References

African Development Bank, African Economic Outlook 2018.

Antil A. (2018), „Afrique subsaharienne: la mondialisation par le bas“, Ramses 2018.

Dorin B., Hourcade J.-C. and M. Benoit-Cattin (2013), „A World Without Farmers? The Lewis Path Revisited”, CIRED Working papers No 47-2013.

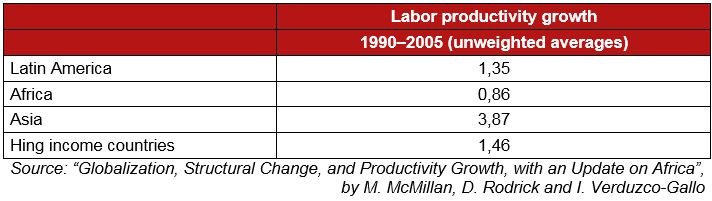

McMillan M., D. Rodrick and I. Verduzco-Gallo (2014), „Globalization, Structural Change, and Productivity Growth, with an Update on Africa“, World Development Vol. 63, pp. 11–32, Elsevier Ltd.

OECD Development Centre, Policy note on Africa “Betting on a growing market”, October 2015.

OECD Development Centre, Policy note on Africa “Investing in growing African cities”, September 2016 .

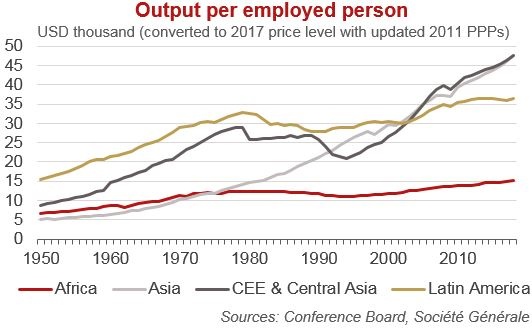

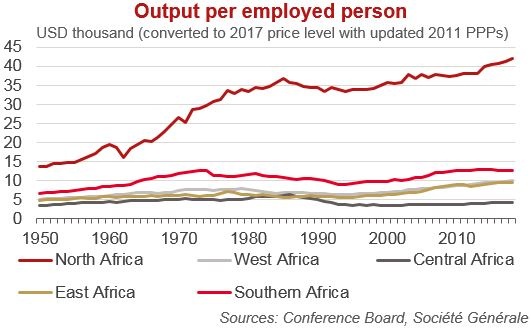

The Conference Board (2018), Total Economy Database™ (Adjusted version).

UNCTAD, World Investment Report 2018.