This paper weighs possible medium-term responsible policy responses to the extraordinary expansion of government spending arising from the COVID-19 outbreak. The paper is divided into two parts. In part one we look at conventional debt sustainability and question whether conventional rules created during a period of high interest rates and high inflation remain relevant. Current and future conditions support a case for government debt/GDP to remain elevated compared to history, conditional upon limited state interference in the economy to allow appropriate allocation of capital and resources.

In part two, we consider the historical experience of the United Kingdom. That country had several examples of one–off rapid, large-scale expansion of government debt relative to the size of the economy. On each occasion, the elevated level of debt to GDP was later reduced by a combination of relatively benign factors, including commitment to low inflation and a sound monetary system. This supported the financial probity of the UK government and allowed it to continue to borrow unimpeded.

Government spending in the United Kingdom has soared as a result of the COVID-19 crisis. There has been a sudden and large rise in the ratio of the national debt to national income, which has catalysed an ongoing UK debate about debt sustainability and prospects of austerity. This paper proposes a fiscal framework for the future, outlines the role the UK’s fiscal institutions should play in maintaining that framework, and examines historical case studies to support this proposal.

In part I of this paper, we propose a new fiscal rule that allows the considerably expanded UK government debt to be handled responsibly yet sustainably for future generations. Our fiscal rule is based on a recognition that the cost of government debt is unlikely to exceed nominal growth of the economy for many years to come. Our findings show that even when using highly conservative estimates of future growth, the stock of debt will be eroded. Moreover, the decline in debt stock is likely even if the country runs modest deficits for some years. It may be wise to plan to increase the stock of index-linked government bonds to ensure inflation discipline and further reassure domestic and foreign investors that the UK remains committed to its historic leadership in fiscal probity and investor protection.

It should be noted too that excessive intervention into the economy by government will impede this goal. But we note that intervention operates in two directions: excessive economic intervention by a government usually leads to misallocation of capital and an unfortunate tendency for the state to end up ‘picking losers’. On the other hand, excessive tightening, when such tightening is obviously not needed, unnecessarily undermines economic and political capital at a time when it is most needed. Government restraint (in this case, restraint from premature withdrawal of fiscal support) can be just as important as prudent long-term fiscal management in the long path to economic renewal. There is a fine balance between prudential consolidation and prudential support, but it is a balance that is worth pursuing.

History can be a guide here. In the second part of our paper, we examine historical case studies where the UK faced seemingly insurmountable debt burdens. A large spike in the stock of government debt has occurred several times in UK history. This paper draws on modern economics and Britain’s financial history and suggests a practical fiscal rule appropriate to current and future economic conditions. The rule would establish a sound basis for government finances and for debt sustainability without rushing unthinkingly to fiscal tightening as the economy recovers.

Figure 1: United Kingdom Debt-to-GDP, 1700 to 2021 (%)

Source: Bank of England and International Monetary Fund

Since the inflation of the 1970s, debt sustainability calculations have been based on assumptions of high inflation and positive real interest rates. However, in response to a one-off spike in debt, such as archetypically produced by war, such calculations can often mislead. This approach is no longer appropriate and needs revision. Rather, we argue that debt is sustainable if nominal growth is greater than the interest rate, provided the government’s non-interest deficit remains contained.

The fiscal rule we propose forecasts the average interest on government debt over the decade ahead, given borrowing costs signalled by financial markets today, and compares them with projected nominal GDP growth. Only if the interest rate is expected to increase above the nominal growth rate will adjustment to future primary surpluses be triggered today. Otherwise modest primary deficits can be tolerated. We propose that the OBR provides the analysis to underpin this rule and to monitor compliance.

Nominal growth at a higher level than interest rates is highly likely for the foreseeable future, meaning there is no immediate need for austerity post-COVID-19. But in the event that private activity rebounds and interest rates increase, fiscal adjustment will become necessary—though this will be largely automatic as tax revenues increase.

A sensible parallel policy to further alleviate uncertainty about future government policy would be to issue larger quantities of inflation-linked bonds. This would reassure investors as these bonds act as a self-regulating guard against unorthodox monetary behaviour, safeguarding the high reputation of UK debt management.

Although government debt may safely remain at an elevated level for a considerable time, it is important the state does not use interventions stemming from COVID-19 to interfere over the longer term with private capital-allocation decisions. This would inevitably distort economic decisions and reduce long-term growth potential, which in turn would damage debt sustainability and the goal to invest in and level up every part of the country.

“It was in truth a gigantic, a fabulous debt; and we can hardly wonder that the cry of despair should have been louder than ever. But again that cry was found to have been as unreasonable as ever. After a few years of exhaustion, England recovered herself. Yet, like Addison’s valetudinarian, who continued to whimper that he was dying of consumption till he became so fat that he was shamed into silence, she went on complaining that she was sunk in poverty till her wealth showed itself by tokens which made her complaints ridiculous. The beggared, the bankrupt society not only proved able to meet all its obligations, but, while meeting those obligations, grew richer and richer so fast that the growth could almost be discerned by the eye.

Macaulay, Thomas Babington. The History of England, from the Accession of James II — Vol 4 (1848)

Standard public debt sustainability analysis (DSA) relies on the assumption that the nominal interest rate on government debt is higher than the nominal growth rate of the economy (i > g). Let us suppose for a moment that this is true. If so, then standard DSA notes a government primary surplus is needed to achieve “sustainability”—the government’s primary balance being the difference between taxes and non-interest expenditure. Primary surpluses represent the current resources generated by the government to service or pay down the stock of debt. Formally, DSA requires the net present value of future primary surpluses to equal the debt stock today, all measured relative to GDP, to ensure sustainability.

Let us consider an example of this “standard” DSA world, where i > g, with a primary surplus of 1½% of GDP and nominal GDP growth equal to 5% – composed of 3% real growth and 2% inflation. And imagine the average nominal interest on government debt is 7½%—so about 5½% real. Then it is straightforward to show that a debt-to-GDP ratio of 63% is sustainable, equal to the NPV of future primary surpluses. If the debt stock were higher than this, debt would not be sustainable and fiscal adjustment needed.

Such numbers today seem outlandish. But they were not unreasonable in the late-1980s, when the global economy was still adjusting to restrictive monetary policy measures needed to tame the Great Inflation of the 1970s. It was against the backdrop of such a disinflationary environment that current DSA was inserted into the policy narrative, and when analysts and politicians first became accustomed to metrics such as the 60% public debt target. In the context of the Maastricht Treaty negotiations, the 60% figure was rationalized thus: “The debt reference value is very close to the average value of this indicator for the EC [European Community] in 1991” (Buiter, Corsetti, and Roubini). And 60% happened to conform at that time with what was needed for sustainability considering average primary surpluses, interest and growth rates for such countries.

But the UK (and global) economy is no longer in such a counter-inflationary environment, nor are there high nominal and real interest rates. Instead our main challenge is to assure sufficient demand and keep a floor on inflation. The discussion needs to go beyond the DSA of the 1980s. The recent observation by Olivier Blanchard in his American Economic Association (AEA) Presidential Address that “not only are today’s interest rates low, they are lower than growth rates” fundamentally overturns one of the cornerstones of the theory of public DSA sketched above. Indeed, in an earlier period working with the OECD in the early 1990s, Blanchard acknowledged the possibility that the interest rate on public debt could fall below the growth rate of the economy, in which case “the government could run permanent primary deficits . . . and these would eventually lead to a positive but constant debt level.” However, while flirting with this possibility, in this earlier paper Blanchard still fell back on the general presumption that the interest rate on government debt exceeds the growth rate—that it “prevails generally.”

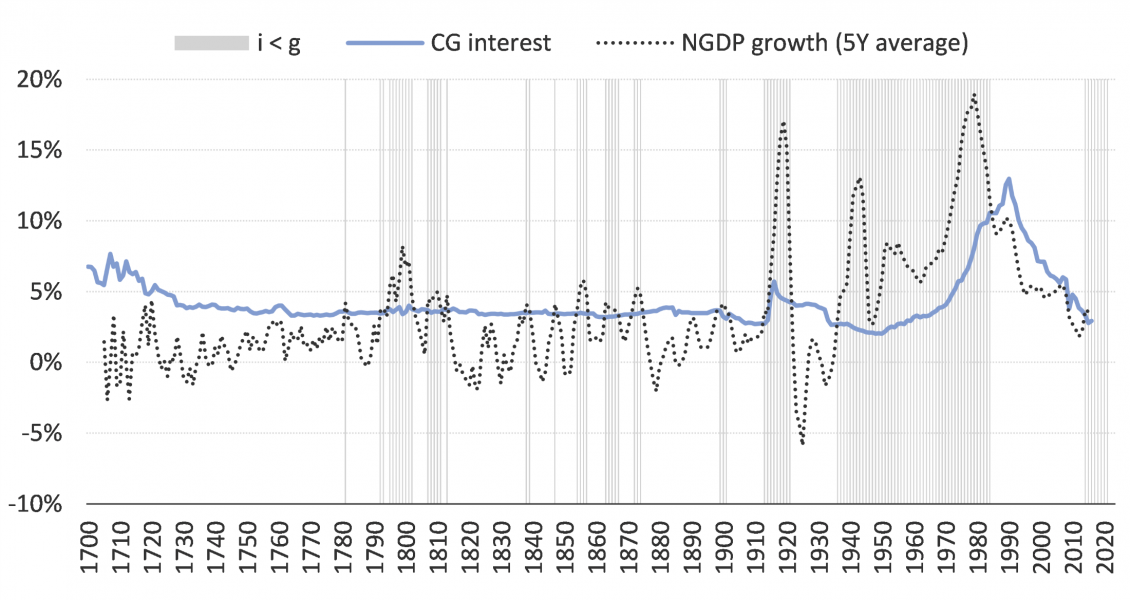

However, it might be that the 1980s and 1990s are an historical aberration—when the nominal interest rate indeed exceeded the growth rate. Indeed, during the post-war period the nominal growth rate of the UK economy was consistently above the average interest rate on government debt—that is, until the 1980s. See Figure 1. Taking a longer view, during the 1700s and most of the 1800s, the interest rate on government debt was higher than the nominal growth rate. Yet this period was constrained by the effects of the Gold Standard which constrained inflation. Outside the closing decades of the last century, when current DSA frameworks were forged, it might be argued the average interest on government debt generally falls below the nominal growth rate, and that we have returned once more to such a situation. This has important implications for periods when public debt is driven sharply higher, as at present.

Figure 2: United Kingdom: General government debt and central government interest payments (%)

Source: Bank of England and International Monetary Fund

First, the presumption that debt-to-GDP has to be immediately reduced post-COVID-19 is not (necessarily) supported by economic theory, so the justification for a fiscal retrenchment to achieve some target debt stock needs to be carefully made. Even if i > g then there would be no theoretical presumption that public debt should be driven lower—as noted above, it would only be necessary to achieve a primary surplus sufficient to service the debt at a higher level. But when i < g even such imperative for primary balance consolidation is not clear; indeed there is no guide from economic theory as to the necessary primary balance for given debt stock. It is conceivable that primary deficits can continue for some time without sustainability being compromised despite a sharply higher stock of public debt.

To be sure, there are some who argue that a lower public debt stock should be sought to provide “insurance” in case another shock emerges. However, experience in lowering or even stabilizing public debt stocks in recent decades illustrates problems with this view. But it should not be forgotten that the Nobel Prize-winner James Buchanan, among many others, argued that raising taxes to pay interest on debt acted as a disincentive to work and to private sector investment.

Public debt consolidation is often accompanied by the private sector assuming greater risk – which itself results in further macroeconomic instability ahead. During the resulting slowdown the central bank often eases monetary policy, contributing to asset price bubbles and risk taking. This can therefore create private sector sustainability challenges.

Second, should interest rates move higher, it would imply fiscal adjustment is required. For example, it is sometimes argued that the nominal interest on government debt will increase for demographic reasons in the medium-run. To be sure, the experience in Japan suggests this will not be the case. Indeed, beyond property and land, government debt provides a key vehicle in Japan for passing wealth between generations, implying demographic considerations support higher public debt. Still, suppose the average interest on government debt indeed increases. Policy need not react immediately except to acknowledge that if interest rates permanently increase then fiscal policy will adjust accordingly. Indeed, since the average maturity of public debt in the UK is 14.8 years, it will take some time for higher interest rates today to have a significant effect on the average interest paid on debt. During this time, it may be necessary to affect fiscal adjustment. However, it seems likely in such a case that fiscal policy will in any case adjust automatically—as private spending accelerates, competing for resources and causing the interest rate to rise, tax revenues will accrue at a faster rate, causing the primary fiscal balance to adjust accordingly. In this case, all that is required is that the fiscal steward collect the taxes that emerge to service or even repay debt.

Against the arguments in favour of a large fiscal intervention now and the slow withdrawal of fiscal support later, there remain legitimate concerns that continued state involvement in the economy will result in growing political pressure to attempt to “pick winners” along with the misallocation of resources. This would be the case if otherwise unprofitable activities are not allowed to slide into obsolescence but instead are underpinned by state intervention. In fact, this would be equivalent to government intervention “picking losers.” Protracted government involvement distorts the distribution of resources, prevents the unleashing of private enterprise and the process of innovation and progress, and hampers the necessary post-COVID-19 and post-Brexit adjustment to changing tastes and technologies. Such intervention would in fact imply slower growth in the real economy and higher inflation. As such, it would underpin lower real incomes in the future and undermine public debt sustainability. This implies public interventions should be generous, but targeted and short term. It should be acknowledged that there are inevitable limits to knowledge about the future, and that even well run firms can fail through imperfect foresight. One persuasive means of showing commitment to the existing policy framework—including a new fiscal rule which might tolerate a higher debt stock—would be to increase issuance of index-linked bonds above historical levels.

All of the above considerations suggest a new fiscal rule is appropriate. It would be one that takes a longer horizon than existing approaches, and links fiscal adjustment to the projected difference between the average interest on outstanding government debt and the nominal growth rate of the economy. The yield curve facing the government at the time of the sustainability assessment would determine the interest rate assumptions, to avoid inevitable optimism. The rule would distinguish explicitly between a jump in the stock of debt with no associated increase in long term spending commitments, and debt financed run-of-the-mill expenditure. The former could be permitted under the rule, the latter would not. An illustrative example of how to articulate this rule is as follows:

The shorter horizon for adjustment compared with the decade forecast acknowledges lags between asset prices and the average interest rate while preventing governments from delaying fiscal adjustment to the next parliament—accepting responsibility immediately.

To ensure the credibility of this rule, the OBR would be charged with providing the analysis and projections as well as ex post monitoring of necessary fiscal adjustment.

There have been three similar, but far from identical, experiences for Britain when vast new spending needs arose. All were during and immediately after major wars, when British government spending surged. The first occasion was the Revolutionary/Napoleonic Wars of the late eighteenth/early nineteenth centuries, when spending resulted in the accumulation of a huge debt and a debt-to-income ratio close to 200%. See Figure 2. There was a similar expansion in WWI when spending again surged, and again during WWII when the need for spending rose dramatically once more. Debt followed and a debt-to-income ratio again reached about 250% at its peak in 1947.

In contrast to other historical episodes when countries faced large debt overhangs as a result of wars, Britain was rarely divided. There was no loss of tax revenues. Tax revenues increased. While there was a clear enemy to be defeated, the tax revenues flowed and on a bigger scale than previously. But taxation alone could not produce sufficient sums. Borrowing had to be relied on. Britain had certain advantages here. It had been at war most of the time between the 1680s and the late eighteenth century. In that period it built a reputation for probity in peacetime and the repayment of debt acquired in wartime. When it came to these three major wars, it had no difficulty borrowing either domestically or abroad.

Nevertheless, the burden of the debt after all of these wars was extremely heavy. How could it be managed? There were really only two viable ways. One was from economic growth and the other was from inflating the debt away. Strictly speaking there were two additional options. One was simply to default. But that was anathema to the governments of the time, and in any case would have damaged or even ruined future possible borrowing requirements. A fourth option would have been strict spending rules, and the further raising of taxes. In the climate of the times neither was acceptable. Following the Napoleonic Wars, there were demands for smaller government. After WWI, the pressure was for spending, particularly on housing, for returning servicemen. And after WWII, a newly elected Labour Government came to power on the promise of big spending that included extensive nationalisation.

Thus, the two options were growth or inflation. After the Napoleonic Wars, there were also demands for greater probity in the affairs of the state and a return to the gold standard that had been abandoned in the early years of the war. As that was aimed for and achieved, inflation was ruled out leaving only growth alongside modest primary surpluses. Similarly, after WWI the gold standard that had been suspended on the outbreak of war in 1914 had to be restored and was in 1925 albeit in slightly different form. Again there was no inflation. Following WWII, there were the large spending plans of the new Labour Government. There was also a much looser association with a metallic base for the currency and the possibility for inflation certainly existed and some inflation duly appeared.

Interestingly, in all three cases the rate of economic growth following the peak point in the debt-to-income ratio was strong and the ratio slowly declined. Only in the last of the three did inflation play some part, as did an increasingly heavy tax burden to pay for an increasing role of the state, a tax burden that continued for many years.

It is clear that approaches to reducing the debt-to-income ratio have differed substantially from episode to episode. However, typically managing the debt overhang has been constrained by the overall policy framework – in particular, the money supply regime and the nature of the state.

The importance of the money supply regime has already been implied. With a fractional reserve banking system, the money supply can change according to the reserve-holding behaviour of banks. But the only source of sustained money supply change is a sustained change in the liquid reserves of banks – the monetary base, as it is known in many countries. The major study of this was Phillip Cagan’s for the United States, but similar results appear for other countries. Hence, so long as the growth of the monetary base was constrained, the growth of broader measures of the money supply was constrained, and so too was inflation. If the monetary base comprised gold (the gold standard) or some other metal (silver for example, or even a bimetallic standard) then the base could grow only to the extent that the supply of the metal or metals did.

Of course, the question of what kept countries on that gold standard must arise, but it is useful also to consider – for the underlying questions are the same – what keeps countries to any low inflation commitment.

Britain could have left the gold standard after the Napoleonic Wars, but instead of perpetuating the wartime suspension the standard was restored (in 1821). And again, Britain could have perpetuated the suspension of the First World War, but instead resumed gold, and at the pre-war parity, until finally forced off in the turmoil of the years leading to the Great Depression in the United States. What kept Britain on gold?

Partly there was simply a feeling that being on the gold standard was natural, that there was nothing else that could be done. But also it was well established that stable prices were desirable, morally and also good for prosperity and growth. Then, too, it was well established that if a country in effect repudiated its debts by debasing the currency then it would be unable, or at the least experience great difficulty, in borrowing again at times of stress. This was, indeed, an argument Alexander Hamilton used when urging the revolutionary Congress to honour the debts of the previous (colonial) administration of what became the United States of America. (Montagu Norman made this point, among other arguments, when he urged Britain to not only return to gold after WWI, but to do so at the old parity.)

Thus, governments are reluctant to use rapid inflation to reduce the debt-to-income ratio. It makes future borrowing more difficult. Today’s monetary framework—including Sterling’s quasi-reserve currency and a clear inflation target—provides additional policy freedom not previously available. But it does not allow an excessive reliance on inflation and does imply a commitment to avoid deflation. Such a credible monetary framework will likewise help contain future borrowing costs.

There are, it should be remarked, many other factors aside from the level of debt that can lead to or allow inflation. Important among them is, quite simply, the ability to make mistakes. Britain during the Heath-Barber administration is an example and inflation started to soar. That was not, though, an attempt to reduce the burden of debt. It was simply a complete misunderstanding of the cause and cure of inflation. There can also be one-off shocks to the price level that are allowed to turn into inflation through a reluctance temporarily to squeeze the economy – that might be a mistake, or a conscious and well-informed decision about trade-offs.

In other words, many things can lead to governments allowing inflation. But choosing to inflate deliberately, as a way to reduce the debt-to-income ratio, involves a neglect of the future. This is what A. C. Pigou, the early twentieth century British economist, referred to as a “defective telescopic faculty.”

That applies whether keeping to a metallic standard or adhering to a rule or to an inflation target. All are self-imposed constraints. There are exceptions to that. An example is the cabinet minister who, when he heard that Britain had left the gold standard, exclaimed in surprise, “No-one told us we could do that.” But, unfortunately, ignorance so benign appears to be rare.

Accordingly, then, without exception such deliberate inflation is avoided only by states which are secure, with a rule of law and the expectation of a basic level of political stability. In contrast, kleptocracies, unless they are stupid as well as corrupt, must always have an eye on the exit.

Systematic debasement to reduce the burden of debt does not happen in well-ordered societies. When the Governor of the Bank of England, Andrew Bailey, was asked about the possibility that inflation would surge in Britain as a response to the sharp increase in the debt, he responded that Britain was not Venezuela. That is as neat a summary of the above argument as one can imagine.

But though neat and to the point, it is incomplete. It does not rule out the possibility of a few years of modest inflation. Suppose inflation averaged 5% per annum for ten years. That does not appear intolerable. But compound 5% for ten years, and the price level has gone from 100 to around 170 (the figure depends on details of the calculation). Such a price level rise would have a substantial effect on the debt-to-income ratio, so long of course as the debt was not primarily index linked.

And here we have a fortunate accident. Index linked debt was intended to be a way of protecting savers from inflation, so long as they held such debt. As noted above, it turns out also to be a way of constraining governments that were minded to use inflation to solve a problem. If enough debt is indexed, inflation can still happen, through accident or error, but it does remove at least to some extent the incentive to inflate to reduce the burden of debt.

This short paper makes two closely related points, one primarily relevant to the future, the other addressed to the always pressing question, “What should we do now?”

A fiscal rule is proposed that henceforth would promote fiscal sustainability, would avoid the explosions of debt to finance long term spending commitments. This rule differs from existing ones in that it builds in a mechanism to adjust for the possibly changing relationships between interest rates and economic growth. There need be no ad hoc and therefore inevitably distrusted changes.

Turning to the second question, it is shown that there have been episodes in the past where Britain experienced sudden jumps in the stock of debt. Analysis of these episodes shows that they cause no problems provided that they do not lead into sustained increases in the growth of debt financed spending.

All that is needed to implement both recommendations is clarity and maturity in political discourse. This is an endeavour in which all of the British public should become engaged.

Blanchard, Olivier (2019) “Public Debt: Fiscal and Welfare Costs in a Time of Low Interest Rates,” Peterson Institute for International Economics Policy Brief 19-2.

Blanchard, Olivier; Jean-Claude Chouraqui; Robert Hagemann and Nicola Sartor (1991) “The Sustainability of Fiscal Policy: New Answers to An Old Question” OECD Economic Studies 15(15), April.

Buiter, Willem; Giancarlo Corsetti and Nouriel Roubini (1993): “Excessive deficits: sense and nonsense in the Treaty of Maastricht,” Economic Policy (1). Also translated into Italian and published as “Disavanzo eccessivo,ragionevolezza e nonsenso nel Trattato di Maastricht,” in Rivista Di Politica Economica, June 1993, 3-82. Reprinted in The Political Economy of Monetary Union, Edited by Paul de Grauwe, pp. 297-331, Edward Elgar Publishing Ltd, Cheltenham, 2001.

Cagan, P (1965) Determinants and Effects of Changes in the Stock of Money, 1875-1960. New York: Columbia University Press for the National Bureau of Economic Research.

Capie, Forrest (1986) “Conditions in which Hyperinflation has Appeared” in Brummer and Meltzer (eds.) Carnegie-Rochester Public Policy Series, Reprinted in Capie (ed.) Major Inflations in History, Aldershot, Edward Elgar.

Capie, Forrest and Geoffrey Wood (2015) ‘Central bank independence: can it survive a crisis?’ in Owen Humpage, ed., Current Federal Reserve policy under the lens of economic history, New York, CUP.

Pigou, A.C. (1928) A study in Public Finance, MacMillan.

Macaulay, Thomas Babington (1848) The History of England, from the Accession of James II — Volume 4.

The views expressed in this paper may not reflect the views of the institutions in which the authors are affiliated.