This note explores the effectiveness of the ECB’s ‘quantitative easing’ program. It argues that an (unsterilized) bond purchase by a central bank is akin to shortening the maturity of outstanding government debt. It then points out that the government bond purchasing program in the euro area is implemented by national central banks (NCBs) operating on their own account, and that different NCBs buy different maturity baskets. The PSPP (Public Sector Purchasing Program) of the ECB is thus equivalent to a shortening of the maturities of national public debt which differs from country to country. Event studies suggest that the announcement of the PSPP coincided with reductions in risk and term premia, as well as some risk free rates. However, these effects were temporary and had dissipated a few months after the start of the actual bond buying despite the extraordinary size of the purchases, which over time amounted to 20% of GDP. Risk and term premia started tightening again only when the tapering of bond purchases started. The evidence suggests thus that the end of central bank bond purchases should not be destabilizing.

Introduction: ‘Large Scale Asset Purchases’ (LSAP) versus ‘Quantitative Easing’ (QE)

The term ‘quantitative easing’ today refers mainly to a situation in which the central bank has brought its (usually short-term) policy rates to the zero lower bound (which could be a slightly negative value). But the central bank might want to ‘ease’ monetary conditions even further if inflation remains significantly below its target. The only policy instrument a central bank has left in that situation is to increase the size of its balance sheet by buying assets. Risk averse central banks have usually concentrated their asset buying on government bonds, which present the biggest pool of relatively safe and liquid assets. A key condition of quantitative easing is that the asset purchases are not sterilized since the ultimate aim is to increase the size of the balance sheet of the central bank. This aspect is key to understand the US experience.

Bond purchase programs in the US

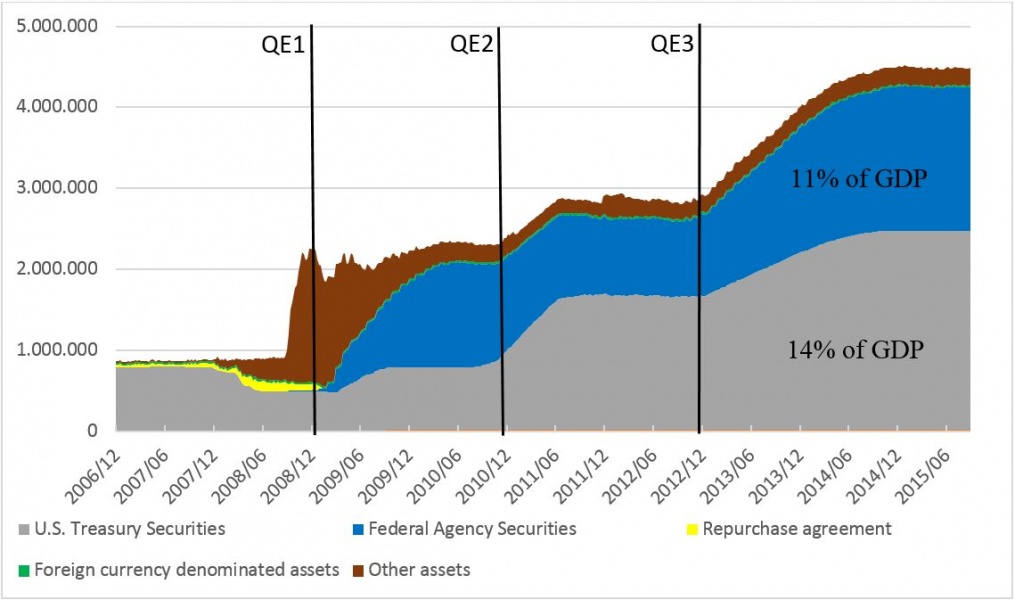

In November 2008, the Federal Reserve announced the first round of asset purchases. These purchases were to include government-sponsored enterprise (GSE) debt and agency mortgage-backed securities (MBSs) of up to USD 600 billion. The motivation given was that the spread on agency bonds had increased, thus making house purchases more expensive.1 After announcing the intention to extend the program in January 2009, the Federal Open Market Committee (FOMC) decided to purchase an additional USD 750 billion in (agency) MBSs, USD 100 billion in agency debt, and also started to purchase long-term Treasury securities worth USD 300 billion in March 2009. In total, the Fed purchased assets worth around USD 1.5 trillion between November 2008 and March 2010 (see also Borio and Zabai, 2016).

However, a key, often overlooked aspect of this so-called QE1 operation was that the balance sheet of the Federal Reserve was supposed to remain unchanged. During 2008 the Federal Reserve had expanded its balance sheet by engaging in foreign currency swaps, providing money market funds and banks with liquidity. As can be seen in Figure 1 below, these assets were reduced to almost zero over the period of QE1 and substituted with bonds, mostly mortgage-backed securities backed by government-sponsored enterprises (Stroebel and Taylor, 2012).

Figure 1: Federal Reserve balance sheet (USD million)

Notes: Percentage refers to 2014 GDP. Federal Agency Securities represent debt securities and mortgage-backed securities backed by government-sponsored enterprises.

Source: Federal Reserve.

At the time of the announcement of (what is called now) QE1 (November 2008) total assets on the balance sheet of the Federal Reserve amounted to roughly 2.2 thousand billion USD. By the time QE1 ended (March 2010) the balance sheet had increased only to 2.35 thousand billion USD, an increase of only about 150 billion, less than 1% of US GDP. Contrary to a widespread narrative QE1 did not imply a large expansion of the balance sheet of the central bank.

However, QE1 constituted indeed a ’Large Scale Asset Purchase’ (LSAP) since, between early 2009 and mid-2010, the Federal Reserve did indeed acquire about 1.5 thousand billion USD of a mixture of US Treasuries, GSE bonds and MBSs. Its balance sheet did not expand over this period because at the end of 2008 the Federal Reserve had provided the banking system with almost 1.5 thousand billion USD in ’liquidity facilities’. These facilities were gradually withdrawn, but the monetary base was kept approximately constant through the first ’LSAP’, as it was correctly called then.2 In this sense the name ’QE1’ is a misnomer: the first LSAP was not meant to provide a ’quantitative easing’ of monetary conditions, but rather to remedy perceived distortions in the pricing of mortgage backed securities. Viewed in this way one should not count the ’QE1’ episode as showing the effectiveness of ’quantitative easing’ in general. The motives for the first round of asset purchases by the Fed in 2008/9 were similar to those the ECB adduced when it started buying Greek and other government debt in 2010 under its SMP program, which is not usually regarded as constituting ’QE’. (The purchases under the SMP were also supposed to be sterilized.)

Real ’quantitative easing’ started thus in the US only with QE2 and QE3, which indeed led to large increases in the balance sheet of the FED.

In October 2010, the FOMC announced the second round of QE (QE2). It contained purchases of USD 600 billion worth of treasuries and was finished in June 2011. Eventually, the third round of QE (QE3) started in September 2012. It targeted a monthly purchase of USD 85 billion. Overall, the Fed balance sheet increased by 600 billion USD through QE2 and about 1.5 thousand billion through QE3 (roughly 13% of US GDP).

The fact that the first LSAP did not really constitute ‘quantitative easing’ poses a problem for the literature on the effectiveness of ’QE’ in general. Surveys of empirical studies usually find that ’QE1’ had a much larger impact on financial markets than QE2 and many studies find no impact for QE3 (Borio and Zabai, 2016). But the latter had implied the by far largest increase in the balance sheet of the Federal Reserve (from roughly 2.8 to 4.4 thousand billion USD, or about 10% of GDP). This lack of a link between the increase in the balance sheet and impact on financial markets, makes it difficult to present a unifying analytical framework for QE in general.

In the US, the largest bond buying operation had the smallest impact on financial markets, and the first LSAP operation, which had little impact on the overall balance sheet, is usually credited with the largest impact on financial markets.

QE as ‘operation twist’ and peculiarities of the euro area

Describing the PSPP, which is the official name of the ‘quantitative easing’ program in the euro area, as ‘the ECB buying hundreds of billions of government bonds’ is not correct. The Governing Council of the European Central Bank takes the key decisions, but its policy is executed mostly by the euro area national central banks (NCBs). Normally all NCBs undertake the same operations and the results are pooled. However, this does not apply to the government bond-buying program (the PSPP): each NCB buys only the bonds of its own government, and it does so on its own account. Thus, the Banca d’Italia has bought only Italian government bonds and the Bundesbank only Bunds.

In a country with its own currency, the central bank and the Treasury can be consolidated for fiscal purposes, at least in the long run. Any gains or losses that the central bank makes are usually transferred to the (national) Treasury. This is one of the reasons why the fact that monetary and fiscal policy cannot be kept completely separate under extreme circumstances matters less in a national context when the country has its own currency.

Within the euro area, one could consolidate the sum of all national Treasuries with the accounts of the ECB, as the Eurosystem, sooner or later, transmits most of its profits to national Treasuries, according to the capital key, which determines the shares of each country in the ECB.

However, this applies only to standard monetary policy operations. By contrast, for example, emergency liquidity assistance (ELA) is granted by NCBs and all the losses or gains from ELA operations remain with the national central bank that granted it.

The PSPP was clearly not regarded as a ‘standard’ monetary policy operation since 80% of the asset purchases are undertaken by the NCBs under their own risk.3 The reason for this decision was obviously that the NCBs from creditor countries, such as Germany or the Netherlands, were worried that they might have to share the losses if there was a default on the bonds bought under this programme. Moreover, these purchases, which remain only on the books of the individual NCBs, concern exclusively national bonds.

The NCBs are part of the larger public sector of their country and they transfer all or most profits or losses of these transactions eventually back to their own government. When the Banca d’Italia buys a long-term Italian government bond it is thus as if the subsidiary of a large corporation buys the debt of the parent company (issuing itself short-term liabilities). Ordinarily one would not expect such an operation to have a large impact. One could thus compare the quantitative easing program in the euro area to a gigantic ‘liability’ management exercise which consists essentially of a reshuffling of (national) public debt from one part of the public sector (governments) to another one (NCBs).

The ultimate effect of this ‘liability’ management is to shorten the effective duration of national public debt. The deposits of banks with the NCBs represent effectively public debt (held by commercial banks) with a zero duration (these deposits can be withdrawn daily). When the Bundesbank buys a German government bond with a residual maturity of 10 years, it reduces the maturity of that part of the German public debt from 10 years to zero (one day, to be precise). If short-term interest rates were to increase, the re-financing costs of the Bundesbank would increase, reducing its profits and thus its contribution to the federal budget accordingly (the income from the long-term bonds in the Bundesbank portfolio would not change).

This shortening of the effective duration of government debt throughout the euro area is substantial given the size of the PSPP (over 20% of euro area GDP), but will vary from country to country.

In the case of Germany, for example, the Bundesbank is likely to have bought about one-quarter to one-fifth of all (publicly traded) German (federal) government debt over the lifetime of the PSPP. If the average maturity of the purchases of the Bundesbank is about six years, the effective duration of German government debt (at least that which is in a publicly tradable form) would be reduced by 1.2 to 1.5 years.

For Italy, the reduction in the effective maturity of public debt might be somewhat different because there are two off-setting factors: The Banca d’Italia buys about the same amount of debt as a proportion of GDP, but a lower proportion of the outstanding debt because Italy’s debt/GDP ratio is much higher (about double) than the German one. This factor would tend to reduce the impact of the bond purchases on the effective average maturity of Italian government debt. But the Banca d’Italia has also bought, on average, longer-term maturities than the Bundesbank. This factor would tend to go in the opposite direction.

In the case of QE, longer-term government bonds are substituted by short-term central bank liabilities, which can be held only by commercial banks. Another way to achieve a reduction of the maturity of the debt held by the public arises when the central bank already holds short-term government debt. This was the case in the US, where the Fed held considerable amounts of short-term Treasuries. It was thus able in 2011 to launch the so-called Operation Twist (OT), under which it undertook to purchase 400 billion USD worth of Treasury bonds with maturities of 6 to 30 years and sell bonds with maturities of less than 3 years, thus extending the average maturity of the Fed’s portfolio.

The only difference between such an operation (which leaves the size of the balance sheet of the central bank unchanged) and QE is the form of the maturity transformation. Swanson (2011) shows that the QE2 operation in 2011 was actually comparable in size to a similar plan of 1961, under which the Federal Reserve also increased its holding of longer-term debt in an attempt to lower long-term rates.

The reduction in the maturity of government debt achieved through QE could also be achieved without any central bank involvement by changes in issuance of (national) debt management offices. For example, in Germany the debt management office could have just stopped issuing any new paper with a maturity over a few months. All longer-term bonds falling due would thus have to be refinanced with very short-term paper (called Bubills). Such a policy would have led to the same reduction in the amount of longer-term (say 10 year) Bunds as the PSPP. The only difference would have been the form of the short-term debt issues: short-term government paper versus commercial bank deposits at the Bundesbank.

One could of course argue that a deposit of a commercial bank at any national central bank is a liability of the entire Eurosystem, rather than the national central bank itself. This is true in the sense that commercial banks could transfer their deposits from one NCB to another. But this would only change the nature of the liability of the NCB. Instead of deposits it would have Target2 liabilities (Gros 2017). Moreover, what really matters for public finances is not so much what entity is legally ‘liable’. What is in fact relevant are the flows of interest payments (on the bonds and their counterpart, which could be either reserves or Target2 liabilities) which ultimately all accrue to the government. Shortening the maturity of public debt yields a short-term cash flow benefit for the Treasury as long as the yield curve is upwards sloping as illustrated below.

Public Finance benefits of QE

The PSPP will benefit public finances as long as the refinancing cost of the short-term liabilities of the NCBs stay ultra-low (negative at present). But the benefit varies from country to country.

For example, for Germany the fiscal gain could be less than one fifth of 1% GDP, given ten-year Bunds at 0.4% and a negative refinancing cost for the Bundesbank at minus 0.4%. The total annual gain would thus be 0.8 percent on debt worth about 20% of GDP, or about 0.16% GDP.

For the periphery the gain should be more substantial given the higher interest rates that government have to pay there. For example, for Italy the fiscal gain might be about double the one for Germany. The yield on 10-year Italian government debt has varied more than that on German debt, but it has rarely been far from 2%. The refinancing cost of the Banca d’Italia is somewhat higher than that of the Bundesbank since the counterpart of most of its asset purchases has been an increase in Target2 balances (see Gros 2017 for details) and the rate of remuneration on Target2 balances is around zero. This implies a gain of around 2 percentage points on 20% of GDP, or 0.4% of GDP.

The debt service savings resulting from the lowering of the effective maturity of public debt through the PSPP are thus in some cases substantial, even if one does not assume that the bond purchases had any impact on rates.

To the extent that one assumes that the bond purchases also reduced overall interest rates the gain would of course be much higher (but there is little evidence of this, as argued below).

Reducing the supply of long-term government bonds available to the public: the portfolio balance channel

If asset purchases of the central bank are supposed to lower (long-term) interest rates by reducing the supply of longer-dated government bonds to the public, one should concentrate the market for these securities. Greenwood et al. (2014) argue that monetary and fiscal policies in the US have been pushing in opposite directions, with debt management policies partially offsetting the impact of monetary policy.

The very large US federal deficits during the QE period (2008-2011) led to a very large increase in the supply of longer-dated federal debt securities (bonds), given that a large proportion of any debt issuance of the US Treasury is always in longer-term paper. Moreover, explicit decisions by the US debt management office to lengthen the average maturities of the new securities it was offering to the public, further substantially increased the outstanding amount of longer-term US federal debt securities.

About one-half of this increase in longer-dated US federal securities from fiscal and debt management policies was undone by the various rounds of asset purchases of the Federal Reserve. (Large deficits combined with the lengthening of maturity by the debt management office would have increased the supply, measured in the equivalent of 10-year bonds, by close to 30% of GDP. But the various rounds of asset purchases by the Federal Reserve took about 15% of GDP from the market.)

The net result of these two opposing policies has thus still been a substantial increase in the longer-term securities held by the public. According to the ‘portfolio balance’ view this might explain why QE did not have a permanent effect on interest rates in the US.

In the euro area the bond purchases under the PSPP were not offset by similar factors. By 2015, when the PSPP started, the average fiscal deficit for the euro area was down to 2% of GDP and declining further so that the cumulated deficit over the three first years of the PSPP amounted to about 5% of euro area GDP. In the US, by contrast, the fiscal deficit amounted to 10% of GDP in 2009, the year the asset purchases started, and over the three years of most intensive QE operations the cumulated deficit was over 25% of GDP, more than five times higher than in the euro area. Moreover, there are no indications that national debt management offices increased the issuance of longer-term dated debt.

Contrary to the US, the PSPP thus led to a net reduction in the supply of longer term government bonds. This should have led to a strong impact on the yield curve through lowering the ‘term premium’ in the euro area. However, this is not confirmed by the data.

Central bank purchases and the yield curve in the euro area

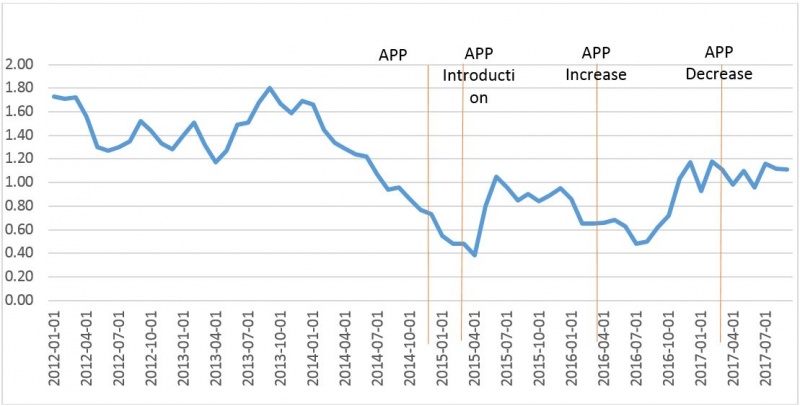

Figures 2 and 3 below show the difference between the yield on 10-year bonds and very short-term ones (around 3 months) for both, Germany and Italy.

Germany provides the risk-free curve for the euro area. The German yield curve should thus provide some information on the evolution of the term premium. The figure shows that the announcement of the PSPP around the turn of the year 2014/5 was followed by a decline in the difference between long and short rates of about 50 basis points, but this was more than undone in the three months after the purchases started. Moreover, a similar pattern was repeated when the ECB decided in mid-2016 to increase monthly purchases: at first the yield curve flattened, but then steepened again.

Figure 2: German yield curve: Ten year minus short-term (residual maturity 6 months)

Source: Fred.

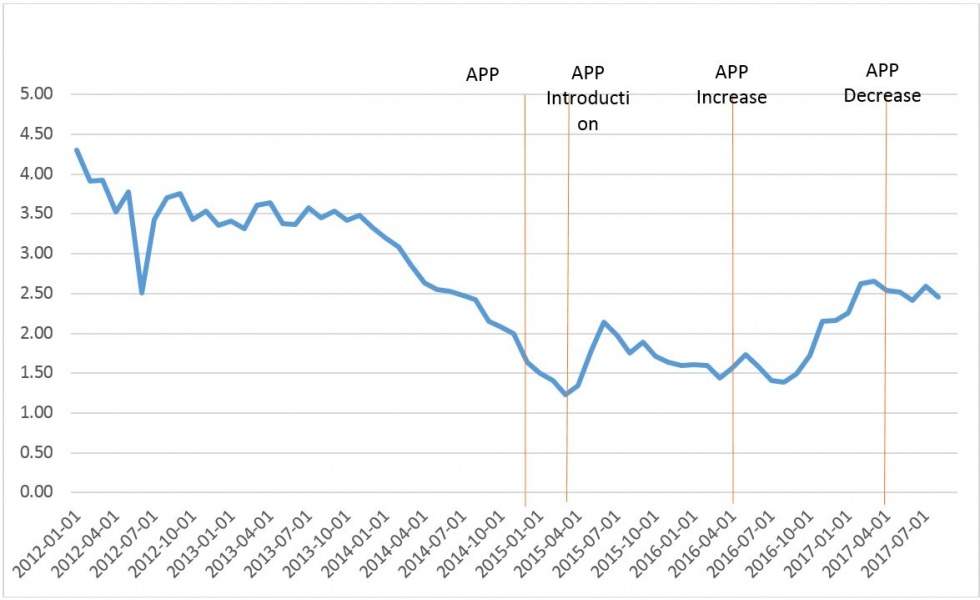

Figure 3: Italian yield curve: Ten year minus short term (treasury bills)

Source: Fred.

For Italy one could argue that the yield curve represents the combined effect of two factors: the ‘pure’ term premium, plus an additional risk factor related to the uncertainty about the longer-term sustainability of the country’s public finances. Even today (early 2018), Italian long-term rates are about 250 basis points higher than short-term ones, whereas for Germany the difference is only about 100 basis points. For Italy one would thus expect a particularly strong impact of the PSPP as it should have reduced both, the term and the risk premium.

However, this does not seem to have been the case. For Italy one observes, as for Germany, a temporary flattening of the yield curve upon announcement of the PSPP, but this is undone with the start of asset purchases by the Banca d’Italia. The 2016 increase in the bond purchases is followed by a substantial steepening of the Italian curve.

There is thus little sign of any permanent impact of the PSPP on the term premium despite the considerable reduction in the amounts of longer-term public debt available to the public.

Euro area QE and risk premia

Evaluations of the effectiveness of QE in the euro area have generally concluded that the impact was strongest for the peripheral countries with risk premia on government bonds (e.g. Altavilla et al., 2015). But why should the risk premium on Italian government debt fall, if one arm of the government (the Banca d’Italia) buys a chunk of it and issues its own short-term debt to finance this purchase? Total government debt is not reduced, and the debt servicing cost falls only by a fraction of GDP, as shown above.

A first mechanical effect is that the bond purchases by the Banca d’Italia lower the amount of bonds in the hand of the public. Central bank liabilities would presumably not be touched under any circumstances. This implies that, should a restructuring of public debt become necessary, the loss for the remaining private bond holders would have to be larger to reach any given reduction in public debt. One could thus argue that the PSPP increased the risk for private sector holders of government bonds.

The key advantage for a country under the threat of financial stress is that the liabilities of the national central bank (i.e. the Banca d’Italia) are not subject to speculative attacks or dual equilibria (as hypothesized in De Grauwe, 2011). (Short-term) central bank liabilities would anyway be typically exempted from any restructuring of public debt. Moreover, for the Banca d’Italia, the counterpart to its purchases of Italian treasuries were mainly Target2 liabilities, which would anyway not be subject to a speculative attack. One could thus argue that the PSPP program reduces the risk of ‘speculative attacks’ on national government debt markets.

However, the net impact of the PSPP on the risk premium remains a priori unclear. The probability of a default (caused by self-fulling expectations) falls, but the ‘loss given default’ (to borrow the term used for the evaluation of bank assets) increases because the loss would be concentrated on a smaller volume of bonds outstanding.

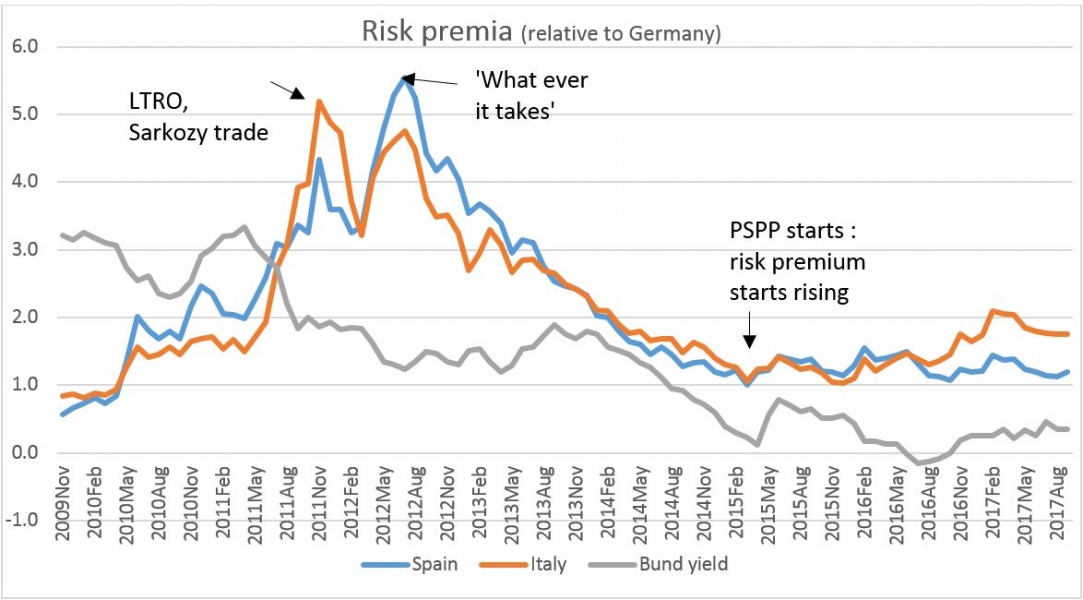

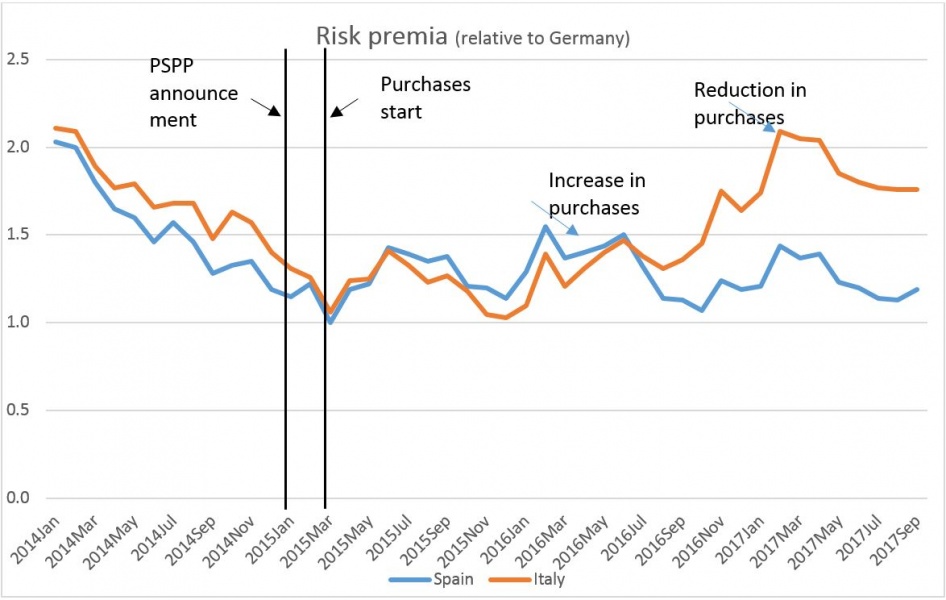

The empirical evidence is again somewhat contradictory. As already observed above, the Italian risk premium fell around the announcement (late 2014/early 2015) of the PSPP, but this fall was subsequently reversed shortly after the actual purchases started. Figures 4a and 4b below show the evolution of the spread of Italian and Spanish long-term (10 year) rates against Germany. The acute period of the euro area crisis is clearly visible in 2011/12. The first attempt to fight the crisis was the announcement, in late 2011, that the Eurosystem would provide banks with hundreds of billions of euro in 3 year loans (LTRO), which could be used to buy government bonds. This measure had a strong immediate impact, but after a few months risk spreads were back to new peaks. Today this so-called ‘Sarkozy trade’ (because the then French President encouraged banks to use ECB funding to buy government bonds and earn a hefty carry) is widely regarded as having been ineffective. However, the time path of the risk spread following the LTRO shows the same pattern as after the PSPP: a decline following the announcement but a rebound a few months after implementation started.

The one measure which seems to have had a major and durable impact was the announcement by the President of the ECB in July 2012 that the ECB would do ‘whatever it takes’ to maintain the euro area intact. That pronouncement, which was followed by the creation of the ‘OMT’ (Open Market Transactions), is widely credited with the long lasting decline in risk spreads which started in July of 2012.

In this respect one can again observe a different approach to measuring the effectiveness of a monetary policy operation: The OMT is credited with a decline of risk spreads which continued for almost two years. In the case of the PSPP a short lived decline is credited to the announcement and the subsequent increase is attributed (implicitly) to other forces (often not made explicit).

Figure 4a

Figure 4b

Concluding remarks

What could account for the temporary nature of the impact of the announcements and then implementation of purchases of huge quantities of government bonds?

Measuring the permanent effects of bond purchases is inherently difficult as bond markets tend to anticipate future policies. Event studies can alleviate this problem, but they can only measure impact effects, not permanent ones. It has also been argued that an increase in long term rates following bond purchases could be viewed as a sign that the policy is effective in stimulating demand and inflation, thus justifying higher rates. But this line of reasoning would make it impossible to measure the impact of bond purchases since both higher and lower rates could be taken as a sign of success.

Another reason why it is so difficult to disentangle the impact of bond purchases from other macroeconomic influences is that monetary policy operation represent clearly also a reaction by the central bank to the perceived state of the economy. Central bank took the decision to enter into bond purchase programs reluctantly. This was particularly true for the ECB, which took this step only ultimately towards the end of 2014, when it thought that there was a danger of deflation.

This creates a problem for the studies which estimate the impact of QE on the economy by just looking at changes in interest rates around certain announcement times. This procedure has similar problems as estimating a supply function from changes in prices at certain points in time. One is never certain whether the demand or the supply function has shifted more during these observations.

A similar identification problem affects event studies, and in particular those looking at the genesis of the PSPP. The President of the ECB had announced already in early 2014 that the ECB would take a sequence of measures, culminating in large scale asset purchases should inflation remain too low. As inflation (and inflation expectations) remained subdued during most of the 2014, the probability of an asset purchase program in the euro area was clearly increasing. It is thus not surprising that interest rates declined when the ECB announced that it was going to implement large asset purchases. This measure had become necessary (in the eyes of the ECB) because inflation was too low. But negative shocks to inflation can anyway be expected to lead to lower interest rates, especially when they are perceived to be permanent.

QE should thus be viewed as a (mostly predictable) reaction of central banks to negative inflation and/or demand shocks. These shocks could be global in nature as suggested by the recent empirical work showing that inflation has a strong global component (e.g. Belke et al., 2010 and Ciccarelli and Mojon, 2010). But even if the shocks are national in nature (i.e. one could argue that in 2014/15 there were stronger deflationary forces in the euro area than in the US), their impact on long-term interest rates could be global, given that long-term shocks to demand in any large economy would tend to be distributed across the global economy.

This view of QE as endogenous would still be compatible with the results from event studies, which generally find some reduction of interest rates around dates when major asset purchase plans were announced or became more likely. The fact that the ECB felt it necessary to adopt this unconventional policy tool could be interpreted by investors as new information about how the ECB views the state of the euro area economy. Given that the ECB can be assumed to have very deep knowledge of the euro area economy, this could motivate investors to modify their own views as well. However, the pessimism of the ECB proved actually unfounded. The euro area did not slip into deflation.

The evidence thus suggests that the impact of the PSPP was minor and temporary, as one would predict given that NCBs buying their own government’s debt implies ultimately only a maturity transformation of existing public debt, akin to an ‘operation twist’. Operations of this kind have had a limited impact in the past as well.

It follows that the importance of Quantitative Easing in the euro area has been vastly exaggerated. Thus, conversely, the end of central bank bond purchases in the euro area can be expected to be a ‘non-event’.

Alcidi, C., Matthias Busse and Daniel Gros (2017) “Time for the ECB to normalise its monetary policy? Insights from the Taylor rule”.

Altavilla, Carlo, Giacomo Carboni and Roberto Motto (2015), “Asset purchase programmes and financial markets: lessons from the euro area”, ECB Working Paper No. 1864, ECB, Frankfurt, November; www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1864.en.pdf.

Belke, Ansgar, Gros, Daniel and Osowski, Thomas, (2017), The effectiveness of the Fed’s quantitative easing policy: New evidence based on international interest rate differentials, Journal of International Money and Finance, 73, issue PB, p. 335-349, https://EconPapers.repec.org/RePEc:eee:jimfin:v:73:y:2017:i:pb:p:335-349.

Ciccarelli, M. and Mojon, B. (2010), “Global Inflation”, Review of Economics and Statistics, Vol. 92, No 3, pp. 524-535, August.

De Grauwe (2011), “Governance of a fragile Eurozone”, CEPS Working Document.

De Santis, Roberto, (2016) “Impact of the asset purchase programme on euro area government bond yields using market news” ECB Working Paper Series 1939, June.

Gros, Daniel (2015), “Lessons from Quantitative Easing: Much ado about so little?’, CEPS Policy Brief Implications of the expanding use of cash for monetary policy.

Gros, Daniel (2015b), “QE ‘euro-style’: Betting the bank on deflation?”, paper prepared for the European Parliament’s Committee on Economic and Monetary Affairs, June 2015.

Gros, D. (2016a) “Ultra-low/negative yields on euro-area long-term bonds: reasons and implications for mone-tary policy”, paper prepared for the European Parliament’s Committee on Economic and Monetary Affairs, September 2016.

Gros, Daniel (2016b) “QE Effectiveness”, paper prepared the European Parliament’s Committee on Economic and Monetary Affairs, June 2016,

Gros, Daniel (2016c), “QE infinity: What risks for the ECB?”, paper prepared the European Parliament’s Committee on Economic and Monetary Affairs, February 2016.

Gros, Daniel (2017) “Target imbalances at record levels: Should we worry?” CEPS Policy Insight No. 41, 23 November 2017, https://www.ceps.eu/system/files/PI%202017-41DG_TargetImbalances.pdf

Swanson, Eric, T. (2011) “Let’s Twist Again: A High-Frequency Event-Study Analysis of Operation Twist and Its Implications for QE2”, Brookings Papers on Economic Activity. The Brookings Institution.

See https://www.federalreserve.gov/newsevents/pressreleases/monetary20081125b.htm

One is tempted to consider the PSPP as ‘ELA for governments’. The non-application of the loss sharing provisions is the same as with ELA to banks.

The very first announcement of the intention to undertake an LSAP did indeed contain a commitment of the Fed to sterilise its purchases.