This Policy Note asks whether central banks are too conservative investors. Since reserves are held for foreign exchange intervention, central banks have prioritised holding safe assets that are liquid in episodes of market turmoil. Moreover, reserves were historically small and have only recently become so large that they exceed what could plausibly be needed for intervention. Several governance factors that bias central banks toward being too conservative are identified. These include a principal-agent problem between the central bank and the Ministry of Finance; the need to ensure sufficient asset management experience among board members and the senior management; and a bias towards a steady stream of profits arising from the profit distribution rules. To offset these problems, governance changes may be necessary.

Central banks are becoming increasingly important investors. Before the crisis their balance sheets were typically small and their significance stemmed largely from their role as monetary policy makers. But sharp increases in their foreign exchange (FX) reserves and the fact that they are now active in many more market segments than before the crisis have boosted their prominence as market participants. Nevertheless, despite these developments, central banks remain conservative investors compared to pension funds and insurance companies in the private sector and to other public sector investors.

This SUERF Policy Note has two objectives. First, to discuss how central bank reserve management has evolved in recent decades and, second, to ask why central banks are so risk averse as investors and what can be done to make them less so. The thrust of our analysis is that central banks are likely to become more risk tolerant in the future.

Before proceeding, it is useful to note that central banks manage three different sets of assets: FX reserves (which have risen sharply in emerging markets following the Asian financial crisis at the end of the 1990s), pension fund assets and assets (largely fixed income assets) acquired as a consequence of Quantitative Easing, mainly in advanced economies. These assets serve difference purposes, have different liabilities associated with them and the investment styles applied to them vary. This Policy Note considers FX reserve management where central banks have considerable room in terms of diversification and investment across asset classes, regions and currencies.

Central bank FX reserve management practices have evolved considerably in recent decades. Historically, central banks did not invest in, or had negligible allocations to, corporate bonds, asset-backed securities, emerging market debt and equity. The bulk of their assets was held in cash, bank deposits and short-duration government bonds. On the investment side, they focussed on liquidity to be able to engage in FX intervention what that was needed.

The picture has now changed. Most notably, the FX reserves managed by central banks have grown to unprecedented levels: with USD 10.5 trillion of reserves, they constitute one of the largest institutional investor segments and their investment decisions can move markets. Following the adoption of Quantitative Easing (QE), they have intervened heavily in global markets with the explicit goal of keeping interest rates low to boost economic activity.

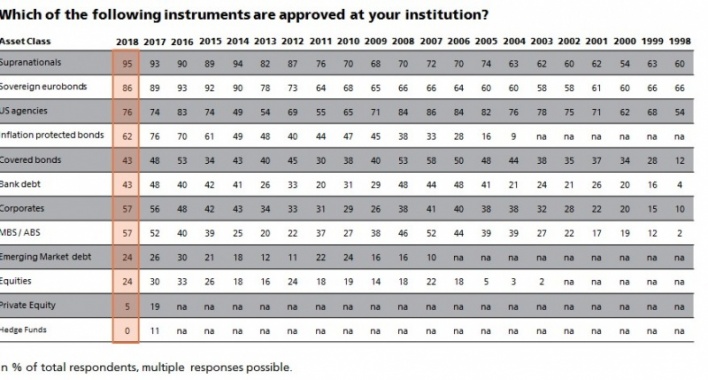

Graph 1 – Trends in Approved Asset Classes

Source: UBS Annual Reserve Manager Seminar, 2018

Today central banks invest across a wider range of asset classes, including spread products in fixed income markets such as corporate bonds and asset backed-securities and increasingly outside the fixed income space such as listed equity. According to the UBS Annual Reserve Manager Survey, more than half of central banks can invest into corporate bonds and asset backed securities and about a third can invest into emerging market debt and equity.

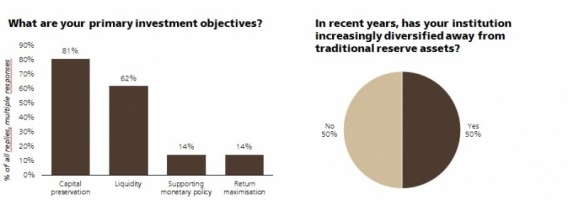

The primary objectives of central banks are capital preservation and ensuring liquidity, with the return objective important only as long as the two primary targets are fulfilled.

Graph 2 – Key Asset Allocation Objectives

Source: UBS Annual Reserve Manager Seminar, 2018

As noted above, the increasing diversification of the last two decades reflects the dramatic rise in FX reserves and the sharp drop in interest rates following the global financial crisis that prompted central banks to join other institutional investors in the “search for yield”.2 As a result of the extraordinary monetary policy measures launched by central banks to stave off the risk of deflation, nominal returns on cash and short duration government bonds across these markets have been very low since 2009. In 2009-2018YTD cash generated an average yearly return of 0.6%; the return on short-duration government bond portfolio was around 1%. A central bank’s portfolio invested across the major currencies in a 50/50 cash/short duration bond portfolio generated a return of 0.8% since 2009, well below the level of the previous decade (around 4%).

In this low interest rate environment, central banks have increased the duration of their government bond portfolios and broadened their investment universe to capture higher returns and to gain diversification benefits. Since 2009, investment-grade corporate bonds generated an annual return of nearly 5% and emerging market bonds in hard currency more than 5%. Global equity rewarded investors with an annual return of more than 9%. Over this period, a central bank portfolio with 60 per cent still invested into cash and short duration bonds and 40 per cent diversified into (investment grade) corporates, asset-backed securities, supranationals and long duration bonds generated a return of above 2 per cent, more than doubling the return of the cash/short duration bond portfolio and protecting the real value of the reserves. By diversifying even further into riskier asset classes, such as emerging market debt and equities, central banks were able to generate returns above 4%, thus fulfilling all their investment objectives of capital protection, liquidity and return enhancement.

Central banks’ asset allocations vary. Based on anecdotal evidence, central banks in the Americas and Africa appear most conservative with limited diversification within fixed income. They only rarely venture into riskier asset classes such as emerging market debt or equity.

In contrast, Asian central banks have diversified aggressively in recent years, reflecting the exceptional level of reserves, which are often well above the level considered as adequate for precautionary reasons. They often diversify into equities and some also invest in illiquid asset classes such as real estate.

European and Middle Eastern central banks stand in the middle between America and Asia but with a recent increasing trend towards more diversification, particularly into equities. There are some notable exceptions – for instance the Swiss National Bank which has a very high level of reserves and a relatively high allocation to equities.

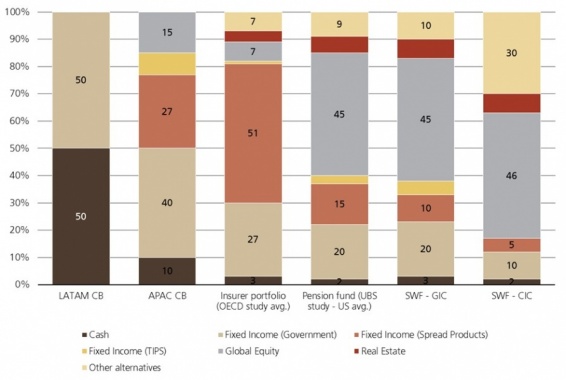

Despite the trend toward increased diversification, central banks’ investment profiles remain conservative in comparison to other institutional investors such as pension funds or insurance companies. The main differences are that central banks have small allocations to equities and almost no allocation to alternative asset classes such as hedge funds, real estate and infrastructure.

In contrast, pension funds generally invest 40% in equities and increasingly invest into alternative asset classes. Insurance funds hold mainly fixed income products for regulatory reasons, but nevertheless hold some equities and alternative asset classes.

When compared to Sovereign Wealth Funds (SWFs), the asset allocation of central banks appears to be even more risk averse, which is not surprising given the long-term investment horizon of these institutions and the fact that they have been created precisely to diversify reserves aggressively in global capital markets. However, it is also worth to note that some SWFs” assets are sometime managed by central banks, illustrating that central banks have the ability to manage highly diversified portfolios.

Graph 3 – Asset allocation of selected institutional investors

Source: UBS Asset Management, OECD

Following the introduction of QE, diversification has paid off as corporate bonds and equities produced good returns with low volatility. Will this trend continue in the post-QE era? Assuming that global growth continues and interest rates are gradually normalised, cash and short-duration government bonds are expected to generate returns in excess of 2% over the next five years. Global government bonds are expected to perform poorly as long-term interest rates rise from historically lows. Corporate bonds and other spread products are also likely to generate lower returns than in past decade as interest rate rises and spreads start from historical lows. Despite current high valuations in certain markets, global equity is expected to generate good returns, well above those in fixed income assets although less than during the last decade.

Should central banks further expand their investment universe as done by other institutional investors? From an asset allocation perspective, the case for adding alternatives to further diversify reserves is strong. Listed equity is attractive, but relative to fixed income and not in absolute terms, given the high level of uncertainty about future global growth in light of a potential negative impact of normalisation in policy rates and the gradual withdrawal of QE. Indeed, the likelihood of a slowdown or even recession in the US is rising.

The table in the appendix indicates how central banks” portfolios including selected alternative assets classes (real estate, hedge funds and infrastructure) would perform across these scenarios. In the base case, maintaining more than 50% of the portfolio to fixed income assets and adding 15% of alternative asset classes boost returns in both absolute and risk-adjusted terms. These selected alternative asset classes (private equity is excluded to reduce the reputational risk arising from investing into specific private companies) do not only provide a source of additional returns but also improve the risk return profile of the portfolio. In a recession scenario, returns are lower but still positive as the fixed income component of the portfolio compensates for the losses experienced in the riskier equity and alternatives.

Portfolios diversified into alternatives also perform better in a stagflation scenario. This is the worst scenario for those central banks which have diversified into equities as the traditional negative correlation between the returns on fixed income and listed equity would turn positive.

Overall, the case for further diversification including alternatives for central banks is strong particularly as the global economy is shifting to a new regime characterised by lower return on fixed income and higher volatility.

Why might central banks be such conservative investors? Traditionally, central banks operated with fixed exchange rates and needed foreign exchange reserves to deal with speculative outflows. Since pressures could develop very quickly and unexpectedly, the reserves were held in a highly liquid form so that they quickly could be used for intervention. In practice this meant that central banks held safe short-term USD treasury debt.

Two factors have reduced the relevance of this consideration. First, few central banks operate monetary policy with a fixed exchange rate. Under inflation targeting, in which the exchange rate only matters to the extent it risks pushing inflation away from the target, central banks’ need to hold foreign exchange reserves has been sharply reduced.

Second, foreign exchange reserves are now in many cases far larger than what could plausibly be needed for intervention. Following the Asian financial crisis, many central banks in emerging economies decided to increase their foreign exchange reserves to be better able to withstand occasional episodes of market pressures. This was all the easier to achieve following the onset of the financial crisis when central banks in advanced economies cut to, or below, zero and adopted unconventional monetary policy to provide further stimulus. This led to large inflows in many emerging economies that central banks often absorbed, increasing their reserves, to mitigate the upward pressure on their exchange rates.

The reduced need to hold foreign reserves for exchange market intervention coupled with the huge increase in reserves means that many central banks by now have become in all but name sovereign wealth funds. Nevertheless, they often retain their past investment strategies and focus on short-term liquidity rather than long-term capital returns.

Before proceeding, it is worth noting that central banks are better able to shoulder risk than private sector asset managers since they can operate with negative capital in an emergency. A financial firm that experienced large losses would soon find counterparties disengaging and customers withdrawing business, leaving the firm frozen out of the markets and unable to survive. Central banks, by contrast, are can always execute payments in domestic currency. Moreover, there are no legal reasons why insolvent central banks cannot continue to operate (as several have done), in contrast to private institutions that would be resolved in such a situation.

Nevertheless, central banks seem to be excessively risk averse. Three factors may play a role: there may be a principal-agent problem, the board that is responsible for setting the investment strategy and risk tolerance may lack investment expertise and experience, and profit distribution rules may reduce the scope for central banks to withstand losses.

6.1 Principal – agent problems

Excessive caution may reflect a principal – agent problem which arises because agent, the central bank, makes decisions on behalf of the principal, the government treasury. Such problems are common when the two parties have different interests and the agent has more information, so that the principal cannot be sure that the agent is acting in the principal”s best interest.

Since central bank profits reduce the need for treasuries to finance government expenditures by raising distortionary taxes, treasuries are naturally keen for the central bank to generate returns similar to those of private sector asset managers, which requires it to assume similar risks.

For the central bank, however, the risk-return trade-off may appear different. Reports of losses, even if rare and also experienced by private sector investors, may trigger press commentary arguing that the central bank is incompetent. Many central banks believe that the effectiveness of their monetary policy depends on them being seen as competent. Excessive media attention to occasional short-term losses is therefore undesirable. As a consequence, central banks may structure their portfolios to avoid such losses, at the cost of lower long-term profits.

6.2 Lack of investment expertise in central bank boards and senior management

Reputational considerations may matter to the central bank’s board and senior management. The board typically must approve the central bank’s investment strategy and determine its risk tolerance on the advice of the central bank’s senior management. Central bank boards typically consist of prominent members of society, drawn from the legal and accounting professions, academia, labour unions, or are retired politicians or civil servants. They have rarely expertise in asset management. This is often true also for members of central banks’ senior management.

Given the private reputational risks associated with presiding over a central bank experiencing losses on its investment portfolio and the associated risk to the credibility of the institution, it is not difficult to see that board members and members of the senior management will err on the margin of safety in establishing investment guide lines. As a consequence, the central bank may not seek to earn a market return on its foreign exchange reserves even if the treasury wishes it to do so.2

6.3 Profit distribution rules

Another factor that can lead central banks to be excessively cautious in managing their foreign exchange reserves is the profit distribution rules. These are typically set in central bank legislation and therefore not always easy to change. Uncertainty about the size of future profit transfers to the treasury is a problem for the fiscal authorities that must prepare long-term projections of government revenues. With distributions paid from current profits, central banks can come under pressure to ensure a predictable stream of income. This can lead central banks to holding relatively safe assets that generate small but sure returns.

To reduce the degree of risk aversion of central banks, governance changes may be warranted.

7.1 Clarifying the central bank act

Central bank boards and senior management may attach greater weight to the effects on their reputation and credibility of negative publicity arising from large losses on their portfolios, and may therefore adopt more conservative investment strategies than desired by their principals. This might be all the easier since central bank acts often provide no guidance about how funds should be invested.

An analogy to monetary policy may be helpful. It is generally agreed that inflation has been lower and more stable in recent decades because central bank acts were rewritten to clarify that price stability was a primary objective of policy. With a clear legal remit and political backing, central banks have been free to focus on this objective, achieving lower inflation.

Clarifying central banks’ investment objectives in legislation is therefore desirable. While it may be difficult to spell out the objectives in detail, phrasings such as “reserves not necessary for foreign exchange market purposes should be invested for long-term capital gain” or that “in managing its investments, the central bank should adopt principles similar to those of other long-term asset managers in the public and private sectors” might be helpful. This would provide legitimacy to the central bank’s asset management decisions and reduce the reputational risks of occasional capital losses.

From this point of view, the recent revision of the Guidelines for Foreign Exchange Management (IMF, 2014) was too cautious and a missed opportunity to upgrade the international standards of reserve management and to inject more focus on long-term returns. The revised guidelines also are weak in addressing procyclical portfolio behaviour, which is one implication of excessive risk aversion by central banks. Given the large pool of assets managed by central banks, their investment behaviour is likely to amplify market movements, particularly during periods of falling asset prices (Jones, 2018).

There are several examples of such investment behaviour by central banks. For instance, following the 2007-8 global financial crisis, central banks reduced by half their deposits with commercial banks, thus amplifying the liquidity crunch of the international banking system. During the euro-area fiscal crisis, several central banks cut their exposure to peripheral government bonds as credit rating agencies reduced the sovereign debt ratings of these countries. In these cases, other official institutions with a much more diversified asset allocation and low risk aversion, such as SWFs, adopted anti-cyclical investment behaviour. For instance, SWFs controlling another large pool of funds, bought equities when other investors were selling thus contributing to provide liquidity to the market.

In these cases, there was a clear conflict between the goal of central banks to maintain stability in the financial system during periods of financial stress and the pro-cyclical behaviour of central banks.

This conflict could resurface in the future. For instance, should inflation surprise on the upside and force central banks to tighten monetary policy by more than is currently expected, the impact on the government bond market could be large, tempting central banks to cut losses and shift assets into cash to protect their portfolios.

7.2 Governance and Investment committees

Another way to overcome the risk of an excessively cautious investment approach is to delegate decision making to an investment committee. Again, a comparison with monetary policy is warranted. While monetary policy decisions historically were taken by the central bank governor (unless the central bank lacked independence, in which case they were set by the minister of finance), in the last two decades Monetary Policy Committees (MPCs) have been increasingly adopted. The hallmark of these is that they have as members, appointed for 3-5 year terms, a combination of senior central bank staff and “outsiders” who are selected because of their expertise. As a consequence, monetary policy decisions are not in the direct control of the central bank.

The benefit of outsiders is that they may be less prone to group think that is always a risk in a central bank. While differences in remuneration levels between the public and private sectors may make it difficult to attract persons will asset management experience from the private sector to senior positions in central banks, a temporary appointment may be more attractive. Indeed, the Bank of England’s MPC often attract private sector economists.

In this regard, the experience of SWFs is important. The best run SWFs are those where the responsibilities of the sponsoring government, the principal, and the SWFs’ management, the agent, are clearly defined and separate. The principal is in charge of defining the risk and return expectations (which does not require it to provide guidance about individual asset classes, regions, etc.), while the agent manages the assets in discretionary way compatible with the chosen risk-return parameters.

7.3 Profit rules

Changing profit rules may also be helpful. Currently central banks typically repatriate some fraction of their annual profit to the Ministry of Finance. If the Ministry values a highly predictable stream, the result may be that the central bank aims for secure, but low, profits.

To avoid this, some device that allows the central bank to smooth profits over time might be helpful. For instance, the central bank could pay the annual profits into a buffer, held by the central bank (or perhaps even by the treasury itself or by a new institution), from which profits could be paid at a regular rate. An alternative might be for the central bank to pay out a fixed fraction – such as the expected return – of the portfolio. The pay-out rate could then be adjusted regularly in light of some objective criteria. This is effectively the logic followed by foundations, university endowments and SWFs.

Needless to say, any change of this type could have important legal and accounting implications that would need to be considered.

This paper has sought to shed light on whether central banks are too conservative investors. Central banks’ risk aversion – which exceeds that of most private sector, and other public sector, investors – is seen largely as reflecting historical circumstances. In particular, since reserves have been held to permit FX intervention, central banks have put a premium on holding safe assets that are highly liquid even in circumstances of market turmoil. Central banks’ reserves have also in many cases been relatively small and have only recently grown to such an extent that they exceed what could plausibly be needed for intervention purposes.

A number of institutional and governance factors that may bias central banks toward being conservative investors are identified. These include a principal-agent problem that can arise between the central bank and the Ministry of Finance; the need to ensure that board members and senior central bank management have sufficient asset management experience; and a potential bias towards a steady stream of profits arising from the rules determining the distribution of profits. To reduce the strong risk aversion, some governance changes may be necessary.

Overall, it seems appropriate for central banks to reconsider whether their current risk-return trade-offs are appropriate in light of the size of their reserves and to address any low risk bias identified, for instance by injecting more asset management expertise at the board and senior management level, set better incentives to resolve any principal-agent problem and improve governance on the investment side. The experience of SWFs, institutions created to accelerate the diversification of reserves, should be looked at by central banks, particularly with regards to their governance and ability to attract and retain financial expertise.

| CB1 | CB2 | CB3 | CB4 | CB5a | CB5b | CB5c | CB5d | ||

| Cash | 50% | 10% | 10% | 10% | 10% | 10% | 10% | 10% | |

| GGB 1-3 | 50% | 50% | 30% | 30% | 20% | 25% | 25% | 25% | |

| GGB | 10% | 10% | 5% | 5% | 10% | 5% | |||

| Corporate Bond | 10% | 10% | 8% | 8% | 8% | 5% | 6% | ||

| TIPS | 10% | 10% | 8% | 8% | 8% | 5% | 6% | ||

| Securitisied | 10% | 10% | 8% | 8% | 8% | 5% | 6% | ||

| Supranationals | 10% | 10% | 8% | 8% | 8% | 5% | 6% | ||

| EMD Hard Curr | 10% | 3% | 3% | 3% | 3% | 3% | |||

| EMD Local Curr | |||||||||

| Global Equity | 15% | 15% | 10% | 15% | 15% | ||||

| Real Estate | 0% | 5% | 5% | 7% | 8% | ||||

| Private Equity | |||||||||

| Hedge Funds | 0% | 5% | 5% | 5% | 5% | ||||

| Infrastructure | 0% | 5% | 5% | 5% | 5% | ||||

| Gold | |||||||||

| Commodity | |||||||||

| Total | 100% | 100% | 100% | 100% | 100% | 100% | 100% | 100% | |

| Yearly | |||||||||

| Return | 2.16% | 2.92% | 3.71% | 4.21% | 3.82% | 3.45% | 3.58% | 3.57% | |

| HISTORIC | Std Dev | 0.76% | 1.88% | 2.59% | 2.92% | 2.86% | 2.31% | 2.61% | 2.67% |

| Return/Std. dev | 2.85 | 1.55 | 1.43 | 1.44 | 1.34 | 1.49 | 1.37 | 1.34 | |

| Minimum rolling yearly Return |

0.22% | – 1.06% |

– 1.86% |

– 7.53% |

– 8.16% |

– 5.15% |

– 7.50% |

– 7.84% |

|

| BaseCase | GRR | 2.28% | 2.20% | 2.19% | 3.15% | 3.79% | 3.46% | 3.79% | 3.91% |

| Std Dev | 1.2% | 2.8% | 3.0% | 4.0% | 4.7% | 4.0% | 4.6% | 4.7% | |

| Return/Std. dev | 1.91 | 0.78 | 0.72 | 0.79 | 0.81 | 0.86 | 0.83 | 0.84 | |

| Recession | GRR | 1.5% | 2.6% | 2.8% | 2.2% | 1.9% | 2.1% | 1.9% | 1.8% |

| Std Dev | 1.2% | 2.1% | 2.2% | 3.5% | 4.8% | 3.9% | 4.9% | 5.1% | |

| Return/Std. dev | 1.31 | 1.27 | 1.29 | 0.63 | 0.40 | 0.55 | 0.38 | 0.36 | |

| Stagflation | GRR | 2.1% | 1.3% | 1.8% | 1.7% | 2.0% | 1.9% | 1.8% | 2.0% |

| Std Dev | 1.2% | 3.3% | 3.7% | 5.8% | 6.8% | 5.8% | 6.7% | 6.8% | |

| Return/Std. dev | 1.68 | 0.39 | 0.48 | 0.30 | 0.29 | 0.33 | 0.27 | 0.29 | |

| Productivity | GRR | 0.4% | 0.6% | 1.5% | 2.2% | 2.0% | 3.5% | 3.1% | 3.6% |

| Std Dev | 1.2% | 2.3% | 2.4% | 3.0% | 4.2% | 3.5% | 3.0% | 3.4% | |

| Return/Std. dev | 0.37 | 0.27 | 0.64 | 0.73 | 0.48 | 1.00 | 1.01 | 1.06 | |

GGB 1- is a short-duration government bond portfolio invested into USD (65%), EUR (25%), YEN (5%) and

GBP (5%); GGB is a long-duration government bond portfolio with the same currency breakdown.

Source: UBS Asset Management

Bank for International Settlements (BIS) (2011), Portfolio and Risk Management for Central Banks and Sovereign Wealth Funds, Proceedings of the Joint Conference organized by the ECB and the World Bank, Basel, 2-3 November 2010, BIS Paper 58.

Berkelaar, Arjan B., Joachin Coche and Ken Nyholm (2010), Central Bank Reserves and Sovereign Wealth Management, edited by Palgrave Macmillan.

Castelli, Massimiliano and Fabio Scacciavillani (2012), The New Economics of Sovereign Wealth Funds, Wiley Finance, United Kingdom.

IMF (2014), Revised Guidelines for Foreign Exchange Management.

Jeanne, Olivier and Romain Rancie re (2006), The Optimal level of International Reserves for emerging market countries: Formulas and Application, IMF Working paper WP/06/229.

Jones, Bradley A (2018), Central Bank Reserve Management and International Financial Stability – Some Post-Crisis Reflections, IMF Working Paper, WP/18/31.

UBS Asset Management (1998-2018), Annual Reserve Manager Survey.

Massimiliano Castelli, Managing Director, Global Sovereign Markets, UBS Asset Management; Stefan Gerlach, Chief Economist, EFB Bank and CEPR (corresponding author: stefan.gerlach@efgbank.com).

The views expressed in this article are those of the authors and do not represent those of the institutions with which they are affiliated.

Interestingly, the “global” financial crisis was in fact primarily focussed on the US and Europe.

This raises the issue of the appropriate degree of transparency in central bank asset management, an area in which practices vary across regions and countries. See IMF (2014) for a review of central banks’ transparency standards.