We model mortgage refinancing as a bargaining game involving the borrowing household, the incumbent lender, and an outside bank. In equilibrium, the borrower’s ability to refinance depends both on the competitiveness of the local banking market and on the cost of switching banks. We find empirical support for the key predictions of our model using a unique data set containing the population of mortgages in Belgium. Households’ refinancing propensities are positively correlated with the number of local branches and negatively correlated with local mortgage market concentration. Moreover, households are more likely to refinance externally if they already have a relation with more than one bank, but the effect is mitigated if their current mortgage lender has a branch locally.

Why do so many households fail to refinance their mortgage when interest rates decline? Prior research trying to answer this question has largely focused on the drivers of the demand for refinancing, attributing household inaction to both behavioral or informational channels (Agarwal et al. 2016; Keys et al. 2016; Johnson et al. 2019). In a recent contribution to this literature, Andersen et al. (2020) empirically model the psychological and information-gathering costs associated with refinancing, and provide evidence that these costs may correlate systematically with borrowers’ demographic and socio-economic characteristics.

In recent work (Emiris, Koulischer and Spaenjers 2022), we take a different perspective and instead focus on the role of variation in the supply of refinancing options that households face. Our approach is motivated by growing evidence that, first, competitive frictions can affect households’ refinancing activity (Scharfstein and Sunderam 2016; Agarwal et al. 2022), and, second, households’ access to finance is shaped substantially by local banking and mortgage market conditions (Ergungor 2010; Scharfstein and Sunderam 2016; Célerier and Matray 2019; Buchak and Jørring 2021). If mortgage markets are local in scope, then households’ refinancing propensities and payoffs conditional on refinancing may vary geographically and over time as a function of both local competitive conditions and borrowers’ interactions with their local banking market.

Our conceptual innovation is to think of households as initiating a bargaining game as soon as they knock on their current lender’s door to ask for a refinancing. We build a simple multi-stage bargaining model in which the equilibrium offer that the incumbent lender does in the first stage will be a function of (i) the probability that the borrower gets an offer from a competing bank in a later stage, (ii) the cost for the borrower to switch from its current lender to another bank, and (iii) the relative cost advantage of the competing bank. If the net payoff for the borrower of switching banks is negative, the incumbent bank will refuse to refinance the mortgage. By contrast, if the borrower and the incumbent bank know that a competing offer would yield a positive payoff after accounting for the switching cost, the borrower will be able to refinance. Whether the borrower refinances internally (with the current lender) or externally (with a competing lender) depends on the relative cost advantage of the outside bank and on the switching cost.

We derive three sets of empirical implications from our model. First, both overall refinancing propensities and the relative share of external refinancing go up with the size and maturity of the mortgage. Moreover, the gross gains from refinancing externally should exceed those from refinancing internally. Second, if local bank competition rises, total refinancing activity—and, in particular, external refinancing activity—is likely to go up. Third, households with lower switching costs are more likely to refinance externally. Moreover, average realized gross gains conditional on refinancing externally will be lower for households with lower switching costs.

To test these predictions, we rely on a unique administrative data set containing all mortgages (and consumer loans) held by households in Belgium since 2006. The data set was provided to us by the National Bank of Belgium. In Belgium, mortgages account for the largest share of household debt, and primarily finance owner-occupied housing. About three quarters of 35-to-65-year-olds own their primary residence. A large majority of mortgages are originated by traditional banks through their branch network. Given the prevalence of fixed interest rate contracts and long maturities, the incentives to refinance tend to be substantial when interest rates fall. Yet, refinancing with a new lender is associated with substantial notary fees.

Our database contains information on more than 7 million mortgage loans (held at some point between 2006 and 2021) for close to 3 million different households. For each mortgage, we observe some basic loan characteristics, the location of the borrower, and the identity of the lender. Each borrower is associated with a unique anonymized identifier that allows us to observe any other loans taken out by the same household. We identify a refinancing as a loan issued in period t that replaces a loan with a similar amount outstanding in period t − 1. To make sure that we are capturing refinancing activity accurately, we exclude a number of specific cases such as borrower-year combinations associated with a move of the household, or borrowers that have mortgages with multiple banks.

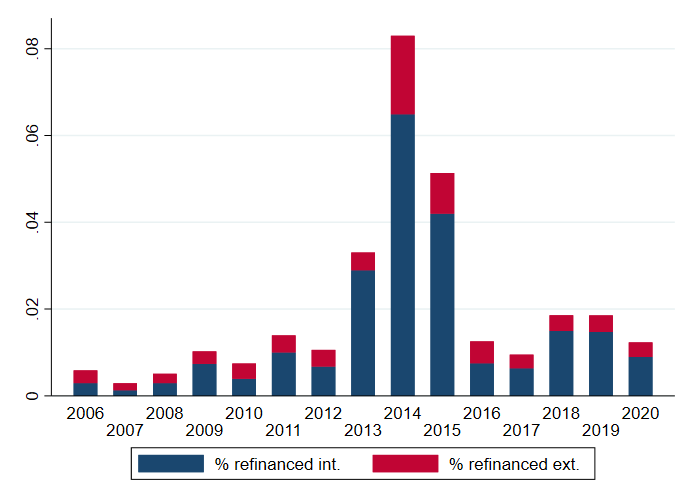

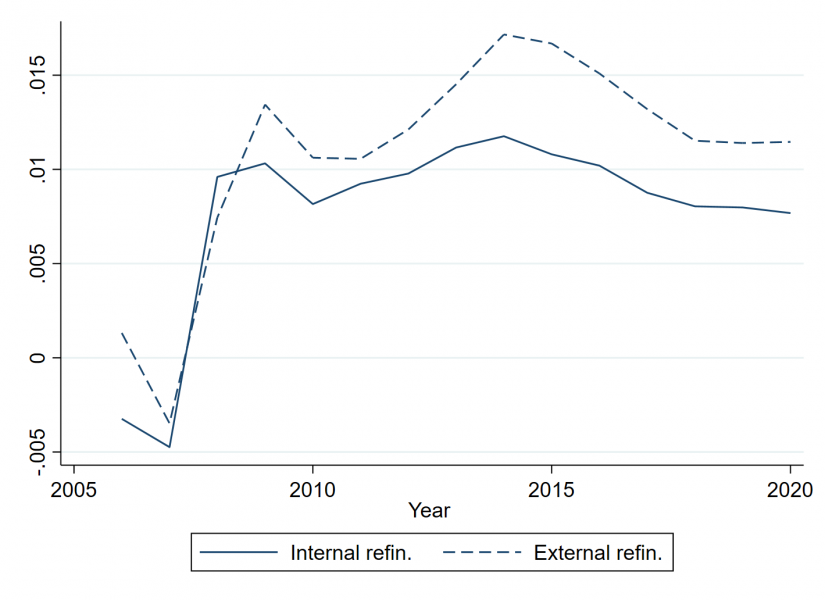

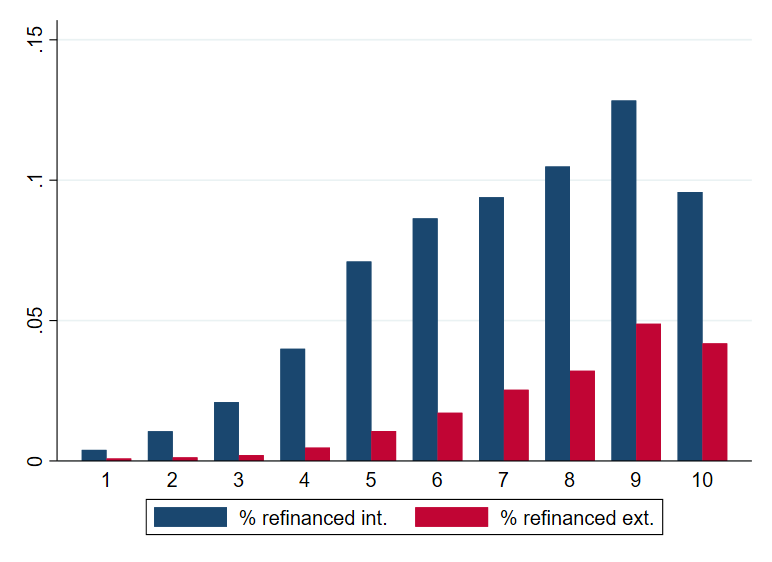

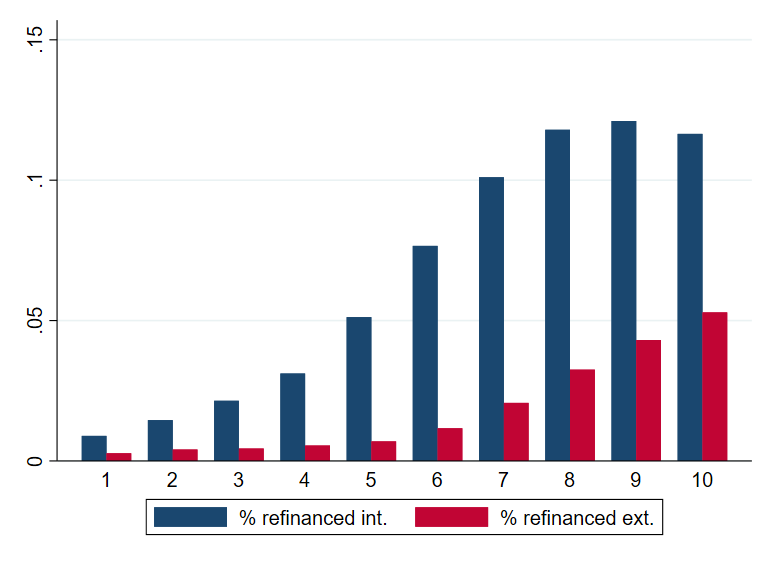

We find that refinancing activity varies strongly over time, with a peak in refinancing in 2015, when more than 8% of mortgages were refinanced (Figure 1a). Internal refinancing is much more prevalent than external refinancing, but households that refinance externally realize a higher decrease in mortgage interest rate (Figure 1b). Also the variation in the use of external refinancing is in line with the implications of our model. Namely, the propensity to refinance—in particular externally—increases with the remaining maturity (Figure 2a) and the outstanding loan balance (Figure 2b).

Figure 1: Refinancing activity and realized gains

(a) Fraction of active mortgages being refinanced in the next calendar year

(b) Interest rate differential on old vs new loans

Panel (a) of this figure provides an overview of refinancing activity over time, showing the share of mortgages outstanding that is refinanced in any given year, as well as the breakdown between internal and external refinancing. Panel (b) shows the yearly average difference between the interest rate on the initial mortgage and that on the refinanced mortgage.

Figure 2: Refinancing propensities in 2015 as a function of loan characteristics at the end of 2014

(a) Deciles of remaining time to maturity

(b) Deciles of estimated loan balance

Panel (a) of this figure shows the fraction of loans that are refinanced (overall or externally) in 2015, by decile of remaining time until maturity measured at the end of 2014. Panel (b) repeats the exercise by estimate loan balance and gross gain from refinancing.

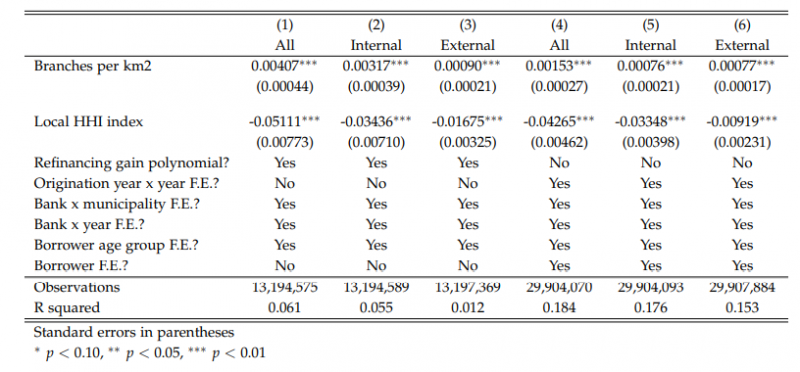

Next, we test whether bank competition affects refinancing activity, as our model predicts. We construct two historical measures of local banking market competition at the municipality × year level. Our first variable measures the number of bank branches per square kilometer. The second variable is a HHI-based measure of concentration based on outstanding mortgages. Our regression models include municipality × bank and bank × year fixed effects, so that identification is coming from local time-series variation in our competition variables. Our results are in line with expectations: refinancing activity is higher when local mortgage market competition is higher (Table 1). To mitigate worries that the local presence of banks may correlate over time with borrower characteristics that also drive refinancing, we repeat our models using borrower fixed effects. In these regressions, identification is thus coming from the subset of borrowers that have moved over our time period. The results are qualitatively very similar to those of the baseline models.

Table 1: Local banking market competition and refinancing decisions

This table presents coefficients from linear regressions where the dependent variable is a dummy variable that equals one if the household refinances- (internally and/or externally). Robust standard errors clustered at the borrower level.

We then analyze the effects of switching costs for households. As expected, we find that households that already have a credit relation with another bank are more likely to refinance externally. However, this effect is mitigated if the borrower’s current lender has a branch locally, which may be associated with a higher cost of switching away. Moreover, the impact of having another bank on external refinancing is larger in low-income municipalities, suggesting that switching costs matter more there.

Finally, we look at the realized gains conditional on refinancing. In line with the implications of our model, we find that the average gains from refinancing externally are smaller for households with lower switching costs (i.e., for households that already have another bank and for households whose current lender does not have a local branch).

Our paper contributes to different strands of the literature. First, it has been well documented that households often fail to refinance even when it seems optimal to do so (Keys et al. 2016). An extensive literature studies the determinants of household refinancing decisions, mainly focusing on (relatively fixed) borrower characteristics (Agarwal et al. 2016; Bajo and Barbi 2018; Johnson et al. 2019; Andersen et al. 2020). Fewer papers have studied local factors, although recent work by Fisher et al. (2021) shows that the lower refinancing activity in less wealthy areas in the U.K. cross-subsidizes the higher activity in wealthier areas. Our innovation is to study the role of local banking market characteristics (and of borrowers’ bank relations).

Second, our paper makes a theoretical contribution by modeling mortgage refinancing as a bargaining game—involving the borrower, the lender, and an outside bank—in the spirit of Rubinstein (1982) and Acharya et al. (2012). In our model, the strategic actions of banks are affected by both the probability that a household will stop searching for refinancing offers and by a household’s (financial or non-financial) cost of switching banks. Our model yields empirical predictions on households’ refinancing decisions and payoffs overall, while also giving insights into what drives internal refinancing vs. external refinancing. Our work relates to that of Allen et al. (2014), who study the role of competition in search-and-negotiation markets by analyzing the price effects of a merger between two mortgage lenders. Recent survey results by Bhutta et al. (2021) point to an important role for shopping behavior in determining the cost of mortgages, but not much work exists on the topic of the costs and payoffs of switching mortgage lenders for households—unlike in the context of corporate borrowing (Ioannidou and Ongena 2010; Barone et al. 2011).

On the policy front, our paper is in line with other studies that emphasize the importance of local mortgage market concentration on refinancing. While local lending concentration does not seem to affect interest rates on new mortgages (Fuster et al. 2022), there may be an effect on lending standards and fees (Buchak and Jørring 2021). Other work has focused on how competitive frictions in the refinancing market can hinder the transmission of monetary policy (Scharfstein and Sunderam 2016; Agarwal et al. 2022). Our paper provides additional evidence that local mortgage market concentration affects the extent of refinancing when interest rates go down. As such, it also contributes to a broader discussion about the transmission of monetary policy through the mortgage market (Benetton et al. 2021; Berger et al. 2021) and the effect of monetary policy on the distribution of household debt (Emiris and Koulischer 2021, and references therein).

Finally, our paper adds to a recent body of work that underlines the importance of local bank branches for both households (Ergungor 2010; Célerier and Matray 2019) and firms (Nguyen 2019). Such research is particularly relevant in light of the ongoing changes in the geography of the banking landscape.

Acharya, Viral V, Denis Gromb, and Tanju Yorulmazer, 2012, Imperfect Competition in the Interbank Market for Liquidity as a Rationale for Central Banking, American Economic Journal: Macroeconomics 4, 184–217.

Agarwal, Sumit, Gene Amromin, Souphala Chomsisengphet, Tim Landvoigt, Tomasz Piskorski, Amit Seru, and Vincent Yao, 2022, Mortgage Refinancing, Consumer Spending, and Competition: Evidence from the Home Affordable Refinance Program, The Review of Economic Studies rdac039.

Agarwal, Sumit, Richard J. Rosen, and Vincent Yao, 2016, Why Do Borrowers Make Mortgage Refinancing Mistakes?, Management Science 62, 3494–3509.

Allen, Jason, Robert Clark, and Jean-François Houde, 2014, The Effect of Mergers in Search Markets: Evidence from the Canadian Mortgage Industry, American Economic Review 104, 3365–3396.

Andersen, Steffen, John Y. Campbell, Kasper Meisner Nielsen, and Tarun Ramadorai, 2020, Sources of Inaction in Household Finance: Evidence from the Danish Mortgage Market, American Economic Review 110, 3184–3230.

Bajo, Emanuele, and Massimiliano Barbi, 2018, Financial Illiteracy and Mortgage Refinancing Decisions, Journal of Banking & Finance 94, 279–296.

Barone, Guglielmo, Roberto Felici, and Marcello Pagnini, 2011, Switching costs in local credit markets, International Journal of Industrial Organization 29, 694–704.

Benetton, Matteo, Alessandro Gavazza, and Paolo Surico, 2021, Mortgage Pricing and Monetary Policy, Technical report.

Berger, David, Konstantin Milbradt, Fabrice Tourre, and Joseph Vavra, 2021, Mortgage Prepayment and Path-Dependent Effects of Monetary Policy, American Economic Review 111, 2829–2878.

Bhutta, Neil, Andreas Fuster, and Aurel Hizmo, 2021, Paying Too Much? Borrower Sophistication and Overpayment in the US Mortgage Market, Technical report.

Buchak, Greg, and Adam Jørring, 2021, Do Mortgage Lenders Compete Locally? Implications for Credit Access, Technical report.

Célerier, Claire, and Adrien Matray, 2019, Bank-Branch Supply, Financial Inclusion, and Wealth Accumulation, Review of Financial Studies 32, 4767–4809.

Emiris, Marina, and François Koulischer, 2021, Low Interest Rates and the Distribution of Household Debt, Working paper.

Emiris, Marina, François Koulischer and Christophe Spaenjers, 2022, Bank Competition and Bargaining over Refinancing, Working paper.

Ergungor, Ozgur Emre, 2010, Bank Branch Presence and Access to Credit in Low- to Moderate Income Neighborhoods, Journal of Money, Credit and Banking 42, 1321–1349.

Fisher, Jack, Alessandro Gavazza, Lu Liu, Tarun Ramadorai, and Jagdish Tripathy, 2021, Refinancing Cross-Subsidies in the Mortgage Market, Technical report.

Fuster, Andreas, Stephanie Lo, and Paul Willen, 2022, The Time-Varying Price of Financial Intermediation in the Mortgage Market, Technical report 26.

Ioannidou, Vasso, and Steven Ongena, 2010, “Time for a Change”: Loan Conditions and Bank Behavior when Firms Switch Banks, The Journal of Finance 65, 1847–1877.

Johnson, Eric J, Stephan Meier, and Olivier Toubia, 2019, What’s the Catch? Suspicion of Bank Motives and Sluggish Refinancing, Review of Financial Studies 32, 467–495.

Keys, Benjamin J., Devin G. Pope, and Jaren C. Pope, 2016, Failure to Refinance, Journal of Financial Economics 122, 482–499.

Nguyen, Hoai-Luu Q., 2019, Are Credit Markets Still Local? Evidence from Bank Branch Closings, American Economic Journal: Applied Economics 11, 1–32.

Rubinstein, Ariel, 1982, Perfect Equilibrium in a Bargaining Model, Econometrica 50, 97.

Scharfstein, David, and Adi Sunderam, 2016, Market Power in Mortgage Lending and theTransmission of Monetary Policy, Technical report.