This Policy Note is based on “Are the new EU budget rules fit for long-term challenges and ambitions?”, RaboResearch, 2024.

After years of debate, EU member states finally agreed to reform the EU budget rules. The reform was a long-standing wish for many. Frugal member states demanded better compliance and stricter enforcement, while highly indebted countries saw the rules as too austere. The pandemic’s impact on debt and the EU’s strive for strategic autonomy complicated the talks even more, but also increased the need for reform. The new rules reflect a compromise between member states with differing views on fiscal discipline and growth. The rules are designed to guide member states towards a sustainable fiscal path, with a focus on reducing debt ratios and supporting investments that align with EU priorities in digital and energy transition, strategic autonomy, and defence.

The reform’s success in reducing debt ratios and fostering strategic investments remains to be seen, as the risk of fiscal slippage is still present. Some member states, such as France, Belgium, Italy and Spain may have to enhance their efforts to align with the new regulations.

After years of debate, EU member states have finally agreed to reform the EU budget rules. The reform was a long-standing wish for many. Frugal member states demanded better compliance and stricter enforcement, while highly indebted countries saw the rules as too austere. The pandemic’s impact on debt and the EU’s striving for strategic autonomy further complicated the talks, but also increased the need for reform. In this publication, we analyze whether (i) member states comply with the new rules, and (ii) the new rulebook will, as intended, succeed in reducing debt ratios in a way that supports growth and induces strategic investments in the areas of digital and green transformation, of social and economic resilience, and of defence capabilities.

In short, the new rules seem to be better fit for purpose than the old ones. However, the risk of fiscal slippage remains substantial and the room for strategic spending remains limited. Some member states may have to step up their game to comply with the rules.

Infographic 1: The new EU budget rules in a nutshell

Source: RaboResearch.

The framework is based on medium-term fiscal plans aiming to achieve a sustainable debt path toward 60% of GDP and a budget deficit well below 3% of GDP.1

The Maastricht Treaty values of 60% of GDP for debt and 3% of GDP for the budget deficit remain unchanged. However, the requirements for reaching them, including the allowed deviations, have changed. For countries with debt ratios above 60% of GDP and/or a deficit above 3% of GDP, the European Commission (EC) conducts a debt sustainability analysis (DSA). The DSA determines the net expenditure path a member state will have to follow during the adjustment period to comply with the debt and deficit rules – a so-called reference trajectory. Net expenditure is defined as the total public expenditure minus one-offs, discretionary revenues, interest payments, cyclical spending related to unemployment, and co-financing of EU-funded programs. The reform should make the budget rules less procyclical than they currently are. Each member state will then draw up its own fiscal plans, which should include a planned fiscal trajectory, reforms and investments, and measures to tackle macroeconomic imbalances.

If a country deviates from the net expenditure path and/ or breaches the 3% deficit ratio, the European Commission assesses whether this is problematic and whether there are mitigating factors that “justify”’ the divergence. Mitigating factors include many possibilities, such as the severity and projected duration of the breaches, the overall debt challenges, the adherence to the promised path of reforms and investment, and defence spending. The Commission also takes the macro-economic environment into account to allow for fiscal flexibility in case of severe and unforeseen downturns. Specifically, both the general and the country-specific escape clause are kept in place.

If there are insufficient mitigating factors at play, the European Commission will propose to the Council to open an excessive deficit procedure (EDP) – although the name suggests otherwise, note that both an excessive deficit and excessive debt can trigger the EDP. If an excessive deficit procedure is opened due to a breach of the deficit rule, the net expenditure path set by the Commission should guarantee a structural adjustment of at least 0.5% of GDP per year. During the transition phase from 2025 to 2027, the Commission may lower that benchmark to reflect the recent increase in interest expenditures. If the excessive deficit procedure is opened due to a violation of the debt rule, countries should return to the initial expenditure path as projected in their fiscal plans, unless the Commission finds the old path inadequately meets the rules.

If the countries do not comply and if there are not enough mitigating factors to explain this lack of compliance, the European Commission could fine member states by 0.05% of their national GDP every six months until they comply.

Some countries should have no trouble following the new rules in the coming years, while others will clearly have to step up their game. Moreover, compliance doesn’t necessarily mean a loose fiscal stance ahead. It “merely” means that a country is projected to do what is required.

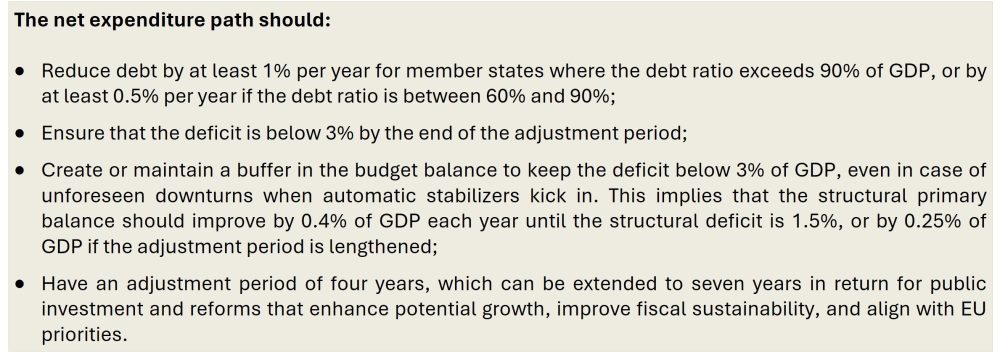

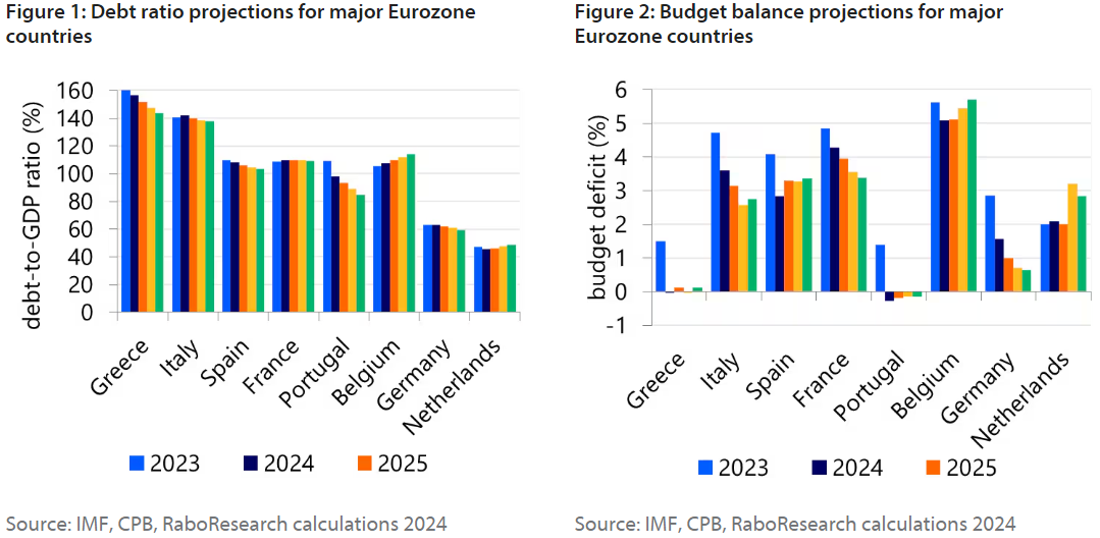

Not surprisingly, countries with low debt ratios are likely to comply. Yet Greece and Portugal, despite their high debt, are also likely to comply during the first adjustment period. This is due to the rapid projected decline in their debt ratio. But not everyone is in the same boat. In Figures 2 and 3, we show our forecast for the debt-to-GDP ratio and the budget deficit for some key Eurozone countries, based on the methodology explained in this report.2 (Calculations were finalized at 26 February, data revisions and realizations after 27 February have not been taken into account).

There are a few figures that stand out. For instance, Belgium and France do not reduce their debt, and their budget deficit doesn’t fall below 3% in the coming years. Spain’s budget deficit is projected to dip below 3% this year, but is projected to rise again thereafter. In our view, these three countries will likely have to improve their budgets to comply with the rules.

The results for Italy3 are more ambiguous. Its budget deficit should fall quite rapidly in the short term, but stabilizes just below 3% from 2026 onward, which hardly is a sufficient resilience buffer. Moreover, while Italy’s debt ratio does decline over the forecast horizon, it doesn’t average the required 1% per year and even increases in 2024. That said, the decline accelerates toward the end of our forecast horizon. This implies that the annual reduction of 1% is within reach if the adjustment period is lengthened (as expected), and the government does not change its fiscal course, which is uncertain. That said, we think the Commission will be lenient with Italy, given that its debt metrics are moving in the right direction. Especially if Italy boosts its spending on defence and/or other strategic sectors and commits to the reforms and investments in its medium-term plans.

Finally, the Netherlands warrants some attention. The Netherlands clearly meets the debt rule, but its budget deficit is projected to rise substantially in 2026, to just above the 3% limit. This should not pose a problem right away, as the breach is small and projected to be corrected in 2027, while the debt ratio is low. But if the Commission’s debt sustainability analysis indicates that deviations are set to increase beyond that horizon, as the Dutch CPB projects, Brussels could urge the Netherlands to change course. If it doesn’t change course now, it will likely have to do so during the next adjustment period.

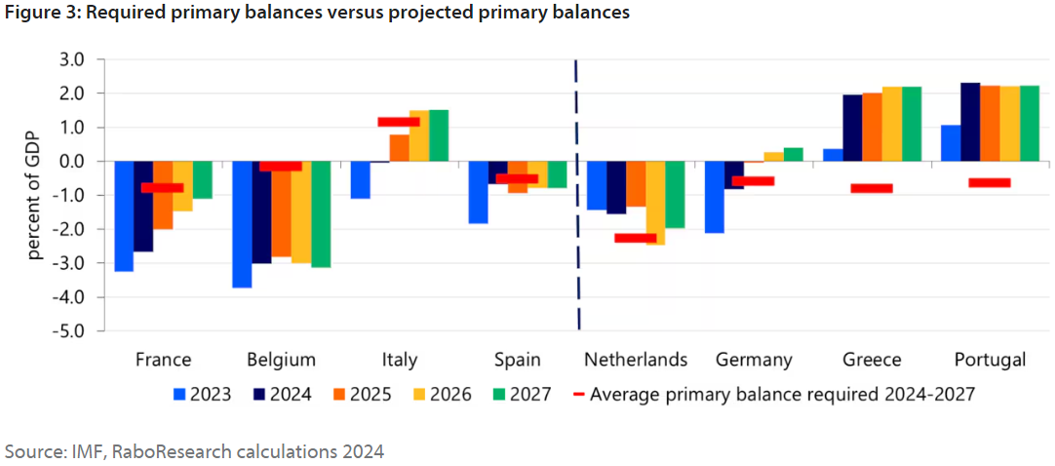

We can estimate how much the primary balance would need to improve for the debt ratio to fall by 1% on average and for the budget deficit to fall below 3%, based on some simple assumptions that ignore the effects of fiscal tightening on growth, inflation and interest rates. Figure 3 shows that France and Belgium have a lot of work to do, both in terms of their starting positions and their planned trajectories. The debt ratio is the toughest rule for both countries. Belgium in particular will need a serious change in its fiscal policy to comply. But France will also need to speed up its fiscal consolidation in the short term.

Meanwhile, Spain and Italy need significant improvement in their primary balance from current levels, but the gap between the rules and the projections is actually quite small. This suggests that a major conflict with Brussels is unlikely. However, they will still need to show commitment and likely take some corrective measures to convince the Commission of their good intentions. This requires both countries to stick to their planned fiscal trajectories and to live up to their medium-term reforms and investment pledges. The Netherlands, Germany, Greece and Portugal are unlikely to face compliance problems during the first adjustment period. Germany will have to tighten its fiscal policy from 2023 levels (which it is already planning to do), while the others could even afford some fiscal loosening.

The new rules tackle some important flaws of the old framework, but are not perfect either

Importantly, the rules become more viable when hard-coded “one size fits all” rules are replaced by tailor-made multi-year fiscal trajectories. The new debt rule also poses less risk to growth than the old one, while still ensuring a downward path of debt-to-GDP4. Moreover, national capitals have more ownership as they draw their own multi-year plans, although the plans have to be approved by the European Commission. This should, in theory, improve adherence to the rules and reduce tensions between Brussels and national capitals.

In addition, the preventive arm no longer rigidly focuses on the erratic computations of countries’ structural balances.5 The fiscal trajectories will instead be informed by a well-established debt sustainability analysis. This analysis leaves room to incorporate the positive impact of reforms and investments on future GDP growth and debt sustainability. The results from the DSA and the resulting adjustment path also need to be signed off by the European Council. This, too, increases national ownership.

That being said, the European Commission still needs to estimate the cyclical part of the unemployment benefit expenditure and revenues. Furthermore, while well-established, debt sustainability analyses still have some subjective elements. The Commission will need to make assumptions on the impact of investments and reforms and future growth, interest rates, inflation and fiscal policy. This could still lead to a wide range of potential outcomes.

Finally, enforceability remains doubtful, as the new framework won’t provide sufficient fiscal leeway for all investment and spending required in Europe’s quest for strategic autonomy.

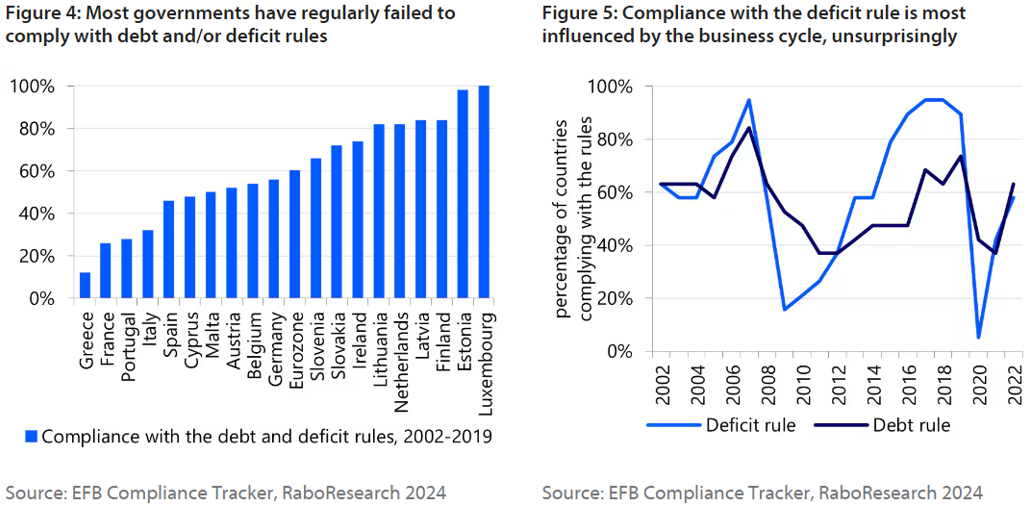

Enforcement has been a major issue since the budget rules were introduced. Letting an outside force, i.e. Brussels, punish a national government based on “Brussels-imposed” rules, is often seen as a threat to a member state’s fiscal sovereignty. Moreover, it feels counterproductive to fine governments that already have fiscal challenges. Figures 4 and 5 show that the rules have been broken by many countries over the years. However, no fines have ever been imposed. This shows that the European Union is still far from a fiscal union.

The new framework gives national capitals more flexibility to set their own fiscal trajectories. In return, the European Commission has vowed to enforce the rulebook more strictly than before. The idea is that increased sovereignty and national ownership improves adherence, while lower fines are more likely to be imposed.

Yet, the European Commission still wields a lot of discretionary power when deciding whether to open an excessive deficit procedure (EDP). Though there are good arguments in favour of such a discretionary approach, it does imply enforcement of the rules is far from straightforward and, from this perspective, the new rulebook won’t improve it. Indeed, in order for the rules to be enforced, this also means that the Commission shouldn’t succumb to political pressure from powerful or influential member states. That is, in all likelihood, a fantasy. And even if it does not, the de facto politicised Council has to approve the Commission’s proposal for starting an excessive deficit procedure or imposing a fine. As such, the new rules raise the risk of fiscal slippage and are likely to facilitate structurally higher debt levels than the 60% limit implies.

Still, even though hard enforcement is unlikely, the rules are not pointless. They foster dialogue between Brussels and member states and the increased focus on debt sustainability analyses helps markets to evaluate a member state’s fiscal stance. Importantly, in the past, market pressure mounted if governments were unwilling to take action to correct excessive deviation from the rules. Going forward, if governments appear unwilling to cooperate with Brussels, this endangers the possibility of obtaining EU support through for example the ESM and ECB TPI, if necessary. This should translate into higher risk premia. Hence, if push comes to shove, we expect market pressure will compel governments to act.

Importantly, the new rules are more supportive of the required investments in strategic areas than the old one. Countries can extend their adjustment periods from four to seven years and avoid excessive deficit procedures and fines if they invest in priority areas. This could benefit defence spending in particular. This change is crucial.

However, there is still not enough room to increase investments at the scale needed. In a recent report, we laid bare the EU’s structural weaknesses as it aims for “strategic autonomy”: a shortage of key (energy) resources, industrial competitiveness, and military power. All three are interconnected and require huge investments of 2% to 5% of GDP, annually.

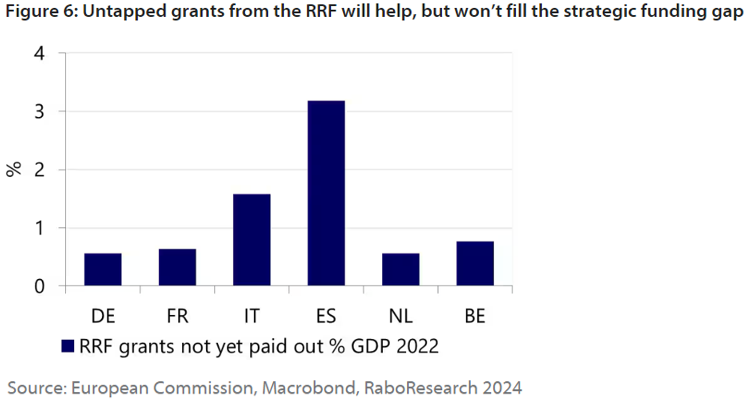

Some of these investments will have to come from the private sector, but governments would also have to contribute, to find funding of this scale. Note that untapped grants in the Recovery and Resilience Facility (RRF) could go some way in helping especially the Southern member states in the next few years. But it would only be a temporary relief, and it does not seem to be enough in most cases. It is also highly unlikely that countries will be able to fulfil all remaining milestones required to actually obtain the funds, before the RRF’s official deadline in 2026. The financing of EU-endorsed public investment could also have been excluded from the deficit calculations altogether, but this proved to be a step too far. As such, it feels like a short-term fix rather than a structural reform to finance the EU’s long-term investment needs.

However, a framework that would allow for investments at the scale of 2% to 5% of GDP, without balancing measures, could also prove counterproductive in due time. Not all spending to improve strategic autonomy leads to higher structural growth. Consequently, unlimited spending – without spending cuts or revenue measures elsewhere – could harm debt sustainability and increase risk premiums. It could also fuel inflation, if it adds more to demand than it raises supply. This is not necessarily bad for public debt sustainability in the short term, but it reduces households’ purchasing power, could spark social unrest, and would keep interest rates higher for longer. This would slow down (private) investments, as also explained in the report.

So, essentially, whatever the fiscal rules are, we argue that a holistic approach is needed to support Europe’s quest for strategic autonomy. Such an approach would involve EU funding, credit bifurcation, selected protectionism, and strategic spending.

The EU’s new budget rules reflect realpolitik. Fiscal sovereignty is important for EU member states, and they resist losing it. The new rules try to meet such demands by giving more ownership to national member states. They are also more realistic than the old ones, especially the debt rule. Finally, they provide more space for reforms and investment that improve a country’s long-term fiscal sustainability. They represent a step forward.

The changes in the rules also reflect that the world is turning into a more volatile place, and recognize the EU’s reliance on other countries for defence, energy, and goods. The new framework creates more short-term fiscal space for investments to pursue more strategic autonomy. However, this is not enough to address the EU’s long-term challenges and ambitions. The negotiations did not result in lasting reform of a permanent fiscal capacity at the EU level, which would be essential for enhancing the EU’s strategic autonomy in a sustainable way. This is a missed opportunity.

The framework is therefore no panacea. It cannot ensure fiscal sustainability or enough spending in strategic sectors by itself. We estimate that in Belgium, France, Italy, and Spain, the fiscal effort needed to follow the rules in the coming years will be large, based on the improvement in the primary balance from its current level. As the economy recovers and energy support measures end, some of this effort could come easily, but discretionary action will also be needed. Especially because of the rising costs of the aging society. In all countries except Spain, fiscal policy will have to be tighter than it was in the four years before the pandemic.

Therefore, we expect calls for extending the 2026 deadline of the Recovery and Resilience Facility and new common EU funding for strategic investment in defence and the energy transition. Governments cannot afford all the transitions and satisfy an unhappy society at the same time.

The updated fiscal rules are still subject to votes both in the European Council and in the European Parliament. Once adopted, the rules will be implemented soon after. Each member state will need to submit their first national plans by 20 September 2024.

We use the IMF’s projections instead of the national ones. These are usually quite similar, but the IMF has a longer forecast horizon. The only exception is the Netherlands, where the recent CPB projections are much worse than the IMF’s. We use the CPB’s data.

Our projections for Italy are uncertain. There are about EUR 100bn of unclaimed tax credits. These have already been recorded in the previous years’ budget balances, but they will increase the debt stock when they are claimed in the coming years. At the same time, the government plans to sell about EUR 20bn of assets. The timing of both is uncertain. We currently assume that debt will grow by an extra EUR 22bn per year.

The old debt rule stipulated that the debt ratio should be reduced by 1/20th of the difference between the current debt ratio and the maximum threshold of 60%, annually. This would have meant an annual reduction of some 4% of GDP for Italy, for example, which would have significantly undermined GDP growth. That said, the new rules still require some rather intense adjustment measures in several member states.

Using a structural rather than merely the general budget balance, which is influenced by the business cycle, was a good idea in theory, yet proved to be a monstrosity in reality. The balance was calculated as the product of the output gap and the elasticity of the general budget balance. In hindsight, the balance appeared to be based on faulty calculations of potential GDP, the output gap, and the elasticity.