This Policy Brief is based on BIS Working Papers No 1126. The views expressed in this manuscript are those of the authors and do not necessarily represent the views of the BIS, the Banco de España, or the Eurosystem.

We analyze the implications of introducing a central bank digital currency (CBDC) for the operational framework of monetary policy and the macroeconomy as a whole. We develop a New Keynesian DSGE model with a detailed characterization of monetary policy implementation and we calibrate it to replicate the main monetary and financial aggregates in the euro area. While the introduction of a CBDC implies a reduction in banks’ deposit funding, the effect on bank lending to the real economy, and hence on aggregate investment and GDP, is rather small. This reflects the parallel impact of CBDC on the central bank’s operational framework. For moderate CBDC adoption levels, the reduction in deposits is absorbed by an almost one-to-one fall in reserves at the central bank, implying a transition from a ‘floor’ system–with ample reserves–to a ‘corridor’ one. For larger CBCD adoption, the loss of bank deposits is compensated by increased recourse to central bank credit, as the corridor system gives way to a ‘ceiling’ one with scarce reserves.

Central bank digital currencies (CBDCs) have received increasing attention in recent times, as central banks around the world consider issuing them.1 Academics and policy makers have focused on the implications of issuing CBDCs from a wide range of different perspectives: financial stability, monetary policy transmission, financial inclusion, currency competition, etc. Much less attention, however, has been devoted to their impact on the monetary policy implementation framework and how this is likely to shape the macroeconomic effects of CBDCs.

Nowadays, most central banks in advanced economies operate a “floor system” in which banks’ demand for liquidity is satiated with an ample supply of central bank reserves (“excess reserves”), and interbank market rates are effectively controlled by the interest rate on overnight deposits at the central bank. The introduction of a CBDC has the potential to affect the operational framework of monetary policy and the conditions in interbank markets if it brings about a sufficiently large decrease in excess reserves due to the reduction in bank deposits. This, in turn, may have important macroeconomic implications, both in the long run and in the transitional CBDC adoption phase.

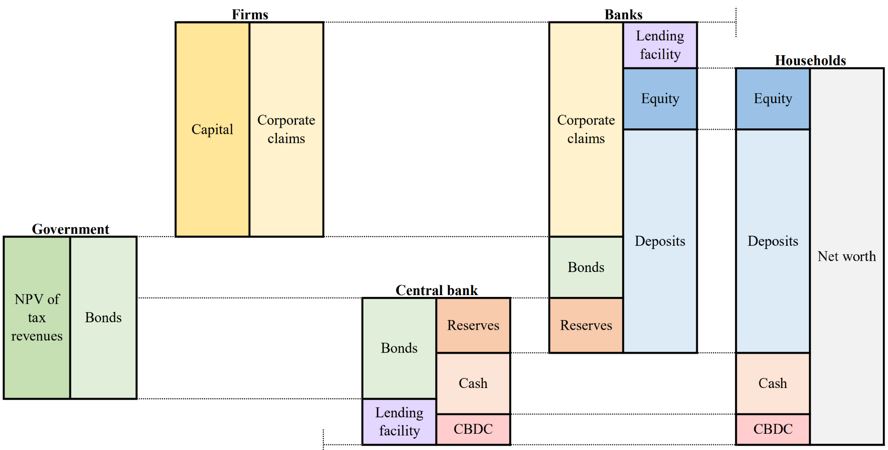

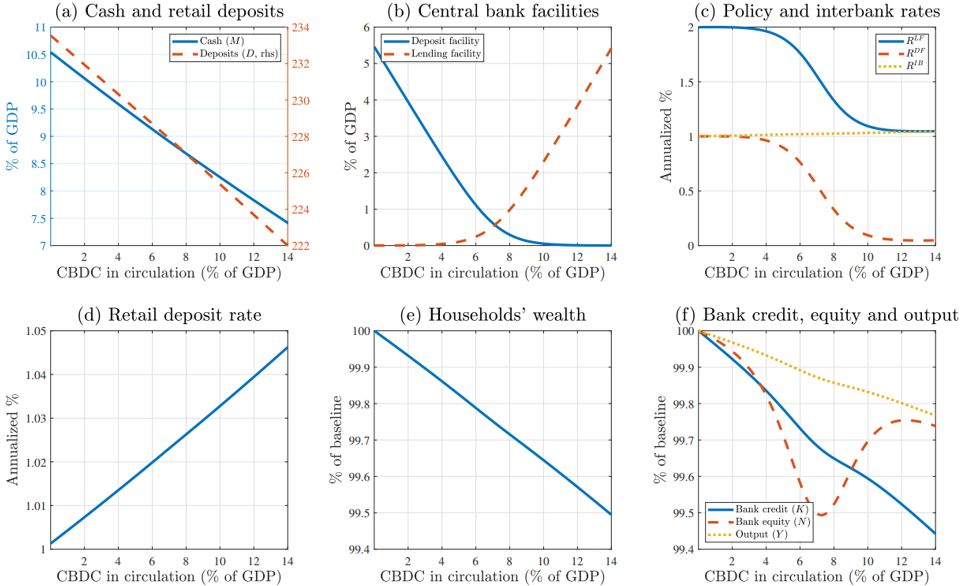

In a recent paper, we analyze the implications of the introduction of CBDC for the operational framework of monetary policy and for the macroeconomy as a whole (Abad, Nuño and Thomas, 2024). To this end, we introduce CBDC in a tractable New Keynesian model with heterogeneous banks, a frictional interbank market, a central bank that operates standing (deposit and lending) facilities, and household preferences for different liquid assets. Figure 1 presents an overview of the different agents in our model economy, the composition of their balance sheets, and how they are interrelated. We calibrate our model to the euro area, such that it replicates key features of the balance sheet of the Eurosystem and the consolidated commercial banking sector, as well as the relationship between aggregate excess reserves and money market rates. The core of our analysis is on the long-run effects of introducing non-remunerated CBDC. In particular, we perform a comparative statics exercise, summarized in Figure 2, in which we vary households’ long-run preferences for CBDC, effectively comparing steady states with a different equilibrium demand for this currency.

Figure 1: Balance sheets of the different consolidated sectors of the model economy

Our analysis predicts that households’ demand for non-CBDC liquidity (bank deposits plus cash) falls essentially one-for-one with CBDC demand, but the bulk of the adjustment (about three quarters) falls on bank deposits (Figure 2, panel a). Therefore, relatively large levels of CBDC adoption come hand in hand with a ‘deposit crunch’ on the banking sector. However, the latter does not imply a ‘credit crunch’: even large reductions in deposit funding have rather small effects on bank lending to firms, and therefore on productive investment and GDP (panel f). For instance, a level of CBDC adoption equivalent to 14% of GDP reduces bank deposits by 11% of GDP, but this lowers bank lending by less than 0.6% and GDP by barely 0.25%.

Figure 2: Steady-state endogenous variables as a function of the demand for CBDC

Note: Variables presented as “annualized %” refer to annualized percentage points; those presented as “% of GDP” refer to percentages of annualized output; and those presented as “% of baseline” refer to percentages of the corresponding value in the baseline model without CBDC.

At the core of the above result lies the impact that CBDC has on the central bank’s monetary policy operational framework. Our initial (no CBDC) steady state is consistent with the ‘floor system’ currently implemented by the ECB and other central banks in advanced economies, characterized by an ample supply of central bank reserves and interbank rates pushed against the remuneration of reserve deposits–the deposit facility rate (DFR) in the case of the European Central Bank or the interest rate on reserve balances (IORB) in the case of the Federal Reserve. For long-run levels of CBDC adoption below 4% of GDP, equivalent to CBDC holdings of about €1,900 per adult person, the reduction in bank deposits is essentially absorbed by an almost one-for-one fall in reserve balances at the central bank (panel b). This allows the banking sector to preserve most of its lending to the real economy despite the fall in deposits. For that range of CBDC demand, the floor system is preserved. As CBDC adoption goes beyond that level, some banks start borrowing from the central bank lending facility and the floor system is replaced by a ‘corridor system’, characterized by a low level of central bank reserves and interbank market rates standing around the midpoint of the interest rate corridor. For CBDC adoption levels exceeding 10% of GDP (equivalent to holdings of about €4,800 per adult person), there are no reserves left to absorb the contraction in bank deposits. Instead, banks replace the lost deposits–and thus continue to preserve most of their lending to firms–by increasing their recourse to the central bank’s credit facility. At those levels of CBDC demand, the corridor system gives way to a ‘ceiling’ system, characterized by scarce (in fact, zero) reserves and interbank rates pushed against the lending facility rate. The endogenous response of the central bank, by lowering its policy rate corridor when excess reserves start to become scarce and recourse to its lending facility increases, guarantees that banks are able to substitute their deposit funding with central bank credit without affecting their overall funding costs (panel c).

While small compared to its impact on the banking sector, the effect of CBDC on real outcomes is nonetheless far from negligible. In other words, CBDC is not neutral in the sense of Brunnermeier and Niepelt (2019) as it affects prices and macroeconomic aggregates. In our model, the non-neutrality of CBDC is a consequence of two different channels. First, there is a remuneration of households’ savings channel, by which demand for (non-remunerated) CBDC implies a lower average return on households’ optimal liquidity basket and hence a reduction in households’ savings (panel e). This leads to a decline in investment and physical capital, which reduces output and consumption. These effects are larger the larger the CBDC take-up is. Second, there is an operational framework channel, which becomes active when CBDC adoption is such that the operational framework transits to a corridor system. Under a corridor system, banks that borrow from the central bank’s lending facility do so at a higher cost than in the interbank market, and banks that lend their liquidity to the deposit facility receive a lower remuneration than in the interbank market. Both factors hurt overall bank profitability and hence bank equity, which in turn impairs bank lending, capital investment and GDP. This channel is not active when the central bank operates either a floor or a ceiling system, because in these cases the facilities are either accessed at market-neutral conditions (e.g. the deposit facility in a floor system) or continue to entail penalized access but are used only marginally (e.g. the lending facility in a floor system).

Brunnermeier and Niepelt (2019) analyze the equivalence between public and private money, in the sense that the introduction of CBDC has no macroeconomic impact as the loss in deposits by commercial banks can be compensated by direct lending from the central bank. This result does not hold in our model when CBDC is not remunerated, as discussed above, because the introduction of CBDC changes the average return on the household’s optimal liquidity basket. We show that, if CBDC is remunerated at an interest rate that does not alter households’ total savings decisions and CBDC adoption is such that the central bank operates either a floor or a ceiling system, then the introduction of CBDC has no impact on long-run prices or real macro aggregates. This equivalence result does not hold if the CBDC-induced reduction in excess reserves is such that the monetary policy framework shifts to a corridor system, because of the ‘operational framework channel’ described above. However, the macroeconomic impact is quantitatively small. Overall, our results suggest that the household savings’ remuneration channel is much more important than the operational framework channel at explaining the macroeconomic effects of CBDC in our model.

Abad, J., G. Nuño, and C. Thomas (2024). “CBDC and the operational framework of monetary policy,” CEPR Discussion Paper 18750.

Brunnermeier, M. K. and D. Niepelt (2019): “On the equivalence of private and public money,” Journal of Monetary Economics, 106, 27–41.

In March 2022, US President Biden’s Executive Order on Ensuring Responsible Development of Digital Assets placed “the highest urgency on research and development efforts into the potential design and deployment options of a United States CBDC”. Similarly, in October 2023 the European Central Bank (ECB) announced the start of the preparation phase of its ‘digital euro’ project, aimed at laying foundations for a potential euro-area CBDC.