C., Yigit, T. (2011). With a little help from our friends: The effect of USAID assistance on SME growth in a transition economy. Journal of Comparative Economics 39, 205–220.

Beck, T., Klapper, L. F., & Mendoza, J. C. (2010). The typology of partial credit guarantee funds around the world. Journal of Financial Stability, 6(1), 10–25. https://doi.org/10.1016/j.jfs.2008.12.003

Bertoni, F. and Colombo, M. G. and Quas, A. (2018). The effects of EU-funded guarantee instruments on the performance of Small and Medium Enterprises: Evidence from France. EIF Working Paper 2018/52, EIF Research & Market Analysis. November 2018.

http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_52.htm

Bertoni, F. Brault, J. and Colombo, M. G. and Quas, A. and (2019). Econometric study on the impact of EU loan guarantee financial instruments on growth and jobs of SMEs. EIF Working Paper 2019/54, EIF Research & Market Analysis. February 2019.

http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_54.htm

Brault, J. (2019). L’impact des programmes européens de garantie de crédit. BSI Economics.

Brault, J., and Signore, S. (2019). The real effects of EU loan guarantee schemes for SMEs: A pan-European assessment. EIF Working Paper 2019/56, EIF Research & Market Analysis. June 2019. http://www.eif.org/news_centre/publications/EIF_Working_Paper_2019_56.htm

Brown, J. D., Earle, J. S. (2017). Finance and growth at the firm level: Evidence from SBA Loans. Journal of Finance, 72(3), 1039–1080.

Cassano, F., Jõeveer, K., Svejnar, J. (2013). Cash flow vs. collateral-based credit. Economics of Transition, Vol. 21, pp. 269–300.

Chatzouz, M., Gereben, A., Lang, F. and Torfs, W. (2017). Credit Guarantee Schemes for SME lending in Western Europe. EIB Working Paper 2017/02 and EIF Working Paper 2017/42. http://www.eif.org/news_centre/publications/EIF_Working_Paper_2017_42.htm

Gereben, A., Rop, A., Petriceck, M., and Winkler, A. (2019). Do IFIs make a difference ? The impact of EIB lending support for SMEs in Central and Eastern Europe during the global financial crisis. EIB Working Paper 2019/09.

Gereben, A., and Wolski, M. (2020). The impact of public sector lending to SMEs on employment and investment. Vox.eu.

Gobbi, G., Palazzo, F., and Segura, A. (2020). Unintended effects of loan guarantees during the Covid-19 crisis. Vox.eu.

Gopinath, G. (2020). Limiting the economic fallout of the coronavirus with large targeted policies. Vox.eu.

Lelarge, C., Sraer, D., Thesmar, D. (2010). Entrepreneurship and credit constraints: Evidence from a French loanguarantee program. In: Lerner, J., and Schoar, A., International Differences in Entrepreneurship.

Martin-Garcìa, R., Morán Santor, J., (2019). Public guarantees: a countercyclical instrument for SME growth. Evidence from the Spanish Region of Madrid. Small Business Economics. Manuscript submitted for publication.

OECD (2013). SME and Entrepreneurship Financing: The Role of Credit Guarantee Schemes and Mutual Guarantee Societies in supporting finance for small and medium-sized enterprises (Final Report).

OECD (2019). Financing SMEs and Entrepreneurs 2019. An OECD Scoreboard.

Rosenbaum, P. R., Rubin, D. BN. (1983). The central role of propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55.

Riding, A. L., and Haines, G. (2001). Loan guarantees: Costs of default and benefits to small firms. Journal of Business Venturing, 16(6), 595–612

Stiglitz, J., and Weiss, A. (1981). Credit rationing in markets with imperfect information. American Economic Review. 71(3).